When OpenAI released ChatGPT to the public on Nov. 30, 2022, shares of Nvidia (NVDA 1.86%) were priced at $1.69 per share, adjusting for stock splits. As of Wednesday's market close, shares were priced at $191.10, a stunning 11,208% rise that would have turned every $1,000 invested back then into $113,900.

Even over three-plus years, it's the kind of gain investors dream of getting even once. But amazingly, Nvidia may still have significant upside remaining. In fact, there's reason to think that shares are even cheaper than they were at ChatGPT's debut. Here's why.

Image source: Getty Images.

Nvidia's price-to-earnings (P/E) ratio is significantly lower now

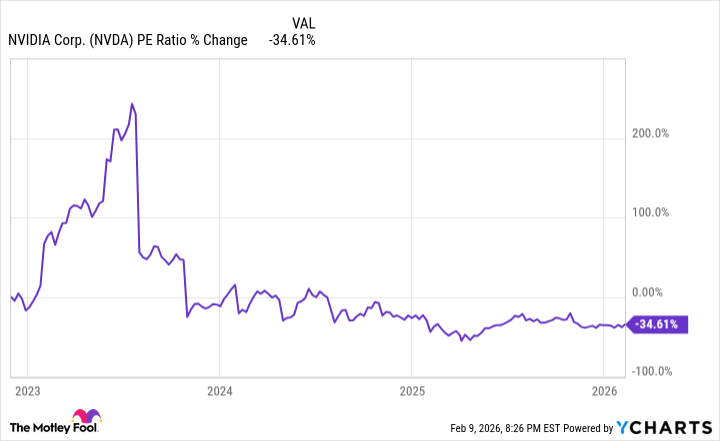

While Nvidia's share price is up 11,208%, its earnings have, incredibly, grown even faster. You can see this in the below chart, which shows the percent change in the price-to-earnings (P/E) ratio since Nov. 30, 2022.

Data by YCharts.

As you can see, shares are more than 34% cheaper by this metric. If this is still hard to believe, consider Nvidia's last quarterly earnings report before ChatGPT came out. On Nov. 16, 2022, the company reported $680 million in net income for the prior quarter.

In its most recent quarter, Nvidia reported net income of $39.1 billion. That 4,591% rise in net income since the launch of ChatGPT falls short of the 11,208% rise in share price. What more than makes up the difference is the company's massive share buyback program.

Last year, Nvidia announced a $60 billion buyback program, a record for the company, and that came on top of its $50 billion buyback program announced in 2024. Share buybacks boost earnings per share by reducing share count, an effect that isn't seen by looking at just the dollar amount of earnings growth.

NASDAQ: NVDA

Key Data Points

So, is Nvidia a buy today?

Companies that are "cheap" aren't necessarily buys, since low P/E ratios can indicate value traps. Today, Nvidia trades at 46 times earnings. That's a premium, to be sure, but not near the nosebleed valuations that the most dangerous tech stocks reached on the eve of the infamous dot-com collapse.

Last quarter, Nvidia grew earnings by 65.3% year over year. That's growth that, if sustained for even a few more quarters, would allow the company to grow into its P/E ratio and then some. Meanwhile, its earnings growth has surprised analysts on the upside in each of the last four quarters. My hunch is that this company is not done surprising, and has much more upside left than Wall Street expects.