For much of the last seven years, the bulls have been running wild on Wall Street. The benchmark S&P 500 has gained at least 16% in each of the previous three years, and for six of the last seven.

But outsize returns for Wall Street's most widely followed index don't mean all stocks have come along for the ride. Just ask investors in gig economy stock Fiverr International (FVRR 1.97%), who've watched their shares lose 95% of their value since peaking on Feb. 12, 2021.

With the stock market entering 2026 at its second priciest valuation in 155 years, according to the Shiller Price-to-Earnings (P/E) Ratio, finding bargains has become progressively more challenging. Like newly retired billionaire investor Warren Buffett, I've been selling more stocks than I've been buying for the past couple of years.

Image source: Getty Images.

However, Fiverr International's risk-versus-reward profile has shifted so far toward "reward" that not even a historically pricey stock market could keep me from recently doubling my stake.

Fiverr stock didn't lose 95% of its value by accident

Before diving into the laundry list of reasons I decided to double my position in Fiverr, it's imperative to lay the foundation for how this online services marketplace stock got to where it is now. In other words, we need to examine both sides of the coin and understand the company's inherent risks before attempting to quantify any potential reward.

One of the leading downside catalysts for Fiverr has been the end of the COVID-19 pandemic. When the global pandemic began, and workers were compelled to stay home to mitigate the spread of COVID-19, demand for freelance work exploded. But as it became clear that the worst of the pandemic was in the rearview mirror, some companies began bringing workers back into physical offices, thereby reducing the opportunities for freelancers on Fiverr's online marketplace.

NYSE: FVRR

Key Data Points

To build on this point, Fiverr has endured a multiyear decline in annual active buyers on its platform. With more workers returning to the office, annual active buyers have retraced from 4.2 million, as of Sept. 30, 2022, to 3.3 million in the comparable quarter three years later.

There have also been concerns about the role artificial intelligence (AI) will play in freelancer marketplaces like Fiverr. Generative AI solutions and large language models can handle tasks that a business would normally hire a freelancer to do. In September, Fiverr announced it would lay off 30% of its employees in an effort to double down on AI as a way to streamline its operations.

Lastly, valuation concerns have weighed on Fiverr stock. When the company's shares were trading north of $300, they commanded a triple-digit forward P/E ratio. While that's no longer the case, Fiverr's year-over-year sales growth rate has fallen from a range of 42% to 77% from 2018 through 2021 to a high-single-digit or low double-digit percentage from 2022 through 2025.

Image source: Getty Images.

Fiverr International stock may never be this cheap again

While I fully recognize and appreciate the aforementioned headwinds, the time to pounce on this historically cheap gig economy stock is now.

Even with select businesses bringing workers back into physical offices, there's been a decisive shift in how workers complete their tasks. Prior to the pandemic, around 7% of paid workdays were completed remotely. But as of 2025, this figure had quadrupled to approximately 28%. While this is down considerably from 2020, it reflects a permanent shift in the workforce, underscoring the need for freelancers and online service marketplaces like Fiverr. In short, Fiverr is ideally positioned to capitalize on this new norm.

In terms of key performance indicators, Fiverr is performing far better than its fishtailing share price would indicate. Although active buyers on the platform have declined by 21% over the last three years (as of Sept. 30, 2025), annual spend per buyer has been climbing at an even more impressive pace. Over this same time frame, annual spend per buyer has risen by 26% to $330. This would appear to indicate that remaining businesses are more engaged than ever -- and that's a good thing!

But perhaps the most impressive aspect of Fiverr's operating model is its marketplace take rate. This represents the percentage of each transaction negotiated on its platform that it gets to keep. The company charges freelancers a 20% commission on their earnings, along with a 5.5% service fee for the 3.3 million active buyers. It can generate additional marketplace revenue from seller subscriptions and Promoted Gigs, which advertise freelancer offerings on the platform.

Whereas most online service marketplaces net take rates in the mid-to-high teens, Fiverr commanded a marketplace take rate of 27.6% in the September-ended quarter. Consistently having the highest take rate of any freelancer marketplace is translating into a sustained generally accepted accounting principles (GAAP) gross margin that's above 80%.

Another reason I'm sold on Fiverr as an investment is its balance sheet. It closed out the third quarter with $712.5 million in combined cash, cash equivalents, and marketable securities, compared to $459.8 million in convertible debt. This $252.7 million net cash position accounted for nearly 44% of Fiverr's market cap, as of the midpoint of last week.

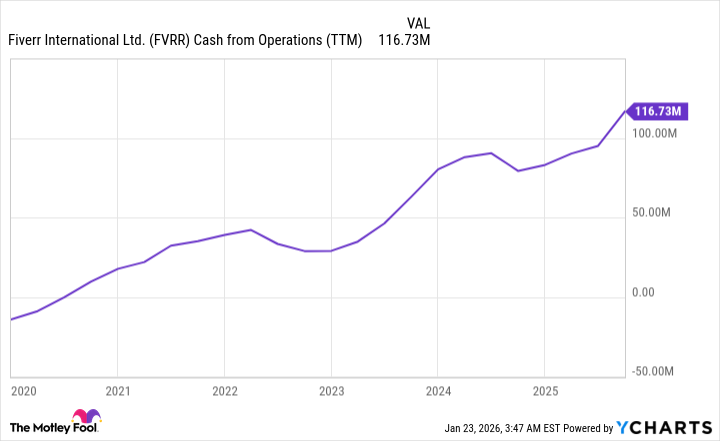

FVRR Cash from Operations (TTM) data by YCharts. TTM = trailing 12 months.

On top of its pristine balance sheet, Fiverr's cash flow has been climbing at a fairly steady pace for years. This is a company that's fully capable of generating $100 million in net cash from its operations, if not more, annually. If this were to persist, Fiverr would have more net cash on its balance sheet than its current market cap by early 2029.

Finally, there's Fiverr's historically cheap valuation. Based on adjusted earnings per share (EPS), Fiverr International stock can be scooped up for a forward P/E of just 5.5. But even using GAAP EPS, Fiverr's forward P/E of 13.5 is historically cheap. If the company's net cash is backed out, it would be akin to paying less than 8 times GAAP forward EPS for a recurringly profitable company that can generate $100 million (or more) in annual operating cash flow.

Fiverr stock may never be this cheap again.