Pizza stock Domino's Pizza (DPZ 1.98%) has underperformed for investors over the last one-, three-, and five-year periods. The S&P 500 has done better over each time span. One would have to zoom out to the 10-year performance to find a period wherein it was better to own Domino's stock instead of just owning an S&P 500 index fund.

On one hand, Domino's is one of the strongest restaurant chains on the stock market. And investors should gravitate toward high-quality businesses such as these. On the other hand, Domino's has struggled with top-line growth in recent years, with revenue only increasing by 18% total over the last five years.

Image source: Getty Images.

With nearly 22,000 locations worldwide, growth is hard to come by at this point for Domino's. That said, growth isn't the only path toward creating shareholder value.

Can Domino's stock have rewarding upside ahead?

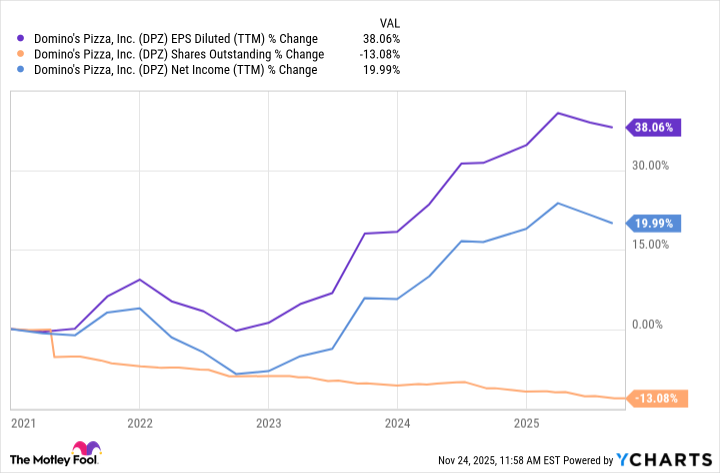

Domino's has grown its earnings per share (EPS) roughly twice as fast as its revenue over the last five years. And the reason is simple: This is a high-margin business, and management buys back stock on a regular basis. So while profits overall are somewhat stagnant, they're going up on a per-share basis because the overall share count is going down.

Data by YCharts

Another thing in shareholders' favor is that Domino's does pay a dividend. While modest, it does go up regularly, with management increasing the payment for 13 consecutive years.

To be sure, Domino's Pizza shareholders still got a smaller return than the S&P 500 over the last five years, even after accounting for the dividend. But returns are a little improved for investors who reinvested the dividends along the way.

Where do Domino's shareholders go from here?

Domino's Pizza continues to grow its sales and will likely do so in coming years. But growth is expected to remain at a modest single-digit rate. Going forward, shareholders can expect profits to stay strong, allowing management to continue buying back stock and paying dividends.

NASDAQ: DPZ

Key Data Points

Profit margins are likely to stay strong for Domino's because of its competitive advantages. The company's restaurants are primarily operated by its franchisees, who pay into an advertising fund and use the company's supply chain.

By pooling resources, Domino's operates one of the most efficient supply chains in the world, keeping food expenses lower than competitors.

And having collected nearly $400 million in advertising funds through the first three quarters of 2025, Domino's has a bigger budget to get its message out to consumers.

Again, growth could be modest for Domino's. But the other thing in shareholders' favor today is the price tag. As of this writing, the stock trades at 22 times its free cash flow, which is its lowest valuation in over a decade. It may have underperformed in recent years, but it's now more attractively priced, which could set it up for better returns over the next five years.