Apple (AAPL 0.15%) has proven its ability to sell great products that customers return to year after year. The company's iPhone, Mac, and other devices have helped propel earnings into the billions. All of this has helped Apple stock score a win for investors over time, with the shares climbing more than 900% over the past decade, for example. So Apple has been a fantastic long-term investment.

But, in recent times, Apple has generated lower returns for investors than many other technology stocks. This is for a couple of reasons. Apple didn't rush to get in on the high-growth area of artificial intelligence (AI) and instead took a slower approach than its tech peers. So, investors aiming to bet on AI didn't necessarily flock to Apple. And for part of last year, investors worried that Apple -- with much of its iPhone production in China -- would face significant import tariffs.

Today, though, Apple is progressing with its AI rollout, and tariff concerns have eased. (The U.S. said it would offer exemptions to tech players that invested in U.S. production -- something that Apple is doing.)

Considering all of this, where will Apple stock be in a year? Let's find out.

Image source: Getty Images.

Apple vs Samsung

So, first, let's consider the Apple story so far. As mentioned, the company built leadership over time, and its iPhone stands out as a flagship product that keeps customers loyal. Apple, neck-and-neck with Samsung over the previous two years, slipped ahead in 2025 to finish the year with the greatest share of the smartphone market, at 20%, according to Counterpoint Research. And the company's 10% growth in shipments well surpassed rivals' -- Samsung delivered 5% growth while the others came in with lower figures, the research showed.

This is key because it illustrates the strength of Apple's moat, or competitive advantage. The company's brand is so strong that fans stick with it, are willing to wait for updates, and even pay a higher price than they might for a rival smartphone. Moats are fantastic because they may ensure revenue growth moving forward.

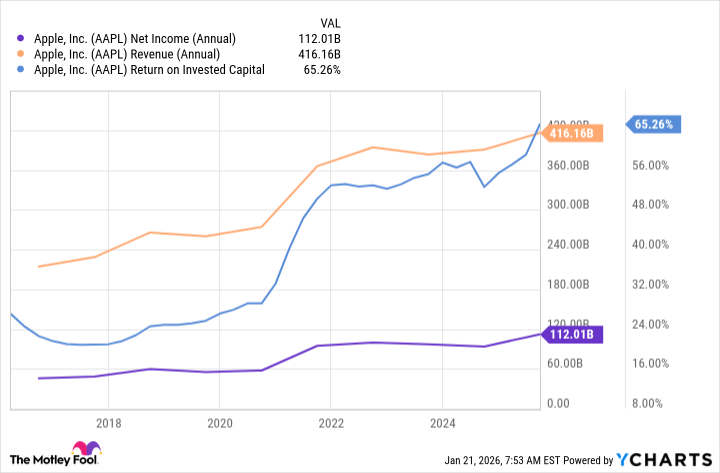

This market position has helped Apple's earnings steadily climb, and return on invested capital (ROIC) also has advanced.

AAPL Net Income (Annual) data by YCharts

The increase in ROIC shows Apple is making smart investment decisions as the company has gone on to benefit from the cash it's spent on its business.

Underperforming the S&P 500

Last year, though, as investors aimed to benefit from AI growth, Apple probably wasn't the first name on their "buy" lists. The stock finished the year with an 8% increase, underperforming the S&P 500.

NASDAQ: AAPL

Key Data Points

But we may expect catalysts for positive performance this year. Apple has rolled out some AI features across its devices, but there is more to come. During Apple's latest earnings call, chief executive officer Tim Cook said the company aims to release the much-awaited version of Siri, Apple's virtual assistant, this year.

Just recently, Apple announced a deal with Alphabet, saying it would use the tech giant's Gemini large language model (LLM) to power the new version of Siri. Gemini is a popular LLM that Alphabet uses across its platforms and offers to customers through its Google Cloud business.

Apple's foldable smartphone

Another potential catalyst for Apple this year may be the release of its first foldable iPhone. The company might launch millions of them this year at a price of about $2,000, according to Citi analyst Atif Malik. And the analyst expects Apple to ship 20 million units next year.

Finally, Apple's sales trends and booming services business are reasons to be optimistic about the company's growth in the coming quarters. In the most recent quarter, for example, Apple reported record September quarter revenue, and services revenue reached its highest level ever.

Wall Street expects Apple stock to increase about 16% over the coming 12 months -- this is according to the average analyst estimate. Considering all of the points I mentioned above, and the fact that Apple trades for a reasonable 29x forward earnings estimates, the stock has plenty of room to run. And that means it could very easily advance in the double digits in 2026.