With ongoing geopolitical conflicts, trade wars, interest rate uncertainty, and more, is now really the time to be investing in stocks? In my experience, there are always reasons for pessimism. But regularly adding new money to stock investments has historically always been part of a winning philosophy.

For this reason, I'm always on the lookout for stocks to add to my own portfolio. And cosmetics company e.l.f. Beauty (ELF +0.76%) might be one that I buy in 2026.

Image source: Getty Images.

From a business perspective, I like e.l.f. Beauty for multiple reasons. First, I like the company's revenue growth. As of its fiscal second quarter of 2026 (which ended in September), the company has grown net sales for 27 consecutive quarters, taking market share from larger players. And management expects 18% to 20% top-line growth for the current fiscal year.

E.l.f. Beauty is growing by being a low-cost leader in cosmetics. The average price for its products is $7.50 compared to $9.50 for comparable mass-market brands. Management implemented a $1 price increase in August, but that still leaves consumers with an incentive to buy its products.

NYSE: ELF

Key Data Points

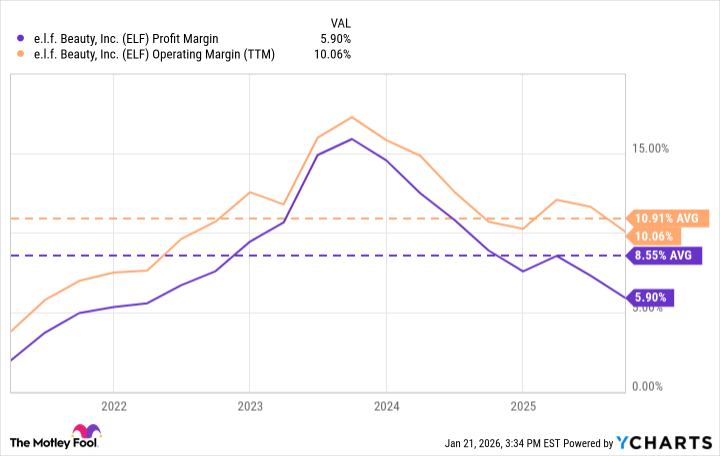

The impressive thing to me regarding e.l.f. Beauty is that it offers lower prices, yet its profit margins remain attractive. Investors shouldn't expect tech margins here. But its five-year average operating margin is about 11%, and its average profit margin is about 9%.

ELF Profit Margin data by YCharts

The constant volatility with tariffs is impacting e.l.f. Beauty's margins for now -- most of its products are made in China. But profits are still respectable. And the price increase will help mitigate the pressure it's feeling.

With only $1.4 billion in trailing-12-month revenue, e.l.f. Beauty still has a lot of runway for growth, which is why I like it for the long term.

What else investors should know

I started this article by pointing out that I might buy e.l.f. Beauty stock this year, implying that I might not. And it's true, my mind isn't made up. This is just one of several companies that I'm considering for my portfolio, and I'm not sure which one I like best yet.

Even if I don't buy e.l.f. Beauty stock this year, I still find the investment thesis compelling, which is why it's on my list in the first place.

E.l.f. Beauty stock is down more than 50% from its 2024 high. By highlighting this company, I'm not saying the bottom is in. To the contrary, stocks can always fall more. And it's unlikely that this is the only 50% drawdown that it will ever have.

This is a good reminder that stocks can be volatile, even good stocks. This is why it's important to hold through market volatility -- you don't want to sell before the bounce-back.

Personally, I've found that investing in companies you love helps you hold on during the hard times. This is another reason I'm considering e.l.f. Beauty stock. While I'm not a user of its products myself, multiple people in my house are, and they would love to see this beautiful growth stock added to our investment portfolio.