Long-time Tesla (TSLA +0.16%) investors can attest to just how much of a roller-coaster ride it's been for shareholders. After losing over 40% of its value from January 2025 to April 2025, the stock finished the year strong, up around 11.4%.

Although Tesla underperformed the S&P 500, it was a much better performance than many anticipated mid-year. It didn't come without disappointing news at the end of the year, though.

Image source: Tesla.

A core business headed in the wrong direction

Unfortunately, 2025 was a record-breaking year for Tesla for all the wrong reasons. The company only delivered around 1.63 million vehicles in the year, 8.5% fewer than in 2024. This was the biggest year-over-year drop in its history.

In the fourth quarter, deliveries fell 16% year over year, and for the first time ever, it's no longer the world's top electric vehicle (EV) seller. That distinction now goes to Chinese automaker BYD, which sold around 2.26 million battery EVs in 2025.

Part of the reason for the decline is the emergence of lower-cost options around the world (such as BYD and Geely), as well as the expiration of government tax credits that had lowered Tesla prices for many consumers. The $7,500 U.S. federal EV tax credit expired at the end of September 2025.

NASDAQ: TSLA

Key Data Points

Tesla's future rides on robotaxis becoming a thing

Auto sales account for close to three-fourths of Tesla's revenue, but its long-term investment case hinges on the company's ability to deliver on its robotaxi ambitions. In an ideal world, robotaxis would give Tesla a high-margin business that operates more like a software company than an automaker.

Unfortunately, the stock is priced as an artificial intelligence (AI) company and as if robotaxi commercialization is guaranteed, though that's far from the case. Which brings us to the next point.

Tesla's stock is trading beyond a premium

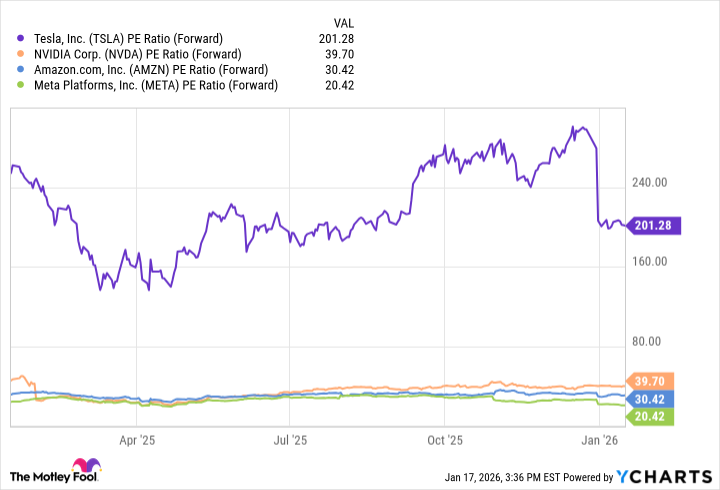

Even with the question mark surrounding Tesla's current core business, the stock is extremely expensive, currently trading at 201 times its projected earnings over the next 12 months. For perspective, that's more than five times higher than Nvidia, more than 6.5 times higher than Amazon, and nearly 10 times higher than Meta.

TSLA PE Ratio (Forward) data by YCharts.

Trading that expensively means investors are pricing a lot of growth into Tesla's stock, but its current business performance far from justifies it. Even with meaningful robotaxi progress, it would be extremely hard to justify Tesla's current valuation.

If you're thinking of investing in Tesla, be prepared to wait years (like 10 or more) for its autonomous vehicle plans to become tangible and for the inevitable high volatility along the way.