O'Reilly Automotive (ORLY +1.13%) has quietly been one of the top-performing stocks of this century.

Its network of auto-parts stores across the country, a hub-and-spoke business model that helps keep inventory fully stocked, and close relationships with repair shops have all helped it deliver steady growth over the years.

The stock price is up a whopping 61,200% since its IPO in 1993 and has delivered steady gains throughout its history.

It's not too late to buy the stock, but there are a few things you should know about O'Reilly before doing so. Keep reading to see two of them.

Image source: O'Reilly.

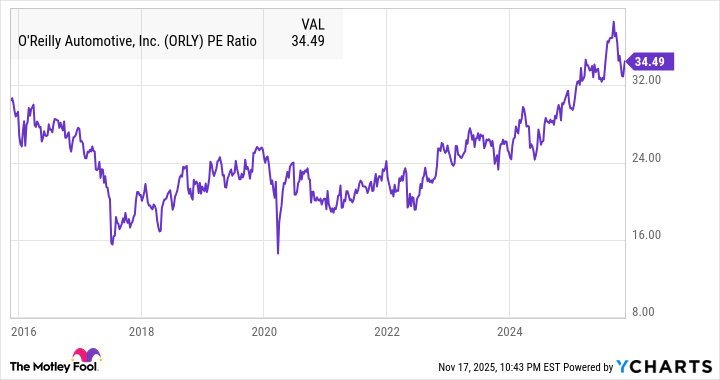

The stock is historically expensive

You might expect a top performer like O'Reilly to be expensive, and that is the case. In fact, with the exception of a pullback on the recent sell-off in the market, O'Reilly is more expensive than it's been in a decade.

Data by YCharts.

O'Reilly now trades at a price-to-earnings ratio of 34, which is a premium to the S&P 500 at 28. O'Reilly has a similar valuation to big tech stocks such as Microsoft, but it's growing more slowly.

O'Reilly delivered solid results in its third-quarter report, with comparable sales up 5.6% and earnings per share up 12% to $0.85 on a 9% increase in operating income.

O'Reilly doesn't pay a dividend and has instead used its profit to buy back stock. That's helped drive its performance over the long term by lifting earnings per share. Over the past year, O'Reilly's shares outstanding have fallen by almost 3%.

NASDAQ: ORLY

Key Data Points

This could be a good time to buy

Aftermarket auto-parts retailers like O'Reilly Automotive tend to be countercyclical, meaning they do better during recessions and down economies. That's because people tend to delay purchasing new cars during tough times, and therefore spend more on repairs, as having a functional vehicle is essential for most Americans.

There are already signs of pressure in the auto market. Delinquencies are rising, and there have been some high-profile bankruptcies in the industry as well. O'Reilly was confident enough to raise its full-year outlook in the third-quarter report, calling for comparable sales growth of 4%-5%.

Whatever happens in the near term, O'Reilly still looks well-positioned to continue to grow over the long term, as the company is still opening new stores, and its sales are well balanced between the DIY (do it yourself) and the DIFM (do it for me) channel.

If the market does continue to weaken, O'Reilly could prove to be a good place to park your cash, despite its current high valuation.