Just as I predicted, Coca-Cola (KO +1.87%) was a better buy than Procter & Gamble (PG +1.71%) in 2025, with Coke gaining 12.3% compared to a 14.5% decline in P&G.

Coke's performance was particularly impressive considering consumer staples was the worst-performing stock market sector in 2025, with the sector sliding 1.2% compared to a 16.4% gain in the S&P 500 (^GSPC 2.06%).

Here's why Coke crushed P&G in 2025, and which dividend stock is the better buy for 2026.

Image source: Getty Images.

Coke and P&G have a similar recipe for success

When it comes to passive income powerhouses, Coke and P&G are 1A and 1B. Coke has 63 consecutive years of boosting its payout compared to 69 years for P&G -- making both stocks some of the longest-tenured Dividend Kings -- an elite group of companies that have grown their dividends for more than 50 consecutive years.

Coke and P&G both have impeccable supply chains and global brand recognition. Coke's network of bottling partners allows it to maintain high margins. Corporate Coke produces syrups and concentrates, which its bottling partners use to manufacture, package, merchandise, and distribute its products. In this vein, Coke maintains high operational flexibility across global markets, which can help it withstand region-specific slowdowns.

Similarly, P&G has industry-leading margins due to its size, global partnerships, and elite portfolio of brands -- many of which are category leading.

High margins allow Coke and P&G to convert more revenue into operating income than their peers, thereby maximizing earnings and supporting dividend growth.

NYSE: KO

Key Data Points

Coke has a more concentrated brand portfolio than P&G

Despite being similar on paper, the two companies differ significantly in their capital allocation. Coke has favored mergers and acquisitions over P&G in recent years -- acquiring key brands like BodyArmor, Fairlife, Topo Chico, and Costa Coffee to become a well-rounded non-alcoholic beverage company and reduce its reliance on soda. P&G has preferred to innovate within its existing brand portfolio through innovation and marketing efforts to drive loyalty.

Despite Coke's investments, it still relies heavily on its flagship Coca-Cola brand, with trademark Coca-Cola accounting for 42% of 2024 U.S. unit case volume compared to 48% of non-U.S. unit case volume. P&G has core brands too -- like Gillette, Tide, Pampers, Crest, Dawn, Olay, Febreze, Bounty, and Charmin. But it doesn't have that dominating brand like Coke.

Diversification can be a strength, but in recent years, Coke's concentration on a few key brands was an advantage, as it was better prepared to absorb and pass along rising costs to consumers than P&G.

For full-year 2025, Coke is guiding for non-generally accepted accounting principles (non-GAAP) organic revenue growth of 5% to 6%. P&G grew organic sales by just 2% in fiscal 2025 (ended June 30, 2025) and is guiding for 0% to 4% organic revenue growth for fiscal 2026.

NYSE: PG

Key Data Points

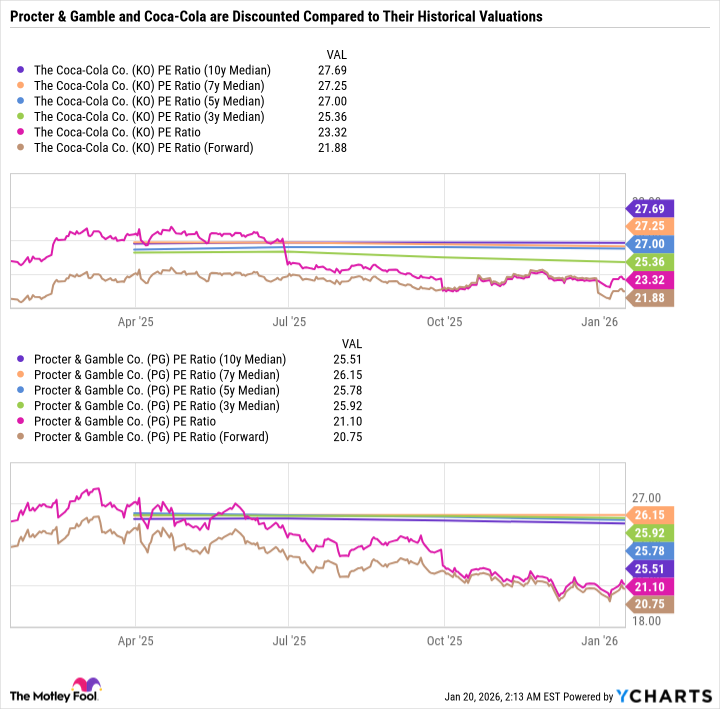

Coke and P&G are great values

Heading into 2025, Coke was a much better value than P&G, especially given its high margins. Throughout the year, Coke did an excellent job maintaining or slightly increasing volume while demonstrating impeccable pricing power.

The narrative has flipped for 2026, as P&G is the better value. But both P&G and Coke are trading below their historical valuations, as reflected in both price-to-earnings and forward P/E ratios.

KO PE Ratio (10y Median) data by YCharts

However, given the slowdown in earnings from both companies, the discount is warranted.

After P&G's sell-off last year compared to Coke's modest gain, both stocks are solid buys in 2026. Especially for income investors looking to boost their passive income streams.