In line with a broader market sell-off, Centrus Energy (LEU +3.55%) has seen its stock decline about 14% over the past five trading days (as of Novembber 18). The nuclear energy stock has now dipped over 45% since hitting a high of around $436 per share in mid-October, returning to a price it had two months ago in September.

For those who have kept Centrus on the waitlist, the sell-off could open a slight window. But is now really the time to buy Centrus, or should you wait this one out?

The value proposition: Domestic enrichment

Centrus sits alone in a critical corner of the nuclear energy industry.

Not only is it one of the few U.S. companies licensed to enrich uranium, but it's also one of the few with a license to produce high-assay low-enriched uranium (HALEU), a specialized fuel critical for several next-generation nuclear reactors.

Ground floor side-view of a HALEU cascade. Image source: Centrus Energy.

To underscore that last point, it helps to understand why HALEU matters.

Most commercial reactors run on uranium enriched to about 3% to 5% U-235. That's fine when you have a large nuclear power plant, but too bulky and inefficient for the smaller, more compact reactors poised to redefine the future of nuclear. HALEU pushes the enrichment level up to between 5% and 20%, which helps these smaller reactors get more power per unit of volume.

Producing HALEU, however, isn't something anyone can do. It requires specialized centrifuges and a technical know-how to control a very sensitive process. And Centrus, which was founded in 1992 with facilities that once belonged to the Department of Energy, has had that know-how for quite some time.

The elephant in the room: Valuation

As mentioned above, Centrus is one of the only U.S. nuclear companies with regulatory approval to enrich HALEU. That uniqueness has contributed to the stock's incredible 225% surge in 2025, yet it has also left it looking expensive by conventional standards.

NYSE: LEU

Key Data Points

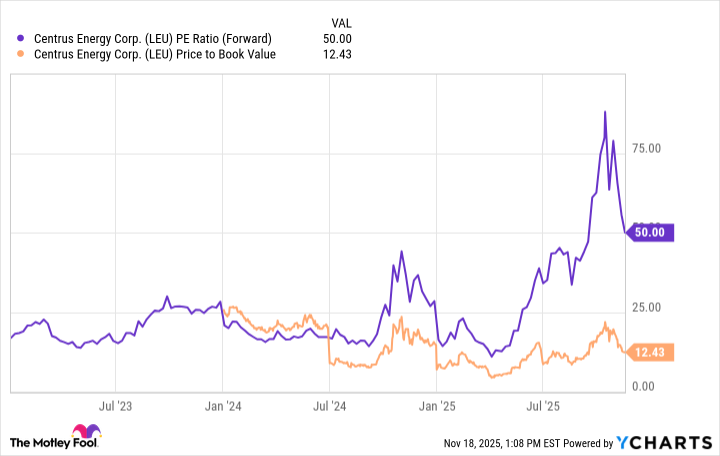

At today's price, the stock trades at roughly 12 times its book value, about triple the price-to-book ratio of the VanEck Uranium and Nuclear ETF. That doesn't make it overvalued on its own -- its unique ability to produce HALEU commands a premium -- but it does indicate that a lot of enthusiasm is baked into the price.

One metric that may lean more clearly toward overvaluation is the forward price-to-earnings ratio, which is currently north of about 60. A number that high means investors aren't paying for what Centrus earns today, but what they hope it will earn in the future. In practice, it means a smooth ramp-up of HALEU production. Any major delays or setbacks -- and in an industry this new, you have to expect them -- could see investor enthusiasm sober up real quick.

LEU PE Ratio (Forward) data by YCharts

To be sure, Centrus has already started producing HALEU, thanks in large part to a cost-shared contract with the Department of Energy.

In June, it earned about $7.3 million on a delivery of 900 kilograms (kgs) of HALEU to the DOE, and it's expected to deliver another 900 kgs by June 2026. That figure was about 10% of its third-quarter revenue, so it wasn't completely meaningless. At the same time, it doesn't change the fact that most of the company's market value still rests on what's (hopefully) coming next.

Is it a buy now?

As a long-term shareholder of Centrus, I see a lot of potential in this company. It has a legitimate technical edge and a deep regulatory moat. As such, I'm excited about its recent HALEU production wins and the role it could play in a more robust U.S. uranium supply chain.

At the same time, I know this stock isn't for everyone. Centrus is building a brand-new supply chain, which requires not just time and money, but also patience as it smooths out the process. Meanwhile, its current valuation assumes almost near perfect execution; in other words, things will likely get bumpier before they get clear.

For investors who can stomach that volatility, Centrus could be a compelling long-term bet on the future of advanced nuclear. More conversative investors, however, may want to consider a nuclear energy ETF instead.