Taiwan Semiconductor Manufacturing (TSM +0.38%) was one of the best stocks to own in 2025 -- it rose over 50%. But 2026 is a new year. None of the stock's success from last year matters, although its business success will still carry over.

The biggest item investors are counting on in 2026 for Taiwan Semiconductor (or TSMC) is to maintain the momentum that drove it higher in 2025. With the tailwinds blowing in the AI space, I think that appears to be a safe bet.

Taiwan Semiconductor recently reported fourth-quarter earnings, and management gave some bullish guidance for 2026 and beyond. I think it's a clear sign to buy the stock now, as the market still isn't fully valuing the stock for how dominant it is.

Image source: Taiwan Semiconductor.

TSMC is at the heart of the AI computing buildout

It's no secret that artificial intelligence requires an incredible amount of computing power. So it requires a lot of computing hardware to accomplish that task. Regardless of what computing unit is used to train and run AI models, they are all filled with chips that come from relatively few foundries.

The largest in the world, by far, is Taiwan Semiconductor. It's the key logic chip supplier for many companies, including Nvidia and Apple. So, when there is insatiable demand for computing power in an area like AI, TSMC will naturally do well. Its Q4 results confirmed this and ensured that the AI race is still going full bore.

NYSE: TSM

Key Data Points

In Q4, Taiwan Semiconductor's revenue rose 26% year over year in U.S. dollars. This shows strong, sustained gains, but TSMC isn't stopping there. For 2026, it expects revenue to increase by nearly 30% in U.S. dollars. This shows that AI demand for chips is real and slated to continue growing in 2026, but that's not the end of it. For the five years starting in 2024 and ending in 2029, TSMC now expects that its compound annual growth rate (CAGR) will be about 25%.

A 25% CAGR for a company the size of Taiwan Semiconductor is nearly unheard of, but it shows how massive the demand for logic chips is. As a result, TSMC can be viewed as not only a great investment for 2026, but also for a few years down the road. Despite its success, Taiwan Semiconductor is still one of the great values in the market.

Taiwan Semiconductor still trades at a discount to big tech

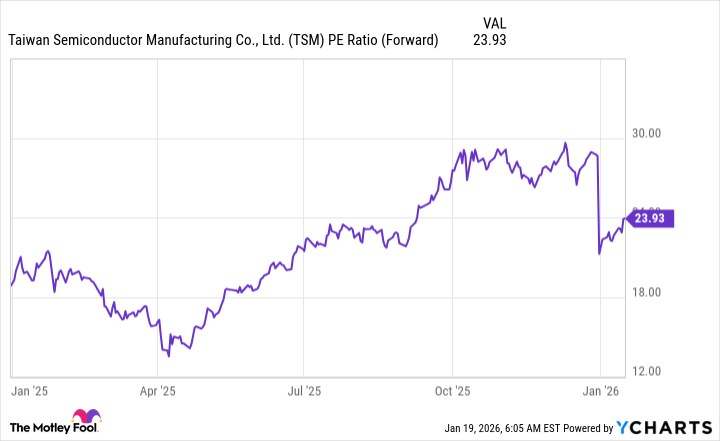

Most big tech companies trade at about 30 times forward earnings. (Nvidia gets a premium to that, due to its rapid growth.) However, none of these companies will come close to delivering 30% revenue growth in 2026. Taiwan Semiconductor should easily hit that threshold, yet it trades for 24 times forward earnings.

TSM PE Ratio (Forward) data by YCharts.

For reference, the S&P 500 trades for 22.3 times forward earnings. While Taiwan Semiconductor trades at a slight premium to the broader market, the market isn't putting up growth anywhere close to TSMC's. As a result, I think that investors can declare its stock rather cheap.

It's not often that you can scoop up a stock with a clearly defined growth case, trading at a cheaper price tag than where it should. But that's exactly where Taiwan Semiconductor is right now. I believe it's one of the best stocks to buy now and hold for the next few years, as it's a great "picks and shovels" play for the generative AI buildout. With AI spending expected to stay strong over the next five years, I can think of few better stocks positioned to take advantage of the massive AI spending spree than Taiwan Semiconductor.