This has been another great year for the broader stock market, with the S&P 500 up 14% year-to-date (YTD). Costco Wholesale (COST +0.78%) shareholders are used to doing even better than the index, with the stock having trounced the S&P 500 over the last five, 10, and 20 years.

But this year is different. At the time of this writing, Costco shares are down 3.3% year to date. You'd have to go all the way back to 2002 to find a year in which Costco underperformed the S&P 500 by a similar margin. Here's why Costco is out of favor, and whether the blue chip stock is worth buying now.

Image source: Getty Images.

Costco is masterfully navigating a challenging operating environment

Costco and Walmart have been growing sales and earnings at a moderate rate. But many other retailers are struggling, from Target to Home Depot, as consumers address cost-of-living increases. Costco is well-positioned to capitalize on the shift to value. The company has razor-thin margins and brilliant marketing, from its $1.50 hot dog/soda combo to various perks for members, including car services, eye care, insurance, and more.

On merchandise alone (excluding membership fees), Costco converts less than 2% of its revenue into operating income, indicating that it offers customers a compelling value. This is part of the reason Costco has such high customer loyalty and membership renewal rates. With such reliable cash flow, Costco can regularly open new stores and expand -- regardless of the state of the economy. But even Costco isn't immune to a slowdown in consumer spending.

Costco's earnings spiked after it boosted membership fees, which were largely absorbed by consumers. But its latest same-store sales growth came in slightly below expectations.

Still, Costco is maintaining its highly efficient supply chain to mitigate the impacts of tariffs. A major advantage for Costco is the selection and range of its private label Kirkland Signature brand -- which includes everything from groceries to apparel and household goods. During its September earnings call, Costco said that its supply chain and Kirkland line had benefited margins across product categories.

On that same earnings call, Costco said that buyers are being choosy with their spending on discretionary items. However, there's an argument that the shift to value benefits Costco because it has numerous levers it can pull to pass along savings to its members.

NASDAQ: COST

Key Data Points

Costco's valuation is beyond overextended

Costco continues to deliver excellent results within a challenging operating environment. So the sell-off in Costco relative to the S&P 500 appears to be a no-brainer buying opportunity at first glance.

It's not. For starters, Costco shares are coming off a massive 38.8% gain in 2024. And it didn't grow earnings nearly as rapidly. So the stock was already priced to perfection heading into this year. But it gets worse. Over the past decade, Costco's stock price has grown much faster than revenue and earnings. Its valuation has expanded as a consequence.

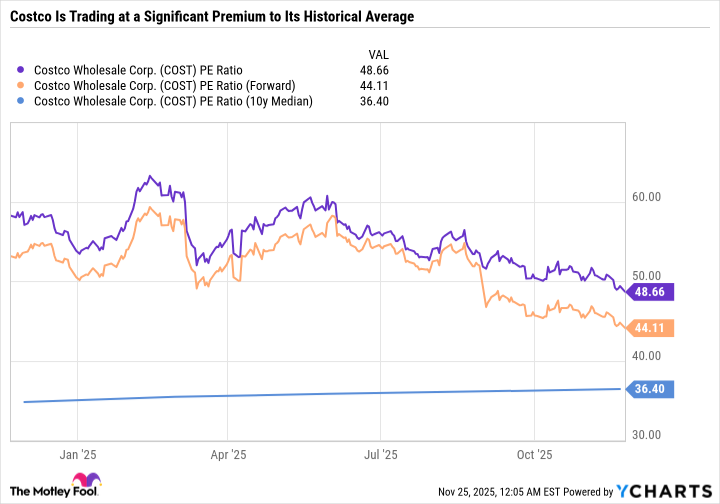

Costco's price-to-earnings (P/E) ratio is still sky-high, even when you account for the stock's poor performance this year. In fact, even judging by forward earnings, Costco is significantly overpriced relative to its 10-year median P/E, which is already high at 36.4.

COST PE Ratio data by YCharts

In fact, Costco is so pricey that its forward earnings multiple is higher than that of red-hot artificial intelligence (AI) growth stocks like Nvidia and Broadcom.

There are better buys than Costco for 2026

Costco is one of the best-run retailers in the world. Unfortunately for investors considering the stock, Costco is so expensive that it could limit its potential return, even for patient investors.

The retailer is also not a great source of passive income with a dividend yield of just 0.6%. It's true that Costco has historically paid one-time special dividends every few years, which can boost the annual payout to a couple of percentage points during those periods.

All told, Costco isn't a good buy for 2026. Investors are better off with growth stocks with reasonable valuations or value stocks like Coca-Cola (KO 0.06%) and PepsiCo (PEP 0.17%) -- two Dividend Kings that have boosted their dividends for 63 and 53 consecutive years, respectively.

Coke and Pepsi have several category-leading brands and international exposure, making them excellent buys for risk-averse investors. Coke yields 2.8%, and Pepsi yields 3.9%.