Last year, shares of artificial intelligence (AI) chip stock Micron Technology (MU -0.56%) blasted higher by 239% -- making it one of the top-performing stocks in the Nasdaq-100 index.

While this level of momentum might suggest you've missed your opportunity to cash in on the AI darling, what if I told you the stock remains dirt cheap even after its parabolic rise? Let's dig into the tailwinds fueling Micron stock right now and explore why the company's growth is just getting started.

Image source: Micron Technology.

The AI memory supercycle: How GPUs are driving demand for high-bandwidth memory

When it comes to headlines about AI chips, odds are investors see references to Nvidia and Advanced Micro Devices more than any other company.

Nvidia's roots are in designing graphics processing units (GPUs) -- the hardware hyperscalers use to build generative AI applications. The company's deep roster of Hopper, Blackwell, and now Vera Rubin architectures have helped Nvidia achieve a 92% market share in the AI GPU space.

In a distant second is AMD, whose MI400 accelerators have started to attract enterprise workloads as big tech seeks to complement their Nvidia infrastructure with a lower-cost chip stack.

As hyperscalers like Microsoft, Amazon, Alphabet, and Meta Platforms accelerate their AI capital expenditures, GPU designers such as Nvidia and AMD become the obvious winners. But underneath the surface, Micron is perhaps even more strategically positioned for the AI infrastructure revolution.

My rationale is that as more data centers are built and outfitted with GPU clusters, AI workloads will scale as developers introduce new products and services. In turn, these dynamics create a bottleneck in memory and storage solutions -- precisely the market in which Micron operates.

NASDAQ: MU

Key Data Points

Wall Street estimates: The path to 400% earnings growth

Given the secular tailwinds fueling demand for HBM solutions, industry research suggests that the prices for dynamic random access memory (DRAM) and NAND chips could rise as much as 60% and 38%, respectively, during the first quarter.

These dynamics give Micron enormous levels of pricing power as hyperscalers increase their AI infrastructure budgets to be more inclusive of HBM systems. Against this backdrop, it's no surprise the company has already reportedly sold out of its 2026 HBM inventory -- hence, Wall Street's bullish forecast.

For Micron's fiscal year 2025 (which ends Aug. 28), the company reported $7.59 in earnings per share (EPS). According to Wall Street's consensus estimates, Micron's earnings are expected to be $33.73 per share in fiscal 2026 -- representing over 340% growth year over year.

Valuation: Micron's forward P/E suggests significant upside is ahead

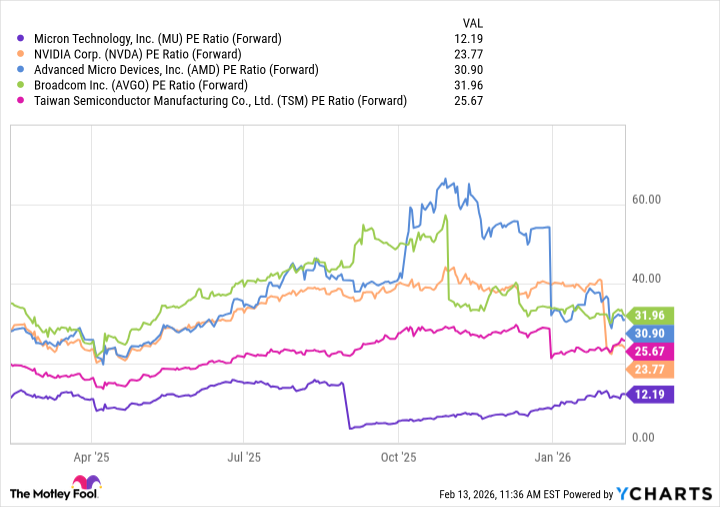

Despite Micron's potential, the stock still trades at a discount relative to other AI chip leaders based on forward price-to-earnings (P/E) trends. In my eyes, the disparity between Micron and its cohorts is due to the cyclical nature of the memory chip market.

MU PE Ratio (Forward) data by YCharts

Smart investors understand that there aren't many companies in Micron's position -- being on the cusp of riding a multi-year growth arc underscored by rising AI infrastructure buildouts. I think Micron's valuation profile will normalize relative to its growth potential throughout 2026.

Should Micron trade more in line with other category leaders in the AI semiconductor market, the stock could reasonably soar anywhere between $650 to $800 -- suggesting up to 100% upside from current levels.

For these reasons, I think Micron stock remains incredibly undervalued and is a no-brainer buy at its current price point.