Palantir Technologies (PLTR +1.25%) has offered just about everything growth investors are looking for in recent years. The tech company has delivered double-digit revenue growth -- and reached profitability and even increased it. Importantly, Palantir has spoken of great demand, particularly among commercial customers, and these customers may lead a new wave of growth over the coming years.

All of this spurred investors to pile into the stock, and as a result, it soared 2,400% over three years. But amid all of these positive points lies a negative one. This momentum helped push Palantir stock to sky-high valuation levels. Investors and analysts have worried about this, considering the levels unsustainable.

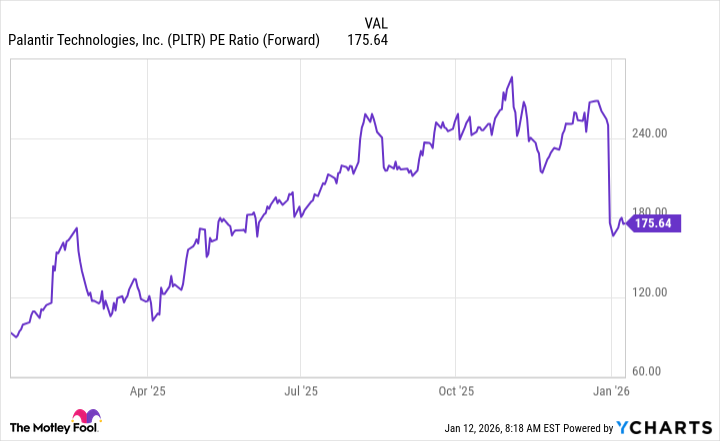

Though valuation remains high, it's fallen nearly 40% from a peak in November. Is Palantir a buy now in 2026? Let's find out.

Image source: Getty Images.

Palantir's software

First, let's consider how this 20-year-old company roared into the center of the scene over just the past few years. In its early days, Palantir was mainly known for its government contracts, and these drove the company's development and growth. Palantir's software platforms help customers aggregate difficult-to-access data, analyze it, and put it to work.

In recent years, though, another customer has emerged and may represent the growth driver of the future. I'm talking about the commercial customer. Palantir only had 14 U.S. commercial customers just a few years ago, and then the launch of its Artificial Intelligence Platform (AIP) supercharged momentum here. AIP offers customers a way to almost instantly apply AI to their problems and develop game-changing solutions.

The timing was right, as today, companies are eager to get in on AI -- it's a technology that could make them more efficient and innovative, and eventually support significant earnings growth. And Palantir offers customers a way to easily seize this opportunity.

NASDAQ: PLTR

Key Data Points

More growth ahead

All of this has translated into impressive earnings performance. In recent quarters, revenue has climbed in the double-digits in both the government and commercial businesses. And the commercial business offers us clear signs that more growth may be ahead. The number of commercial customers has reached into the hundreds, which shows growth but also offers plenty of room for customer acquisition. Contract values are soaring, suggesting customers are going all in on their work with Palantir. For example, in the recent quarter, U.S. commercial total contract value surged more than 300% to $1.3 billion, a record.

Finally, a key point to note is that Palantir is balancing this growth with profitability. In software, this feat is measured by the Rule of 40, with a score of 40% or higher showing the company is successful here. Palantir's score has been steadily growing, well past 40% in recent quarters, and the latest reading is 114%. So that's a big reason to be optimistic about Palantir in the future.

Your investment strategy

Now, let's return to our question: Is Palantir a buy now that valuation has come down? This depends on your investment strategy. If you're a cautious or value investor, Palantir probably isn't the right choice for you right now. The stock, even after a dip in valuation, remains expensive according to commonly used metrics.

PLTR PE Ratio (Forward) data by YCharts

But if you're a growth investor, you may look at this situation differently. Palantir has built out its technology over a number of years, and its software systems have proven their usefulness. Now, as customers aim to incorporate AI into their businesses, Palantir offers an ideal way to do just that. The company is generating impressive growth, but earnings figures, with quarterly revenue of nearly $1.2 billion and GAAP net income of $476 million, leave room for additional gains now and down the road.

All of this means that, even if the stock looks pricey right now, Palantir could grow into its valuation over time. So, for long-term growth investors, it's a great idea to buy Palantir on the dip in 2026.