We're just one month into 2026, and it's already looking like artificial intelligence (AI) stocks are set for another year of strong gains. As the hyperscalers continue to expand their data center capacity, investors understand that semiconductor stocks in particular stand to benefit.

The smartest investors are realizing that AI budgets are not just about buying GPUs and networking equipment anymore, though. With that in mind, Micron Technology (MU 3.33%) looks like a top AI chip stock to buy for 2026.

Image source: Micron Technology.

AI's new bottleneck is memory and storage

According to a forecast from Goldman Sachs, big tech will spend over $500 billion on AI capex in 2026. If you only paid attention to the headlines, you'd think every penny of that was destined for the coffers of Nvidia, Advanced Micro Devices, and Broadcom. At this point, it seems like these three chip designers are announcing new deals or strategic partnerships practically every day.

Here's what most investors are overlooking: As more GPU clusters are built, AI developers are pushing their training and inference capabilities to the max. Those expanding AI workloads are facing bottlenecks when it comes to memory and storage.

Micron specializes in high-bandwidth memory (HBM) chips. Just to clarify how vital this niche of the chip realm is, consider that the company is forecasting that the total addressable market for HBM solutions will grow at a 40% compound annual rate over the next couple of years and reach $100 billion by 2028.

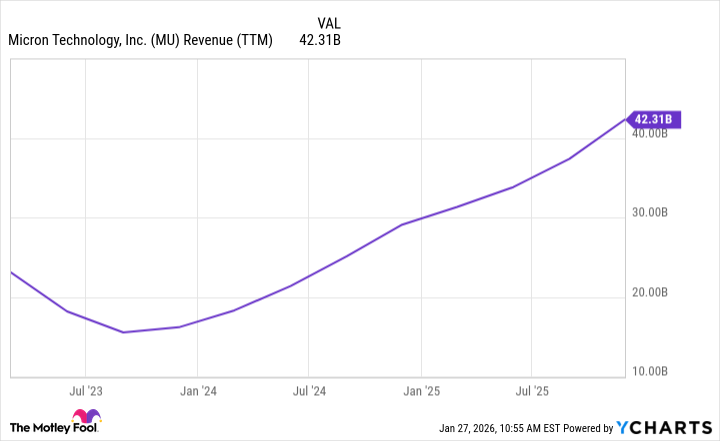

MU Revenue (TTM) data by YCharts.

Considering Micron's trailing-12-month revenue isn't even half the value of the expected HBM market size, I think the company could be on the cusp of an epic growth arc.

Against this backdrop, and with demand for memory already well outpacing supply, Micron has plenty of leverage to raise prices for its memory and storage chips. As such, the company should be able to complement its revenue acceleration with healthy profit margins.

Is it too late to buy Micron stock?

Over the last year, Micron stock has skyrocketed by nearly 300%. In the wake of that type of gain, you might think it's too late to buy the stock.

While a rise of that magnitude in such a short time frame would generally leave a stock overbought, Micron is a rare exception to that principle.

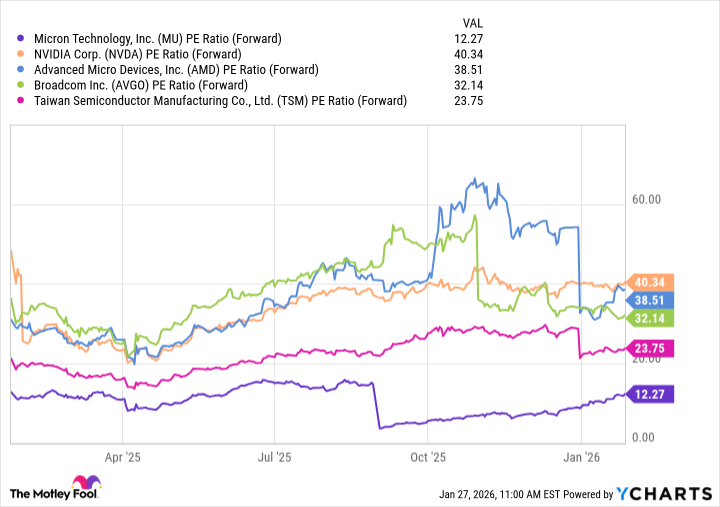

MU PE Ratio (Forward) data by YCharts.

Micron's forward price-to-earnings (P/E) ratio is considerably lower than those of other leading semiconductor businesses. Even after the stock's meteoric rise, Micron's valuation pales when benchmarked against other mission-critical chip players.

In 2026, the Wall Street analysts covering Micron expect its earnings per share to triple to about $33. Should the stock continue to appreciate and reach a forward P/E level of, say, 25 -- somewhat more in line with other indispensable chipmakers -- shares of Micron would double by year's end.

But don't focus too much on specific implied price targets. The bigger takeaway from this analysis is that Micron is poised for explosive growth both in 2026 and beyond, with both earnings growth and a valuation expansion apparently on the horizon. As such, buying its shares now with the intention to hold them for the long run should result in meaningful gains.