Revenue growth isn't always a reason to invest in a company. While it can be impressive, it's important for investors to focus on other numbers beyond just the top line. A fast-growing business can have problems under the hood that make it a bad buy overall.

Super Micro Computer (SMCI 2.45%), commonly referred to as just Supermicro, has been experiencing tremendous growth in recent years as demand for its servers has been red hot due to continually strong demand for all things related to artificial intelligence (AI). The company recently reported its latest earnings numbers, which again showed impressive year-over-year sales growth. But despite the strong top-line numbers, here's why you shouldn't rush out to buy the tech stock.

Image source: Getty Images.

Supermicro's margins remain incredibly low

One important number investors should always consider when investing in growth stocks is gross profit. This represents revenue less cost of goods sold, which tells you how much is left over to cover the company's remaining operating expenses and overhead. Low margins will make it incredibly difficult for a business to grow its earnings unless it is doing an incredibly large amount of volume.

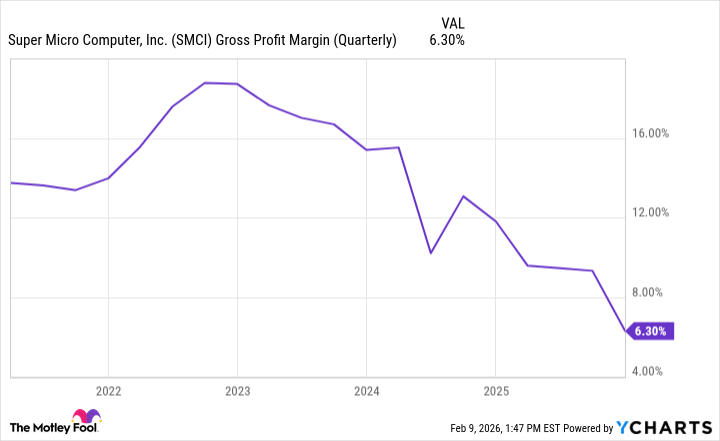

Supermicro's margins are not only low and in the single digits, but they've also been declining.

SMCI Gross Profit Margin (Quarterly) data by YCharts

The company recently reported its earnings for the last three months of 2025, and while net sales rose by 123% to $12.7 billion, its gross profit increased by just 19%, to $798.6 million. Overall operating income of $474.3 million was up by 29%. While that's some solid growth, it's nowhere near as strong as what the top line showed.

NASDAQ: SMCI

Key Data Points

The stock looks cheap, but it's not worth the risk

Currently, Supermicro stock trades at just 25 times its trailing earnings, which may look cheap given that it's benefiting from a lot of AI-related growth. But consider that this is the type of growth it is achieving under ideal conditions, when there is a big arms race in AI and tech giants investing heavily into AI models. As that inevitably slows down, Supermicro's business may begin to look much worse. Right now, its incredibly fast revenue growth is enabling the bottom line to rise at a good pace, but that's not likely to happen amid a slowdown in tech spending.

At 25 times earnings, the stock is arguably a bit of a risky option given its poor margins and the question marks around its future growth.