The S&P 500 (^GSPC 0.43%) is up 14.9% over the last year, but payment processors Mastercard (MA 0.91%) and Visa (V 3.00%) are down slightly. Both stocks have sold off so far in 2026 as investors grow concerned about weakening consumer spending and the Trump administration's proposed 10% cap on credit card interest rates.

Visa and Mastercard reported quarterly earnings on Jan. 29. Here are the key takeaways and why both stocks are great buys on the dip.

Image source: Getty Images.

Strong results from Mastercard and Visa

In their earnings releases, Mastercard and Visa both credited solid consumer spending for their record results -- challenging the narrative that consumer spending is under pressure.

Mastercard's revenue jumped 18%, and Visa's rose 15%. Mastercard's operating income grew by 25%, far faster than the 10% increase in operating expenses as operating margins grew to 55.8% and diluted earnings per share (EPS) jumped 24%. Visa's operating margin was even better at 61.8%, but its non-GAAP (adjusted) EPS increased by 15% -- less than Mastercard.

Both companies reported high-single-digit to low-double-digit increases in payment volume and frequency. Mastercard and Visa make money every time their cards are swiped, tapped, or processed digitally. The fee structure is based on frequency and a percentage of total sales. So both companies are somewhat recession-resistant, in the sense that they will still do well as long as consumers use their cards rather than alternatives like other cards or cash. But they will do even better when global spending is growing -- which it did in 2025 despite a flurry of consumer spending challenges.

NYSE: MA

Key Data Points

Returning capital to shareholders

2025 was a banner year for Mastercard and Visa, as both companies performed well in a less-than-ideal operating environment. Since both companies have such high operating margins, they can afford to maintain rock-solid balance sheets with tons of cash and very little debt, and consistently raise their dividends and buy back stock.

In 2025, Mastercard paid $11.73 billion in stock buybacks and $2.76 billion on dividends. In its latest quarter, which was the first quarter of fiscal 2026, Visa bought back $3.73 billion in stock and paid $1.29 billion in dividends -- a run rate of $20.08 billion for the year.

Both stocks yield less than 1% because they prefer to return cash to shareholders through buybacks over dividends. But if both companies hypothetically reallocated all their funds toward dividends instead of buybacks, Mastercard would yield about 3% and Visa would yield 3.1%. Mastercard and Visa fully support their buybacks and dividends with free cash flow -- a sign that returning capital to shareholders is sustainable and affordable.

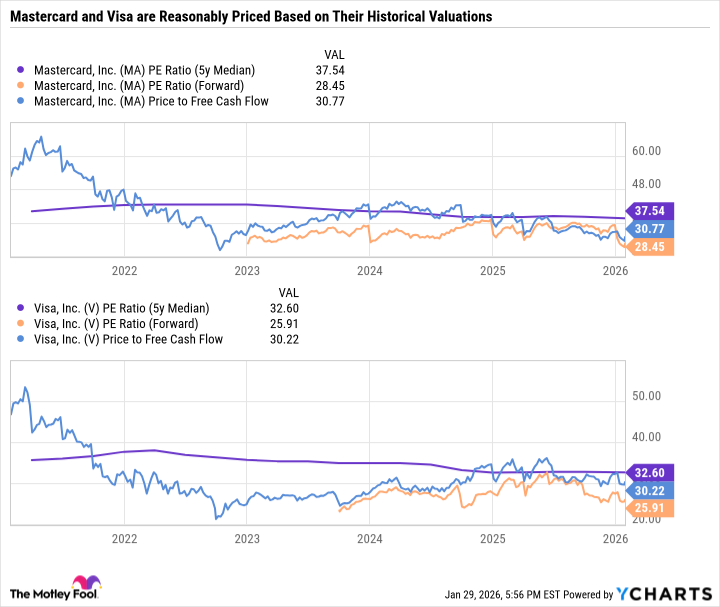

To top it all off, both stocks sport reasonable, if not borderline cheap, valuations based on price-to-FCF and forward earnings expectations.

MA PE Ratio (5y Median) data by YCharts

Two foundational stocks to build a portfolio around

Mastercard and Visa are two of the best business models in the world. By working with financial institutions to issue cards, they avoid the credit risks that come with managing loans and debt. Instead, their value comes from their global network effects and processing.

Both companies have done an exceptional job of growing their employment networks. And while the issue of capping credit card interest rates could persist, I doubt something as low as 10% would be implemented. At such a low incentive, financial institutions would simply restrict credit access for many users, which would hurt consumers in the long run.

Add it all up, and Mastercard and Visa are two high conviction stocks to buy in 2026 that can anchor a long-term portfolio.