The S&P 500 marched on to its third consecutive annual gain in 2025, but one of the country's market leaders missed out on this momentum. I'm talking about UnitedHealth Group (UNH 0.49%), the U.S.' biggest health insurer. The company faced more than its share of headwinds, from the unexpected departure of its chief executive officer to a probe into its Medicare billing practices.

UnitedHealth's earnings also suffered last year, as the company underestimated the rising cost of care and patients' increased use of services. All of this weighed on demand for the stock, and as a result, UnitedHealth shares finished the year with a 34% decline.

But this healthcare giant hasn't been sitting still and instead has taken measures to address problems and generate results. Should you buy shares of UnitedHealth in January? Let's find out.

Image source: Getty Images.

A probe into billing processes

As mentioned, UnitedHealth has met with various challenges over the past year. One that stands out is the U.S. probe into the company's Medicare billing processes. Just this week, The Wall Street Journal reported that a Senate report says UnitedHealth used aggressive practices to increase Medicare payments.

UnitedHealth hasn't commented on that report yet. But the company has taken action to address headwinds in recent months, so there's reason to be optimistic about what's ahead. For example, Steve Hemsley, who took over as CEO in May, commissioned an independent assessment of the company's processes across departments.

In December, he wrote a letter to shareholders that the review found the company's practices "robust, rigorous and generally sound," but also made recommendations to strengthen them further. Hemsley said this work is "well underway."

Meanwhile, UnitedHealth has also taken steps to improve earnings. The company has exited certain plans, made adjustments to benefits, launched a repricing effort, and increased the adoption of artificial intelligence to streamline operations. All of this helped the insurer report 12% revenue growth in the latest quarter and raise its full-year earnings forecast to $14.90 per share. That's up from the earlier forecast of $14.65 per share.

Sustainable growth just ahead

UnitedHealth expects some headwinds to persist this year, especially in the context of the government's cuts to Medicare in recent years. But the company aims to deliver solid growth in earnings in 2026, and Hemsley predicts "sustainable double-digit growth beginning in 2027 and advancing from there."

NYSE: UNH

Key Data Points

Now, let's return to our question: Considering all of this, is UnitedHealth a buy in January? It's unlikely that UnitedHealth's troubles will disappear overnight. The U.S. government probe into its billing practices isn't over and may represent a hurdle for stock price performance -- some investors may see the stock as too risky until this issue is resolved. And the path to earnings improvement may not be linear, though there is reason to be encouraged by the steps the company has taken and the results it is seeing so far.

A long-term view

When looking at UnitedHealth -- or any stock -- it's important to step back and take a long-term view. And here we can see that, though the company may be traveling through a rough patch, it's well-positioned to deliver growth over time. Thanks to its leadership position as well as its two businesses -- UnitedHealthcare insurance and the Optum services unit -- the company has a significant moat, or competitive advantage. It would be difficult for a rival to construct a similar empire and unseat this player.

Meanwhile, Hemsley has been proactive since taking on the CEO role. And it's important to remember that he's not new at this -- he held the same role from 2006 through 2017 and knows the company well, so he's the ideal candidate to lead this turnaround.

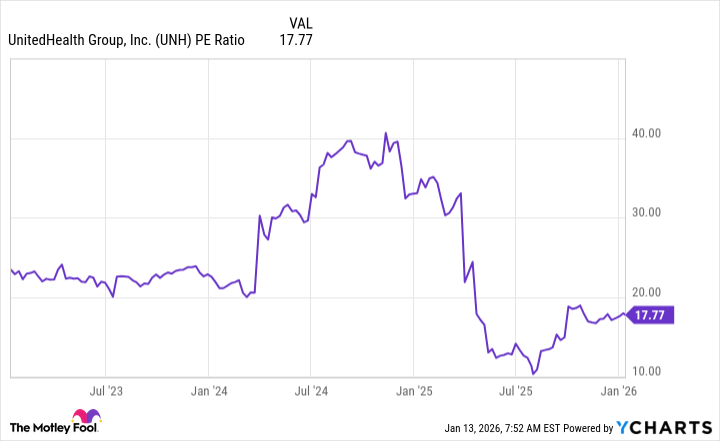

Finally, it's worth looking at valuation, and here we see that UnitedHealth is trading for 17x trailing 12-month earnings.

UNH PE Ratio data by YCharts

This valuation level is well below what we've seen over the past three years. So the stock looks reasonably priced considering the recovery steps being taken now, the progress the company has made in recent months, and the long-term opportunity.

All of this means that, right now in January, for investors who can accept the uncertainties I mentioned above, UnitedHealth is a great recovery story stock to buy and hold for the long term as this story unfolds.