The artificial intelligence (AI) boom has made plenty of winners for investors, but over the last few months, it's been hard to beat Micron (MU +10.95%), the memory-chip specialist that has benefited from soaring demand for the high-bandwidth memory (HBM) chips used in data centers for AI applications.

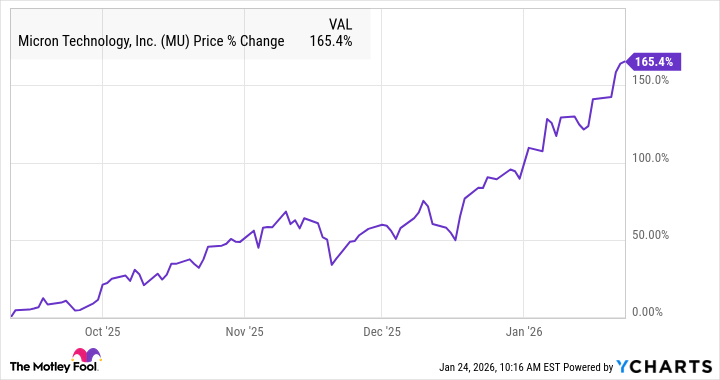

Over the last three months, Micron has nearly doubled, jumping 93%. In fact, since I made this prediction last September, calling for the stock to soar over the next three years, the shares are up 165%, and as the chart below shows, they have been scorching hot into 2026.

Why Micron has nearly tripled since then

There's a supply crunch happening in the memory subsector, which has exacerbated in the last few months, leading to a surge in prices, and making the major players in memory soar, including Samsung, SK Hynix, and even Sandisk, a smaller company that focuses on less advanced flash memory products, rather than HBM.

Micron spelled out these industry dynamics in its latest earnings report in December, noting that the $100 billion HBM total addressable market (TAM) milestone in the industry is now expected to arrive in 2028, two years earlier than it previously expected. Management also called for a compound annual growth rate of 40% in HBM through 2028, which should assuage concerns about the cyclicality of the memory sector as supply shortages can shift to gluts, leading to tumbling prices.

Micron also smashed expectations with its guidance in that report, showing that Wall Street had significantly underestimated its growth and margin expansion. For its fiscal second quarter, it called for revenue around $18.7 billion, well ahead of the consensus at $14.3 billion, and it forecast earnings per share at a midpoint of $8.42, nearly double expectations at $4.71.

Image source: Getty Images.

Is Micron still a buy?

As the forecast above shows, Micron expects the strong industry dynamics and demand growth to persist at least through 2028, and it's already contracted out its HBM supply for 2026, which should support further growth in the cycle.

Intel just reminded investors in its fourth-quarter report on Thursday that it's on the other end of the memory shortage, hampering its growth in 2026, a dynamic that clearly favors Micron and its peers.

Micron is also still being valued like a high-risk, cyclical stock as it trades at a forward P/E of just 12 based on the consensus for fiscal 2026.

With that low price tag and no signs of the memory shortage abating in the AI boom, Micron continues to look like a strong buy for 2026.