As we approach Thanksgiving, I wanted to take a step back and look at two stocks I am thankful for. Not only have these stocks provided solid returns for me (though I could have done better, as you'll find out), but they've taught me even more critical lessons along the way.

Today, I'll discuss the growth stock I'm grateful to have once held (for a while), the lessons it taught me, and the unstoppable stock I'm buying now after applying these lessons.

Image source: Getty Images.

Remember Amazon's Fire Phone?

It was 2014, and I was a happy Amazon (AMZN +1.96%) shareholder. I was somewhat early in my Foolish journey, and if I remember correctly, Amazon stock had nearly tripled for me in just a few years of owning it.

Quick returns like this can have a way of making investors feel invincible, or even like they're playing with "house money." At least that's how I felt at the time.

So, when Amazon announced the upcoming release of its Fire Phone in June of 2014 -- an idea I really disliked -- it was a no-brainer to sell the stock. It wasn't so much that I thought the company was headed for ruin, but rather that I thought the phone was a terrible idea.

Now, with the benefit of hindsight, I can say that I was absolutely right about the Fire Phone. However, I was wrong about Amazon stock. While the Fire Phone was a complete flop, Amazon went on to become a 14-bagger.

NASDAQ: AMZN

Key Data Points

The lessons I missed at the time were to avoid short-term thinking, to trust the management of a founder-led company, and not to bet against innovation (that is, new ideas, even if they were sometimes bad).

Suppose Amazon and Jeff Bezos had been perpetually afraid to fail, as they did with the Fire Phone. In that case, they might never have tried expanding beyond selling books online -- creating Amazon Web Services, buying Whole Foods, building an advertising empire, or developing one of the most no-brainer memberships out there in Amazon Prime.

Long story short, Foolish investors need to give management some time to let ideas play out -- especially at founder-led companies, which typically outperform the market.

These lessons all apply to one of my favorite core holdings today, Organ Care System (OCS) provider TransMedics Group (TMDX +0.28%).

Oh no, TransMedics bought an aviation company

I bought the promising growth stock at the beginning of 2023, and it immediately raced out to early gains. TransMedics' Organ Care Systems help keep donated livers, hearts, and lungs functioning and healthy on their way to their donees -- a far superior solution to traditional ice storage.

However, when management announced that it was acquiring Summit Aviation in August 2023, my initial thought was that TransMedics' ambitions of achieving higher margins were gone after adding such a capital-intensive business.

The market seemed to agree, and its share price was halved over the next few months.

NASDAQ: TMDX

Key Data Points

But despite my initial instinct and the market's negative stance on the stock, I didn't take any action with my position. I just gave management time.

Had I not learned from Amazon to do that, especially when letting founder-led companies try new ideas, I probably would have sold TransMedics early on. I could have cashed in on my quick gains and gotten away from an idea I didn't like.

However, by the end of the year, CEO and founder Waleed Hassanein had painted a vision for the company's future that included a nationwide logistical network. This vast network could enhance organ utilization rates and improve overall donation outcomes.

Two years later, it's safe to say that the founder has delivered on this vision, with TransMedics' stock tripling from its 2023 lows and its sales more than doubling over the same time. Not only that, but the company's in-house aviation unit is now utilized by 78% of the transplants performed under its National OCS Program.

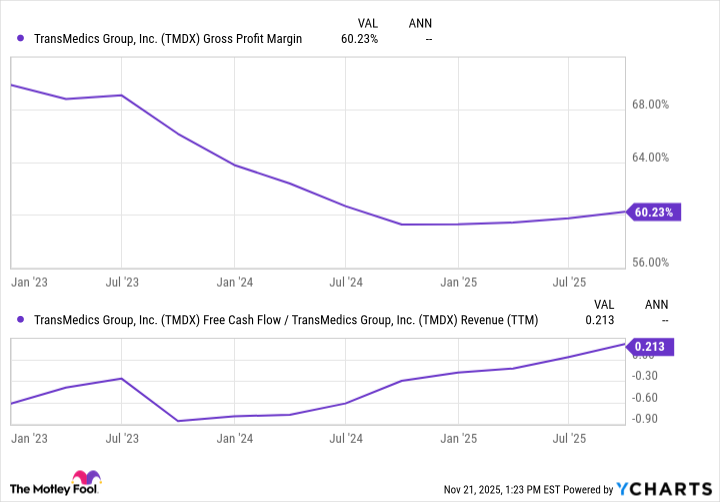

While I was (sort of) right about the new aviation unit cutting into TransMedics' margins, it only slightly lowered gross margins, whereas the company's free-cash-flow margins ballooned:

TMDX Gross Profit and Free Cash Flow Margin data by YCharts

In the most recent quarter, the company's transplant revenue increased by 32%, logistics revenue rose by 35%, and net profit margin stood at 17%.

TransMedics aims to more than double its transplants to 10,000 over the next few years. Furthermore, it plans to expand into the kidney donation and international markets -- opportunities that could be multiples larger than its existing operations.

Naturally, concerns have already arisen about these two new markets, and about whether TransMedics' next-generation heart and lung systems will achieve any measure of success. However, I'm going to simply think back to that Amazon Fire Phone, keep adding to this winning stock, and give the promising founder-led company plenty of time and space to execute on its long-term vision.

As to why I'm happy to share this mildly embarrassing story with everyone, it boils down to a humorous but true quote from Warren Buffett: "It's good to learn from your mistakes. It's better to learn from other people's mistakes."