Citigroup (C +0.60%) is performing well as a business right now. But does that make this large and well-known bank a buy? The answer is no; you also need to consider the price you are paying for the stock. Here's a quick look at why you might want to buy Citigroup, and why you might not.

Citigroup is in rally mode

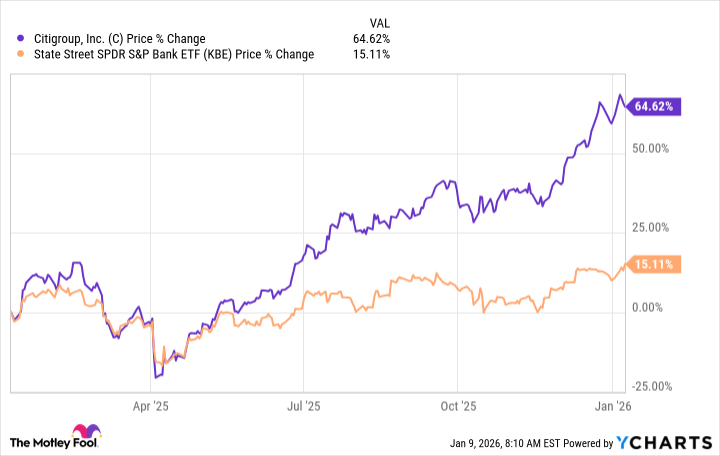

Citigroup's stock has risen 65% during the past year. That compares to a 15% increase in SPDR S&P Bank ETF, which tracks large U.S. banks.

As the chart highlights, Citigroup's outperformance began during the 2025 second quarter.

Citigroup reported first-quarter 2025 earnings last April. In that quarter, the company reported that earnings per share (EPS) increased to $1.96, up from $1.58 in the first quarter of 2024. That's a 24% increase, which is substantial by any measure. Helping things along was a 300-basis point improvement in the company's return on average tangible common equity, a key measure of a bank's performance.

Given the year-over-year improvement, it isn't surprising that investors were optimistic about Citigroup's stock. It followed that quarter with 29% EPS share growth in the second quarter and 23% growth in the third quarter.

Again, it isn't shocking that the rally in Citigroup's share price continued through to the end of the year, given the strong results at the bottom of the income statement.

Image source: Getty Images.

Is Citigroup worth buying now?

In hindsight, it would have been a great investment decision to buy Citigroup at the start of 2025. But what about at the start of 2026, after the stock has outperformed the average bank by such a wide margin? The answer is actually less clear than you might think, particularly if you have a growth at a reasonable price (GARP) focus.

Citigroup isn't nearly as cheap as it has been from a valuation perspective. The price-to-earnings (P/E) ratio is currently 17, compared to a five-year average of roughly 9. The price-to-book (P/B) value ratio is about 1.1 times the five-year average of roughly 0.6. If you compare the stock to its own history, it looks expensive.

However, a comparison to the average bank, using the SPDR S&P Bank ETF as an industry proxy, changes the equation slightly. The SPDR S&P Bank ETF's average P/E ratio is about 12.5 and the average P/B ratio is 1.3. While Citigroup's P/E ratio is above the average, its P/B ratio is below the industry average. Meanwhile, the average dividend yield for a bank is about 2.5% compared to Citigroup's yield of 2%.

NYSE: C

Key Data Points

For the most part, Citigroup still looks relatively expensive compared to the average bank. If you have a value focus, you will probably want to avoid Citigroup. However, Citigroup is performing exceptionally well right now. If you are a GARP investor, it might be worth paying a little bit more for what appears to be an outperforming bank.

Still, it will take strong execution to sustain the company's growth story. It isn't impossible, but investors will want to closely monitor the company's quarterly results after the significant price advance. It is also important to note that year-over-year earnings comparisons will be much more challenging in 2026, given the significant advances made in 2025. Even GARP investors should probably tread with caution at this point.

Most will probably be better off avoiding Citigroup

If you believe Citigroup's financial results can keep growing at a rate close to the current one, you might want to consider buying it. However, go in recognizing that the stock's valuation has risen materially during the past year. Citigroup will likely not interest value investors now that its valuation is on par with, or slightly higher than, the average bank.

It is more appropriate for GARP investors, but even then, you need to think carefully about how likely it is that the bank's EPS will increase at 20% or more each quarter in 2026. Investors should be prepared for full-year 2026 results to be less impressive than they may be hoping.