As with much of the industrial sector, it's been a challenging year for trucking companies. Uncertainty around tariffs and ongoing weakness in manufacturing and the industrial economy have led to most sector stocks falling this year.

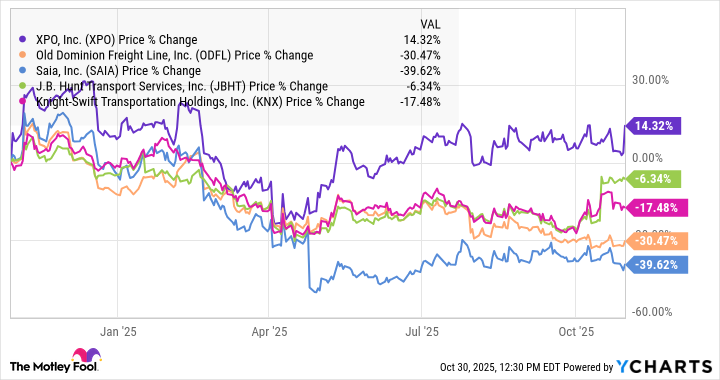

XPO (XPO +4.16%) is an exception to that rule. The stock is now up 13% year to date. As you can see from the chart below, it's the only one of those five major trucking stocks to have gained, and it's significantly outpaced its two closest rivals, Old Dominion Freight Line (ODFL +1.96%) and Saia (SAIA +1.68%), this year.

XPO put some more daylight between itself and its peers on Thursday after it delivered strong third-quarter results in a challenging macroeconomic environment.

Revenue rose 2.8% to $2.11 billion, which edged out the consensus at $2.07 billion. Revenue was up 0.3% to $1.26 billion in North American Less-Than-Truckload (LTL), its core business, while European Transportation revenue rose 6.7% to $857 million as it benefited from its leading position in markets like France, Spain, and Portugal.

What most impressed the market, however, was XPO's improvement in operating margin. Its adjusted operating ratio, the inverse of operating margin, fell 150 basis points to 82.7%, outperforming seasonality, and it was the only one of the top three LTL carriers to report an improving ratio this quarter.

In an interview with The Motley Fool, Chief Strategy Officer Ali Faghri gave credit to continuing service improvements, including in areas like damage control and on-time performance. As the company has improved service, it's been able to raise prices. This led to LTL yield, or pricing, rising 5.9% in the quarter, helping it overcome a decline in tonnage and shipments as industry demand remains weak. Shipments per day were down 3.5%, while tonnage dropped 6.1%.

Image source: XPO.

How AI is playing a role

Perhaps the biggest announcement from XPO in the quarter was the AI-driven productivity improvements it touted.

The company is leveraging artificial intelligence in a number of ways, including helping to control costs and improve efficiency and productivity. For example, as Faghri explained, XPO is now fully automating decisions about how it moves freight around its network, essentially removing the human decision-making component from the process. By optimizing the linehaul network with AI, the company had a low-single-digit improvement in productivity, which is significant at scale, driving tens of millions of dollars in savings over the course of the year.

It's rolling out AI in other areas, including pickup and delivery operations, managing labor at the loading dock, and using it for pricing and scales. Over the coming years, management expects it to drive further productivity and margin improvements.

Related to the linehaul management, XPO reduced outsourced linehaul miles to a record 5.9% of its total, down 770 basis points, from the previous year, and helping to drive profitability. The company still sees an opportunity to push outsourced linehaul miles lower over the coming years.

NYSE: XPO

Key Data Points

Is XPO a buy?

With manufacturing remaining weak, the macroeconomic climate is still challenging for XPO and its peers, and it has been for the last three years.

However, that should eventually change. The company is well-positioned to capitalize on an increase in demand, which could send profits soaring, given the improvements it's made in a weaker environment.

Meanwhile, as it continues to harness the power of AI and make other improvements at the service level, the company should continue to expand margins, even if the macro environment doesn't cooperate.

Over the long term, XPO still looks like a smart buy. If manufacturing rebounds, the stock could surge.

![XPO LTL truck road side profile XPO_Drivers_01_0488 web[6]](https://g.foolcdn.com/image/?url=https%3A%2F%2Fg.foolcdn.com%2Feditorial%2Fimages%2F795964%2Fxpo-ltl-truck-road-side-profile-xpo_drivers_01_0488-web6.jpg&w=3840&op=resize)