When it comes to leading semiconductor stocks, most investors probably don't bother looking past Nvidia, Advanced Micro Devices, and Broadcom. These three powerhouses dominate the market for AI accelerators -- graphics processing units (GPU) and custom application-specific integrated circuits (ASICs) used to develop generative AI.

While investing in chip designers has been a good proxy for the overall health of the AI landscape, a more lucrative opportunity might be hiding in plain sight. As the world's largest chip manufacturer by revenue, Taiwan Semiconductor Manufacturing (TSM 0.83%) plays an enormous role in ensuring AI chips make into data centers on time.

One of my predictions for 2026 is that Taiwan Semi will be the next member of the trillion-dollar club to reach a $2 trillion valuation. Let's unpack how TSMC can reach this milestone and assess why the stock looks like a no-brainer buy right now.

Image source: Taiwan Semiconductor Manufacturing.

What would it take for Taiwan Semi to reach a $2 trillion valuation?

Currently, Taiwan Semi has a market cap of $1.7 trillion -- making it one of the most valuable companies in the world. In order to reach a $2 trillion valuation, shares of TSMC would need to rise by another 18% this year -- or about $380 per share. Considering the stock has rallied 62% over the last 12 months, joining Amazon in the $2 trillion club looks attainable. Let's take a look at some of the company's tailwinds that support further valuation expansion.

How TSMC can dominate in 2026 and beyond

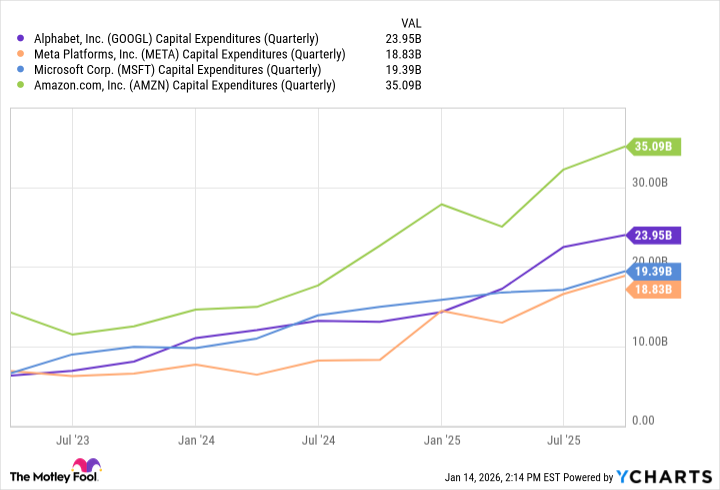

Throughout the AI revolution, hyperscalers including Alphabet, Microsoft, Meta Platforms, and Amazon have each accelerated their investments in AI capital expenditures (capex).

GOOGL Capital Expenditures (Quarterly) data by YCharts

According to consensus estimates from FactSet Research, Wall Street is expecting the hyperscalers to spend $527 billion on AI infrastructure in 2026 -- up 13% from previously issued forecasts at the beginning of the third quarter.

Taking this a step further, McKinsey & Company estimates that $5 trillion will be spent on supporting AI workloads by 2030. Translation: Appetite for training and inference (i.e., more chips) is expected to grow and accelerate among AI's largest developers for the next several years.

The obvious winners of the AI infrastructure era are companies like Nvidia, AMD, Broadcom, and Micron Technology. But behind the scenes, many of these companies are relying on Taiwan Semi to manufacture their chips in order to fulfill expanding backlog orders.

NYSE: TSM

Key Data Points

TSMC is already getting ahead of the curve as it relates to ratcheting up its foundry capabilities. The company is expanding its geographic footprint beyond Taiwan -- in particular, setting up facilities in Japan and Germany. Perhaps more importantly, however, TSMC is also considering a $300 billion expansion to its existing $165 billion infrastructure project in Arizona.

By diversifying its manufacturing expertise and doubling down on its relationship with the U.S., I think Taiwan Semi is positioning itself for even stronger relationships with its major customers. As such, I think the company is poised to continue commanding a high degree of pricing power over the competition -- fueling even further acceleration across the top line complemented by expanding profit margins.

Should you buy Taiwan Semi stock right now?

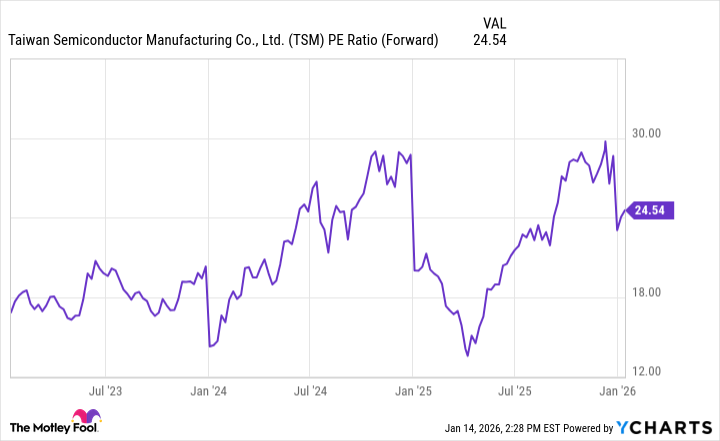

Taiwan Semi's forward price-to-earnings (P/E) multiple of 24 may not appear "cheap" upon first glance.

TSM PE Ratio (Forward) data by YCharts

The subtle nuance from the chart above is that the company is trading about 22% below its peak forward earnings levels. According to consensus estimates, sell-side analysts are anticipating TSMC to generate $13.26 in earnings per share (EPS) in 2026.

At its peak forward P/E of 30, TSMC could reach $390 per share assuming it meets analysts' earnings expectations. I think this is more than reasonable, as should the company reach or surpass these estimates, I would not be surprised to see the stock experience a meaningful rebound and propel well past a $2 trillion valuation.

To me, Taiwan Semi is one of the best examples of a pick-and-shovel opportunity tailor-made for the AI infrastructure chapter. With this in mind, I view TSMC as one of the most reasonably priced and safest AI chip stocks on the market right now relative to its growth prospects for this year and beyond.