For three years, no catalyst has fueled Wall Street's bull market rally quite like the rise of artificial intelligence (AI). Giving software and systems the necessary tools to make split-second decisions without human oversight is a technological leap forward that should benefit most global industries. Statistically, we're talking about a multitrillion-dollar opportunity that's going to result in a laundry list of long-term winners.

Although graphics processing unit (GPU) titan Nvidia is typically viewed as the face of the AI revolution, an argument can be made that there's been no greater success story than that of AI-data mining specialist, Palantir Technologies (PLTR 1.06%).

Since the beginning of 2023, shares of Palantir have rallied by over 2,500% and added close to $400 billion in market value. At its peak, Palantir had become one of the 20 most valuable publicly traded companies on U.S. stock exchanges.

Image source: Getty Images.

The issue with high-flying stocks is that when things seem too good to be true, they often are. While Palantir has clear competitive advantages that I'll touch on in a moment, historical precedent offers two undeniable clues of what's to come for Wall Street's hottest AI stock in 2026.

Palantir's competitive advantages have set the bar high

Whereas investors have focused a lot of their attention on AI data center infrastructure, Palantir has led the way with the application of AI solutions.

The leading factor that's helped Palantir stand out is the irreplaceability of its two core software-as-a-service (SaaS) platforms, Gotham and Foundry. While select competitors do exist, no company comes remotely close, at scale, to matching the services Palantir can provide with its AI- and machine learning-driven SaaS platforms.

For the moment, Gotham is the breadwinner. This SaaS platform enables the U.S. military and its allies to plan and oversee military missions. Most of the contracts Gotham secures span four to five years, which leads to highly predictable operating cash flow and sustained double-digit sales growth.

NASDAQ: PLTR

Key Data Points

But perhaps by the end of this decade, Foundry can become Palantir's biggest cash cow. This operating segment is subscription-based and used by businesses looking to make sense of their data. Foundry is a newer SaaS platform that assists businesses in streamlining their operations, which can include supply chain management and automation to improve efficiency. Palantir ended September with 742 commercial customers, up 49% from the comparable quarter one year prior.

In addition to Palantir consistently blowing past Wall Street's sales forecasts, investors are likely also enamored with its pristine balance sheet. It ended September with over $6.4 billion in combined cash, cash equivalents, and marketable securities, to go along with no debt. This abundant cash position is fueling stock buybacks and ongoing innovation, ensuring Palantir remains irreplaceable at scale.

While there's certainly a premium that professional and everyday investors are willing to pay for a sustainable moat on Wall Street, history decisively suggests the stock market's hottest AI stock has overstepped its bounds -- and by no small degree.

Image source: Getty Images.

History weighs in on Palantir's parabolic ascent

To preface any discussion based on historical precedent, the past can't concretely guarantee what will happen in the future. Nevertheless, history does tend to rhyme on Wall Street, with some correlated events exhibiting greater accuracy in foreshadowing the future than others. Two of these correlations strongly suggest Palantir stock can plunge in 2026.

The first problem for Palantir is the nature of next-big-thing investment trends. Although some of Wall Street's most-hyped technological trends have gone on to change the world, there's an undeniable learning curve when it comes to the adoption, utilization, and optimization of innovations.

For example, there wasn't any adoption issue when the internet began to proliferate in the mid-1990s. Businesses embraced this new technology as a way to expand the reach of their marketing and improve their sales and profit potential. However, it took more than half a decade for companies to figure out how to optimize the internet to boost their sales and earnings potential.

For more than three decades, investors have overestimated the adoption or optimization rate of every next-big-thing innovation, without exception. When these lofty expectations aren't met, the music stops and the bubble bursts. Although AI hardware sales are robust, we appear to be years away from businesses optimizing AI solutions to generate positive returns on their investments.

While Palantir's multiyear government contracts with Gotham and subscription-driven operating model with Foundry should act as a partial silver lining, an AI bubble-bursting event would target industry leaders, including Palantir Technologies.

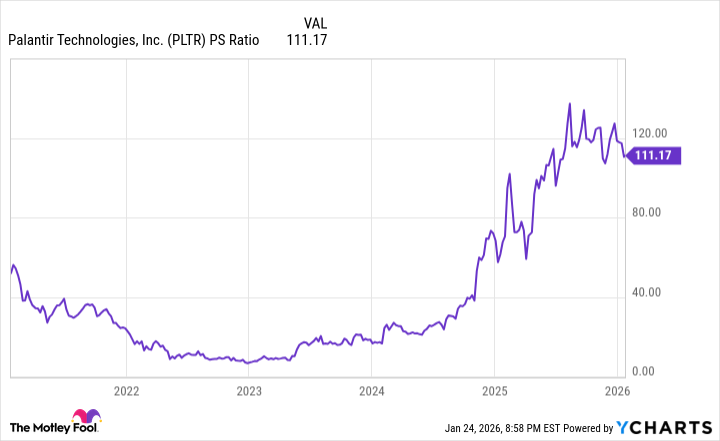

PLTR PS Ratio data by YCharts. PS Ratio = price-to-sales ratio.

The second historical issue is its otherworldly valuation. Even taking into consideration that there isn't a one-size-fits-all blueprint when evaluating a public company and that valuations are subjective, history doesn't mince words when it comes to hyped innovations trading at nosebleed premiums.

From the beginning of 1999 until the bursting of the dot-com bubble in March 2000, companies at the forefront of the internet revolution commonly peaked at price-to-sales (P/S) ratios ranging from 30 to 45, with some wiggle room at each end. While the P/S ratio wasn't helpful in identifying when these stocks topped out, it's made clear that premium valuations aren't tolerated over extended periods.

With the knowledge that no company on the leading edge of a game-changing innovation has ever been able to sustain a P/S ratio above 30, Palantir ended the Jan. 23 trading session at a P/S ratio of 111. This is nearly four times the level that historically signals a forthcoming bubble-bursting event.

Even with Palantir consistently increasing its sales forecast, there's no guide management can provide that would justify a P/S ratio of 111, let alone 30, over an extended period.

Based solely on what history has to say, Palantir stock is a prime candidate to plunge in the new year.