Apple (AAPL +0.91%) is the world's second-largest company, with a market cap of $3.8 trillion (as of Feb.12). However, I think it'll be surpassed by others over the next few years.

The reality is that Apple's artificial intelligence (AI) strategy has fallen on its face, and it is now relying on Google to save the day. Additionally, it has failed to launch any innovative new products over the past few years, which indicates it is resting on previous success, not future innovation.

This can open the door for a few companies to pass Apple in terms of valuation in a few years, and I think Apple's days as one of the world's largest companies are numbered if it doesn't start innovating again.

NASDAQ: AAPL

Key Data Points

Apple trades at a premium valuation

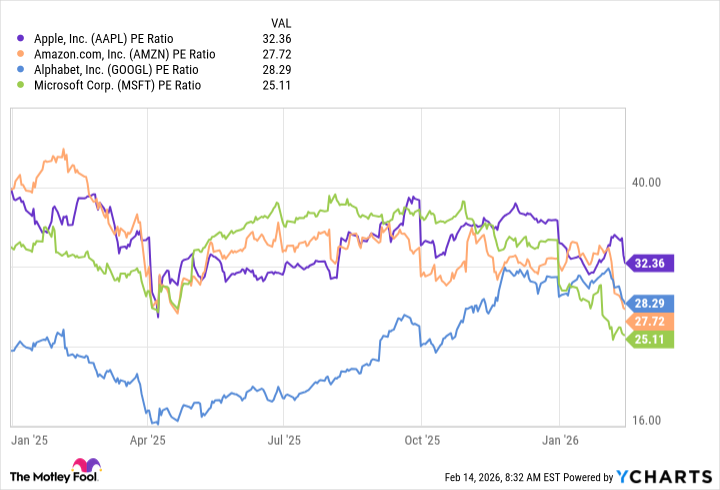

One of the reasons why Apple has such a high market cap is its valuation. Compared to Alphabet (GOOG 0.37%) (GOOGL 0.36%), Microsoft (MSFT 0.16%), and Amazon (AMZN +1.38%), Apple has a large premium, as measured by price-to-earnings ratio.

AAPL PE Ratio data by YCharts

At a price-to-earnings ratio of 32, Apple is far more expensive than the other three stocks that I think will be worth more than it three years from now. I'm not against a stock having a premium valuation, but it must be earned. I don't think Apple's is.

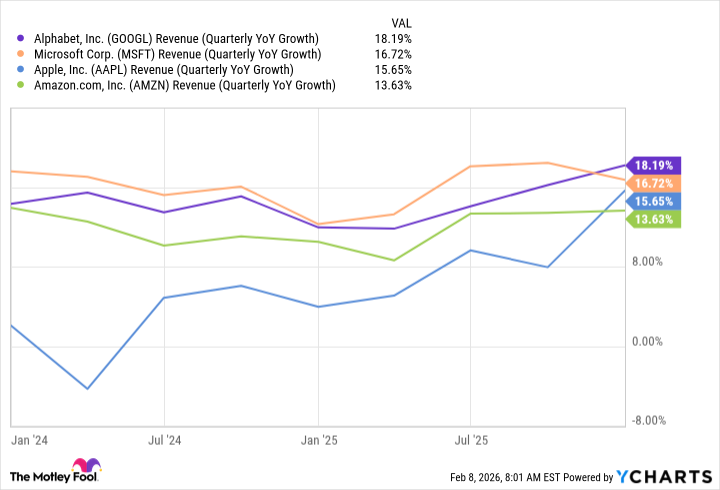

Just take a look at the growth rates of these companies over the past few years.

GOOGL Revenue (Quarterly YoY Growth) data by YCharts

Although Apple had a strong holiday quarter, I need to see more results before I'm willing to give it a premium. The reality is Apple has delivered single-digit revenue growth or worse for the past few years. The other three have been growing much faster, and I'd expect that trend to revert in the ensuing quarters for Apple.

If it can deliver mid-double-digit growth as it did in its recent quarter, I think a slight premium (although not the massive one it has now) is warranted. But until then, I like the chances of the other three stocks rising at a much faster pace.

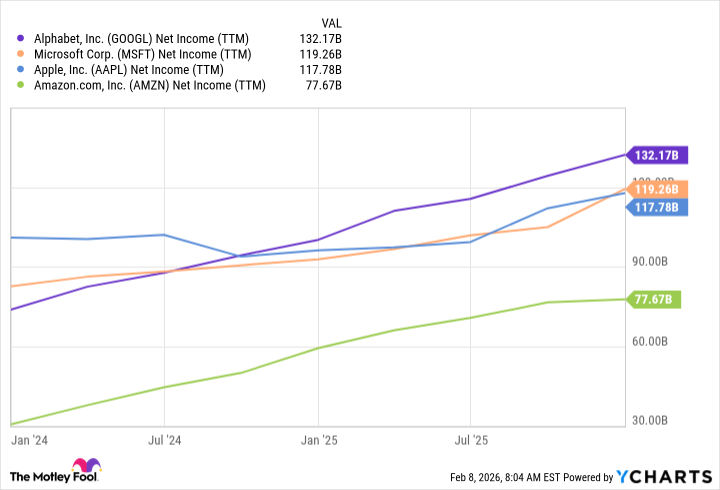

If you look at raw net income figures, you can see which components should be worth more if they each had the same earnings multiple attached to them.

GOOGL Net Income (TTM) data by YCharts

Using that logic, Alphabet and Microsoft should be worth more than Apple, although Amazon still has a ways to go. I think Amazon can close the gap over the next few years, and the primary way it will do that is through its cloud computing platform. Alphabet and Microsoft also have a thriving cloud computing business, and it provides a massive upside that Apple doesn't have.

Cloud computing will power these three to new levels

In Q4, Google Cloud from Alphabet posted the best quarter, with revenue rising 48% year over year. Microsoft's Azure and other cloud services posted the second-best quarter at 39% year over year. Amazon Web Services (AWS) was the slowest-growing at 24% year over year, but it was also its best quarter in over three years. AWS has developed some chips to rival those from the biggest players, and that business is growing at a triple-digit pace.

Cloud computing is a huge part of the AI buildout because it gives developers access to computing power that doesn't make sense to build out individually. Cloud computing is on a multi-year trajectory to boom thanks to the generative AI buildout. It will boost Alphabet and Microsoft to new heights and will also cause Amazon's profits to soar over the next few years. I think it could be to the point where it surpasses Apple. However, if Apple can launch an innovative new product or feature that boosts its revenue, Apple may prevail.

Time will tell how Apple fares, but one quarter won't define a company's comeback. If Apple can deliver similar growth over the next few years, then its premium valuation is warranted. Until then, I'm still skeptical and prefer these other three stocks.