The questions on everyone's mind in the artificial intelligence (AI) investing sector are along the lines of: Is AI demand real, and is there a bubble forming? This is a very important question, because many companies are pouring hundreds of billions of dollars into this technology. Most of the AI hyperscalers would say that they haven't brought enough computing capacity online to do what they want. So, spending looks set to continue.

One company is at the center of all of this spending: Taiwan Semiconductor Manufacturing (TSM +2.29%). TSMC, as it's also known, holds a massive market share in the logic chip market, and without it, AI computing wouldn't look the same. If TSMC weren't on board with the buildout, it wouldn't be increasing production capacity to meet demand. However, it just gave investors 56 billion reasons why AI demand.

I think investors should consider scooping up the stock as a result.

Image source: Getty Images.

Taiwan Semiconductor's CEO is nervous about AI demand

Just because TSMC is excited about artificial intelligence chip demand doesn't mean it's not also cautious. During its fourth-quarter conference call, CEO C.C. Wei stated that he's "very nervous" about AI demand.

That doesn't seem like a great stance to take when you're the CEO of the primary chip manufacturer for AI, but Wei followed that up with a caveat. He went on to say that TSMC is about to invest up to $56 billion in capital expenditures to meet that demand. So, his nervousness comes from the stance of having to spend a ton of money to meet the demand.

This is healthy skepticism, but he's done due diligence with his primary clients over the past few months to understand if the long-term demand is there, and he concluded that it was. This makes a pretty clear case that AI demand is here to stay, and until generative AI capabilities are fully maxed out, Taiwan Semiconductor will continue to be at the center of the movement.

NYSE: TSM

Key Data Points

Taiwan Semi's stock still trades at a discount to big tech

Although Taiwan Semiconductor's stock has been on a phenomenal run since the AI race started in 2023 (it's up over 300% since then), I think it's just getting started.

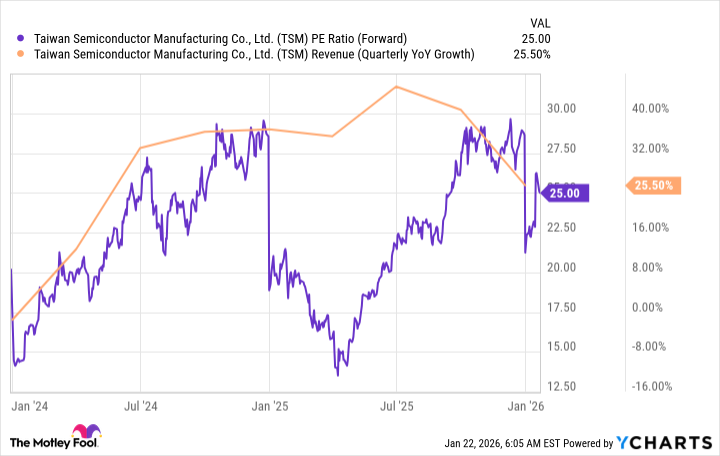

Most big tech companies trade for about 30 times forward earnings in today's market environment. Additionally, these companies are growing their revenue at about a mid-teens rate. Taiwan Semiconductor is both cheaper and growing faster, potentially making it a stronger investment. During its last quarter, its revenue rose 26% year over year, and it trades for 25 times forward earnings.

TSM PE Ratio (Forward) data by YCharts.

That's really not that much more expensive than the broader market, which trades for 22.3 times forward earnings, as measured by the S&P 500. Furthermore, that growth rate is expected to accelerate throughout the year.

Taiwan Semiconductor's guidance for 2026 was nearly 30% revenue growth, further contributing to a sustained 25% compound annual growth rate (CAGR) that it expects to deliver through 2029. The AI buildout has clearly benefited TSMC, and with its chips being the best options on the market, it will continue to thrive regardless of which company is providing the best AI computing hardware.

The biggest factor for Taiwan Semiconductor is for the AI hyperscalers to continue spending on data centers. As long as this continues, demand will stay elevated, and TSMC will continue to be a market leader. Many projections expect data center buildouts to grow through at least 2030, so there are still several years of growth left for the stock.

I think the risk of an AI bubble forming at this point is fairly minimal. While investors always need to stay diligent, I think Taiwan Semiconductor is among the best investments you can make right now.