Only a few dozen companies have ever broken the $350 billion market cap mark. Now, imagine losing that much value in hours. That's what happened to Microsoft (MSFT 2.86%) on Jan. 29, 2026 after reporting its fiscal second-quarter (ended Dec. 31, 2025) earnings the day before.

It's fair to wonder whether this sell-off is a warning sign, a sign of the stock correcting itself, or the result of irrational investors. While that remains to be seen, one thing is sure in my eyes: Microsoft is still one of the better artificial intelligence (AI) stocks you can invest in for the long haul.

Image source: Microsoft.

Why are investors jumping ship?

Microsoft's quarterly results were impressive, all things considered. Its revenue grew 17% year over year to $81.3 billion (nearly $1 billion more than estimates), earnings per share (EPS) increased 24% to $4.41 ($0.22 more than estimates), and net income increased 23% to $30.9 billion.

Despite Microsoft's impressive performance, there are two main reasons why investors began jumping ship and selling: its capital expenditures (capex), and projected slowdown in Azure (its cloud platform) growth.

In the last quarter, Microsoft spent $37.5 billion on capex. For perspective, that's more than Walmart's profit from its past four quarters combined. And while spending a lot isn't bad in itself, investors have seemingly grown impatient with the lack of returns on this heavy spending.

Azure also posted an impressive quarter, up 39% year over year, but the focus was on its likely slower growth in the near future.

NASDAQ: MSFT

Key Data Points

Keep your eyes on the long-term prize

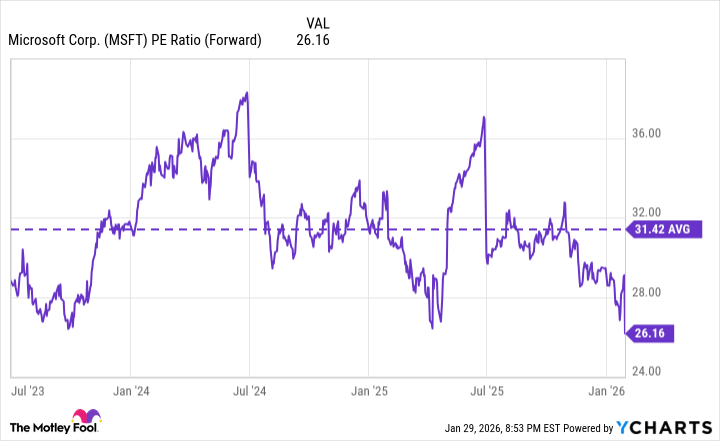

I still believe Microsoft is a great buy. If anything, this recent drop presents a more attractive opportunity to begin or increase your stake. It's currently trading at around 26.2 times its projected earnings over the next 12 months, well below its average for the past couple of years.

MSFT PE Ratio (Forward) data by YCharts

Regarding Microsoft's spending, yes, it's a lot, but I think investors are falling victim to impatience (nothing new there). Microsoft is spending on longer-term projects that won't necessarily produce immediate profit boosts. And although this spending might have a short-term impact on margins or free cash flow, investing in Microsoft is about the long game.

I'm also not concerned about Azure's potential growth slowdown. Microsoft predicts Azure revenue will grow between 37% and 38% this quarter, only a slight slowdown from the previous quarter. But even if its growth slows by more, the platform is well positioned to keep a lock on the No. 2 spot behind Amazon's AWS.