The artificial intelligence (AI) trade has been completely upended in 2026.

Last year, investors focused on the immense potential of AI and how it could transform businesses and the global economy. This year, markets are trying to assess who the winners and losers will be in the AI boom. And the latter group is getting hit hard.

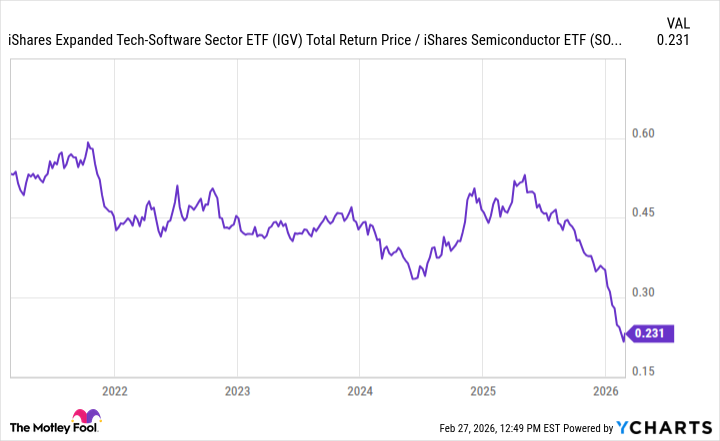

This is a popular chart that's been making the rounds. It compares the relative performance of software stocks to semiconductor stocks.

Fundamental Chart data by YCharts

The implication is pretty clear. Investors believe that the demand for chips (and the subsequent revenue and earnings growth that comes from it) is likely to continue. The software sector, on the other hand, is thought to be replaceable by AI as coding capabilities continue to improve.

For the time being, it looks as if semiconductors are the way investors will play AI growth.

Image source: Getty Images.

My top pick for this space was the VanEck Semiconductor ETF (SMH 2.93%). Its concentrated exposure in this sector (it owns around 25 names and market cap-weights them) helped produce a 49% return in 2025. It's up another 12% in 2026 year to date.

Clearly, investors love their semiconductor stocks, but can it sustain its momentum?

The growth outlook remains strong

There's no question that the AI boom will fuel chip demand for the foreseeable future. The global semiconductor sector is expected to hit $975 billion in sales in 2026, a 26% growth rate compared to the previous year.

NASDAQ: SMH

Key Data Points

That growth rate will start to slow eventually. Over the next year, however, 26% growth looks like a reachable target. Given big tech company spending on AI buildouts and the number of years it's likely to take to get close to anything resembling a finished product, strong growth is likely to keep fueling stock price gains.

Nvidia's post-earnings stock price drop provides a warning

The biggest question is whether investors are already paying too much for this growth story.

The VanEck Semiconductor ETF currently trades at 45 times trailing 12-month earnings. If we assume that 26% growth rate, the forward price/earnings (P/E) ratio gets closer to 35.

Anytime the P/E ratio gets significantly above the growth rate, the value question comes into play. We just saw Nvidia (NVDA 1.49%) report quarterly revenue expectations, earnings expectations, and included raised guidance for the coming year. The stock still lost more than 5% on the day following the announcement.

That suggests the market may have fully priced growth expectations into stock prices. And any miss in the near future could be met with a harsh reaction in the stock price.

Overall, I still like the outlook for the VanEck Semiconductor ETF. One risk, however, is how top-heavy it is. Roughly 30% of the portfolio is dedicated to the combination of Nvidia and Taiwan Semiconductor. That will make future performance heavily dependent on just two companies.

But the market is still sticking with the industry's mega-cap leaders for the time being. As long as that's the case, this ETF could be lined up for another strong year in 2026.