Over the past few years, there have been few better stocks to own than Nvidia (NVDA +4.34%). In 2023, its stock rose 239%. It then followed up its excellent 2023 with a strong 2024, rising 171%. 2025 was a comparatively tame year, with the stock rising 39%. However, investors are wondering if Nvidia could double this year.

It's not going to be easy to do, but if Nvidia can attain the same valuation as some of its peers, then I think it's entirely possible that Nvidia could double. However, investors need to watch out for rising competitors.

Image source: Getty Images.

Nvidia's hardware is best in class

Nvidia's graphics processing units (GPUs) are the top computing option in the artificial intelligence (AI) realm. Its full technology stack is second to none and gives users a turnkey product to do all the AI training and processing they want. Although Nvidia's products are at the top of the industry, it's constantly innovating and launching new products

Its next architecture generation, known as Rubin, cuts the number of GPUs needed to train an AI model by a fourth compared to the previous Blackwell generation. It can also be deployed for inference scenarios and at a 10x lower cost per token than Blackwell.

NASDAQ: NVDA

Key Data Points

Those are huge improvements that will keep Nvidia at the top of the list of best computing products. But all of this comes at a cost.

It's no secret that you have to pay a premium to use Nvidia hardware. As a result, companies have been exploring cheaper alternatives. While they will never replace Nvidia completely, supplementing their computing infrastructure with products from competitors ensures that Nvidia's prices don't get too out of hand.

Advanced Micro Devices' computing hardware is often cheaper, and its capabilities are improving thanks to its ROCm control software finally receiving upgrades to compete with Nvidia's CUDA. Broadcom's custom AI accelerators are also a worthy challenger, as they are custom-designed for each end user to handle the workloads they have in mind. This creates a computing option that can outperform Nvidia's GPUs in specific tasks, at a lower price point.

Both companies pose a threat to Nvidia, but Nvidia is still selling its hardware to AI developers and users worldwide. But can that lead to its stock doubling?

Nvidia's road to a double will not be easy

At Nvidia's $4.5 trillion market cap, it would need to be a $9 trillion company to double. That's monstrous and would make Nvidia about the same value as Apple, Microsoft, and Amazon combined. But if the financials warrant that valuation, then it could be entirely reasonable.

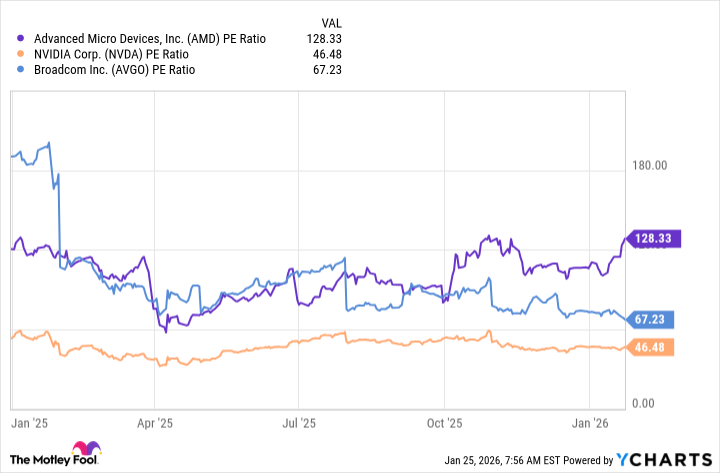

Wall Street analysts project a 52% growth rate for fiscal year (FY) 2027, which would bring its earnings per share (EPS) to $7.66. Currently, Nvidia trades at a price-to-earnings (P/E) ratio of 46. That's a bit cheaper than some of its peers.

AMD PE Ratio data by YCharts.

If Nvidia achieves $7.66 in EPS in FY 2027 and trades at a 46 times trailing-earnings valuation, that would price the stock at $352.36 per share. That would translate to a market cap of $8.7 trillion, falling just short of the $9 trillion threshold noted above.

If Nvidia's trailing P/E ratio rises to 50, it would be valued at $9.4 trillion. So, Nvidia doubling is actually not far out of the realm of possibilities; it will just require its trailing valuation to stay high. Even if it doesn't double, Nvidia is still slated for a strong 2026, and I think investors should load up on the stock before the rest of the market catches on.