In 2020, ride-hailing and food delivery giant Uber Technologies acquired a company called Postmates, and in 2021, it spun Postmates' robotics division off as a separate company: Serve Robotics (SERV +0.89%).

Serve has become a leading developer of autonomous last-mile logistics solutions, and it's currently building thousands of its latest Gen 3 robots -- small delivery systems that travel on sidewalks -- to deploy in the Uber Eats food delivery network. Citing an estimate by Cathie Wood's Ark Investment Management, Serve believes the largely untapped market for robotic and drone delivery could be worth a whopping $450 billion by 2030.

Serve stock declined by 23% last year, but it has already soared by 40% in the first few weeks of 2026. Now trading 8% above where it began 2025, is it still a buy?

Image source: Getty Images.

Serve's deal with Uber Eats is a game changer

Serve believes existing last-mile logistics solutions are inefficient because they rely on cars with human drivers to deliver small commercial orders from restaurants and retailers. In fact, the median distance traveled during a food delivery in the U.S. is just 2.5 miles, so Serve thinks small robots and drones would be better suited to the task.

Around 3,600 restaurants in five U.S. cities have used Serve's robots to deliver more than 100,000 food orders since 2022. Powered by Nvidia's Jetson Orin hardware and software, Serve's latest robots have achieved Level 4 autonomy, which means they can safely drive on sidewalks (at a maximum speed of 11 miles per hour) within designated areas without human intervention.

Serve thinks it can bring costs down to just $1 per delivery as its Gen 3 lineup scales. That's far lower than the cost of any existing human-driven solution. The company's deal with Uber Eats will go a long way toward helping it work toward that target, because it requires the deployment of 2,000 robots across several U.S. cities, including Los Angeles, Atlanta, Dallas, Miami, and Chicago.

On Dec. 12, Serve announced it had built its 2,000th robot, so the company is entering 2026 at full capacity. However, in October, it also announced a new deal with DoorDash that will call for even more robots as this year progresses.

Serve's revenue is expected to soar, but there's a catch

Serve generated $1.77 million in revenue during the first three quarters of 2025, which isn't much for a company with a $1.1 billion market cap. It will report its operating results for the fourth quarter in February or March, which should take its total 2025 revenue to $2.5 million, according to management's guidance.

But management predicts Serve's revenue will explode tenfold in 2026 with 2,000 active robots in its fleet, so this could be the company's biggest year so far.

NASDAQ: SERV

Key Data Points

However, scaling a robotics business isn't cheap, and even a tenfold increase in revenue won't be enough to offset Serve's ballooning costs. Its total operating expenses were $63.7 million during the first three quarters of 2025, more than twice as much as the prior-year period, when they were $25.3 million.

Because of Serve's minuscule revenue, those costs resulted in a $67 million loss on the bottom line during the first three quarters of 2025, so its full-year loss is almost certain to eclipse its 2024 loss of $39.2 million.

The company had $210 million in cash on hand as of Sept. 30, so it can afford to operate at a loss for now. However, if it doesn't achieve profitability in the next couple of years, it might have to raise more money with secondary stock offerings, diluting its existing shareholders.

Is Serve stock a buy in 2026?

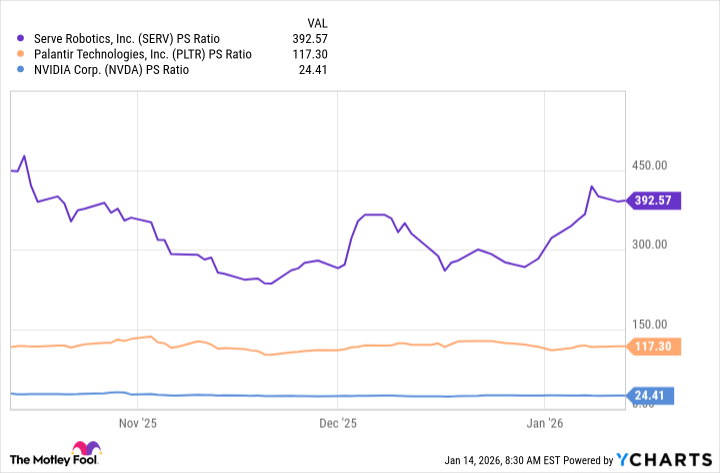

Serve stock is trading at a price-to-sales (P/S) ratio of 392 as I write this, which is wildly expensive. For some perspective, Nvidia's P/S ratio is just 24, and it's arguably the highest-quality hardware company in the artificial intelligence and robotics space.

Serve even makes Palantir Technologies' P/S ratio of 117 seem relatively reasonable, when it's actually extremely expensive in its own right.

SERV PS Ratio data by YCharts.

With all of that said, if we assume Serve's revenue will soar tenfold during 2026 to around $25 million, then its forward P/S ratio at today's share price would be 44 -- a little more reasonable, although still not cheap. Further, if robotic and drone delivery really does become a $450 billion opportunity by 2030 as the last-mile logistics industry shifts away from human drivers, then Serve stock is probably a bargain today.

However, robotic delivery is still a very new concept, and there is no guarantee it will scale as effectively as Serve expects. If the company's business model hits any speed bumps that result in a much slower increase in its revenue than expected this year, then its sky-high valuation leaves it highly vulnerable to another sharp decline in its stock price.

That is a legitimate risk for investors who buy the stock today, so it might be wise to keep the size of any position you open in Serve relatively small.