SoundHound AI (SOUN 4.11%) is a voice artificial intelligence (AI) company that looks to help its customers add efficiency to their day-to-day operations. It has been growing its customer base via acquisitions, and that has enabled the business to become more diversified in the process.

Investors may be surprised to learn, however, that despite doubling its sales in 2025, the AI stock has been struggling badly. At around $3.4 billion, its market cap is a fraction of what it was in the past, and the stock is down 64% from its 52-week high of $22.17. Here's why there is no shortage of bearish investors when it comes to SoundHound AI stock.

Image source: Getty Images.

SoundHound's growth rate has been slowing down

Last month, SoundHound reported its fourth-quarter results for 2025, which showed strong top-line growth of 59%, as revenue came in at just over $55 million for the last three months of the year. And the company's full-year revenue of $168.9 million roughly doubled the $84.7 million that SoundHound reported a year ago.

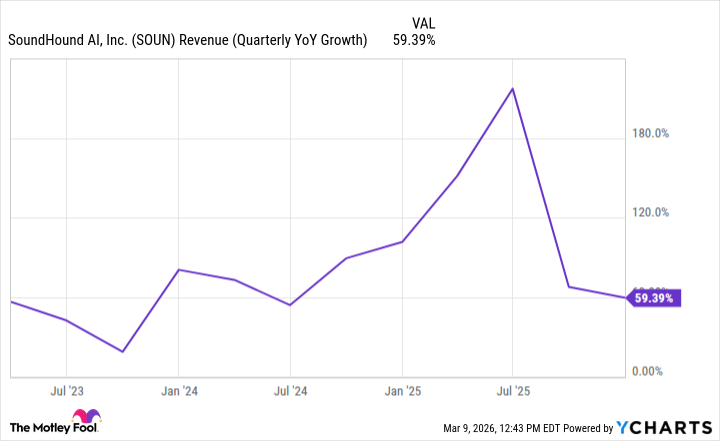

Normally, a fast-growing business will see its most recent quarterly results growing at a faster rate than the full-year rate. But in SoundHound's case, its growth rate has actually been slowing down in recent quarters.

SOUN Revenue (Quarterly YoY Growth) data by YCharts

The chart paints a very different story, one of a brief spike followed by a sharp slowdown. While a near-60% growth rate is impressive, it's important to understand why SoundHound has done well. The growth has been primarily due to acquisitions, which can make it difficult to determine just how well the tech business is doing organically. While acquisitions can provide a company's top line with a boost, that type of growth can be short-lived if the entire entity isn't growing organically.

NASDAQ: SOUN

Key Data Points

Why SoundHound doesn't make for a great growth stock

As impressive as its growth rate may seem, there are still sizable problems with SoundHound's business. Last year, the company incurred an operating loss of $23.3 million, which would have been significantly worse if not for a favorable $163.1 million change in the fair value of contingent acquisition liabilities. SoundHound also used up $98.2 million just from its day-to-day operating activities.

The company's lack of profitability, ongoing cash burn, and pursuit of acquisitions make this a risky stock to own, as investors may experience a lot of dilution in the future. Year to date, the stock is down 20%, and it wouldn't be surprising to see SoundHound go even lower because while its growth rate may seem impressive, it doesn't tell the whole story.