It's been a tough past couple of years for Constellation Brands (STZ +1.59%) shareholders. The stock's down more than 50% from its early 2024 peak, and seemingly still moving lower. The end of the COVID-19 pandemic's worst and the beginning of an inflation-riddled period is taking a double-barreled toll on alcohol consumption. Not only are people drinking less of it for health-minded reasons, but for cost-related reasons as well.

The sellers, however, have arguably overshot their target, ignoring how the company's foreseeable future looks much better than its recent past. This budding turnaround makes the pullback an attractive entry opportunity for patient investors.

Constellation Brands is on the defensive

You may know the company better than you think. Constellation is parent to popular beer brands Modelo and Corona, which account for the bulk of its revenue. It also owns a handful of smaller wine brands, like Kim Crawford and Ruffino, as well as spirits like High West whiskey and Mi Campo tequila.

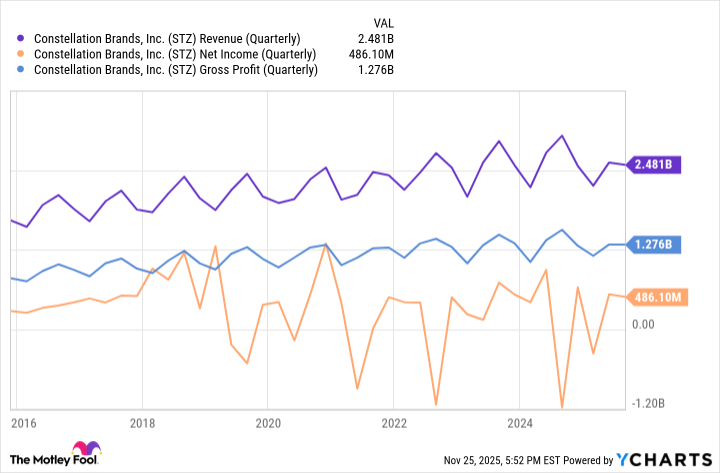

The $23 billion company did $10.2 billion worth of business last fiscal year, up slightly from the previous year's top line.

NYSE: STZ

Key Data Points

That would be the end of a respectable growth streak, though. Sales are down 10% through the six-month stretch ending in August. Gross profits and operating profits are similarly lower, mostly thanks to "a difficult socioeconomic environment that dampened consumer demand across the industry."

That's not an inaccurate explanation. The Beer Institute reports that through September, shipment volume is down 5%, jibing with data from the Brewers Association. Separately but simultaneously, a recent survey from Gallup confirms the business' worst fears -- a record-low 54% of American adults are now regular drinkers, with a majority of this crowd citing health concerns as their top reason for cutting back.

To this end, Constellation Brands' guidance for the full year ending in February suggests a 4% to 6% top-line dip, leading to a slightly bigger decline in operating income.

STZ Revenue (Quarterly) data by YCharts.

The bullish case

But things are about to change in a way the market isn't pricing in -- or even seeing -- yet. In simplest terms, think of 2025 as a reconfiguration year for Constellation Brands. It's rebuilding a better business for what should (hopefully) be a better business environment.

Chief among these changes so far is the decision made earlier this year to shed certain wine brands with lower price points. Although wine isn't a particularly big piece of the company's revenue, as CEO Bill Newlands explained of the move, "concentrating our wine and spirits portfolio in higher-growth segments remains an important element of our overall business strategy and complements our higher-end beer portfolio."

He's right. While overall alcohol consumption is down, higher-end alcohol consumption is up, even if only modestly. This bodes well for Constellation's breadwinning beer brands Modelo and Corona, neither of which are priced out of reach for most beer drinkers, but both of which are clearly priced above most baseline beers.

Image source: Getty Images.

Then there are the company's more operationally minded efforts. In Newlands' words, spoken at Barclays' recent consumer staples company conference, Constellation is "controlling the controllables." This includes plans to cull $200 million worth of unnecessary annual spending by the end of fiscal 2028. For perspective, the analyst community expects the company to earn $1.86 billion this year.

Perhaps the most compelling reason to step into this stock while it's down, however, is the cyclical swing that's not evident yet, but sure to be brewing. That's a rebound of the broad beer business driven by rekindled economic strength. If there's one thing veteran investors know, it's that everything ebbs and flows, including different categories of consumer goods. These same veteran investors also know the turnaround often takes shape with little to no warning.

In the meantime, newcomers will be plugging into this stock while its forward-looking dividend yield stands at just over 3%. That's not a bad way to start out a new trade.

More reward than risk

This is certainly no guarantee that Constellation Brands shares are ready to soar. There's no guarantee that they've even hit their ultimate low. There's risk here, to be sure.

With a forward-looking price-to-earnings ratio of less than 20 for a company that's usually profitable though, most of any risk has likely been wrung out. It may not be your highest-growth prospect, but it's certainly not your most dangerous.

More than anything, you're buying into one of the highest-quality companies in an industry with proven long-term staying power. Alcohol's current headwind isn't going to last forever. You'll want to dive in during the headwind when the stock's beaten up -- not after the recovery is well underway.

This might help. Although the stock's been a poor performer for a while, the analyst community isn't discouraged. They're actually becoming more bullish. Most of them are calling Constellation a buy, with a consensus price target of $169. That's 28% above the stock's present price, which isn't a bad way to start out a new trade.