In January 2025, I wrote an article suggesting that investors buy artificial intelligence (AI) stocks Nvidia (NVDA 0.04%) and Meta Platforms (META +10.21%) hand over fist. My argument for each was fairly simple: Nvidia's computing hardware would continue to be in high demand, and Meta's base business would carry its stock higher while its AI developments took form. Both of those cases panned out as I predicted, but their share price moves were not as parallel as I expected.

In 2025, Nvidia's stock rose an impressive 39%, while Meta gained 13%. In a normal year, those would both be considered strong results. But last year, the S&P 500 (^GSPC 0.55%) rose by more than 16%, which made Meta a market laggard. However, I still think each is well worth buying today.

Image source: Getty Images.

Nvidia

What I wrote about Nvidia a year or so ago could nearly be copied and pasted into today's analysis, as its outlook is nearly the same. Nvidia's graphics processing units (GPUs) are still the top processors available for training and running artificial intelligence models. Additionally, Nvidia is again preparing to ship another revolutionary chip architecture. Last year's launch was the Blackwell Ultra architecture, which provided major improvements over 2024's Blackwell architecture. In 2026, the new tech is the Rubin platform, which provides further huge gains. Tech companies using Rubin hardware will be able to train AI models with a quarter of the processors they needed before, and they'll only need a tenth as many to handle the same volume of inference workloads, compared to using Blackwell.

NASDAQ: NVDA

Key Data Points

A year ago, Wall Street analysts were projecting 52% revenue growth for Nvidia in its fiscal 2026. Ironically, that's the same growth rate being projected right now for its fiscal 2027, which ends in January 2027. Now trading at 40 times forward earnings, the stock is cheaper than it was in January 2025, when it traded at 47 times forward earnings.

In sum, nothing has changed for Nvidia's stock except that it's a bit cheaper. This makes it a no-brainer buy right now, and I think it will crush the markets again in 2026.

Meta Platforms

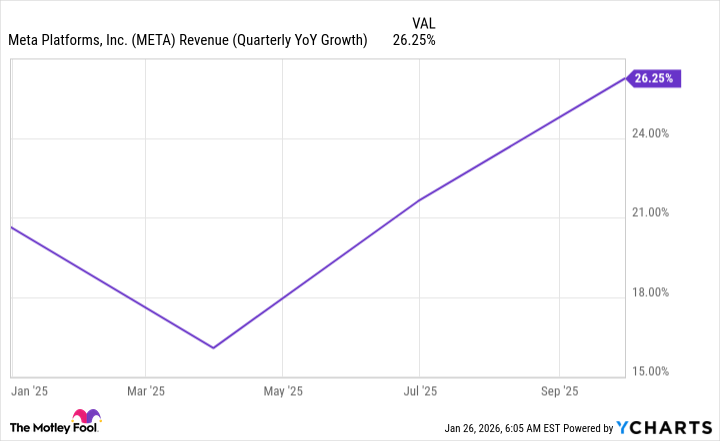

Meta Platforms' base business did incredibly well in 2025. In Q3, its revenue rose by 26% year over year, continuing the acceleration it started in Q2.

META Revenue (Quarterly YoY Growth) data by YCharts.

However, the bigger issue that has been dragging on the stock price is the company's capital expenditure plans. Wall Street is concerned about how much Meta will spend on data centers in 2026, and as a result, the stock is down around 15% from the all-time high it touched in August.

Its social media businesses are still doing well, so its valuation of 22 times expected forward earnings is fairly reasonable. The market is primarily concerned about whether Meta will get a return on investment for all of its AI spending. If it can deliver solid growth, then the stock has room to soar. If it cannot, it may remain stuck in a lower valuation range.

I think Meta's stock is a great buy at its current price, and investors should consider scooping it up to benefit from a potential rebound from the slump it has been in since last summer.