In contrast to the mainstream artificial intelligence (AI) sector, which is dominated by a host of well-known large and megacap players, in the quantum computing space, the most popular stocks so far include a small collection of relatively unknown companies. One that has emerged as a perceived leader in the quantum computing space is IonQ (IONQ 2.34%).

With shares up more than 30% over the last year, IonQ stock has outperformed both the S&P 500 and Nasdaq Composite. Yet Wall Street thinks IonQ's rally is just getting started. The average price target among analysts covering IonQ is $65 -- more than 100% higher than current trading levels.

While it's tempting to follow the hype, I think Wall Street is wrong on this one.

Image source: Getty Images.

IonQ's explosive revenue growth is less meaningful than it seems

Last year, IonQ reported jaw-dropping 202% revenue growth to $130 million. Similarly impressive is the company's guidance for 2026: Management forecasts revenue to be in the range of $225 to $245 million, representing 81% growth at the midpoint.

With integrations with each of the big three cloud service providers -- Microsoft Azure, Amazon Web Services, and Google Cloud Platform -- in addition to a strategic partnership with Nvidia, you probably think that IonQ's approach to building a vertically integrated quantum computing ecosystem is poised for explosive AI-driven growth over the next several years.

Here is why I'm not impressed by IonQ's growth arc: The company has spent more than $4 billion on acquisitions over the last couple of years. So not only is a major portion of IonQ's revenue -- and its revenue growth -- coming from inorganic (acquired) assets, the company has yet to generate much from these sources relative to what it paid.

NYSE: IONQ

Key Data Points

IonQ has a money problem that the market isn't paying attention to ... yet

While IonQ has crossed the $100 million sales milestone, the company is burning cash like there's no tomorrow. In 2025, IonQ posted net losses of over $500 million, and its operating cash flow was negative $283 million. The company is nowhere close to becoming profitable.

Moreover, with this type of cash burn rate, IonQ's liquidity of $2.4 billion doesn't give it much of a runway. This raises the question: How is IonQ even funding its growth?

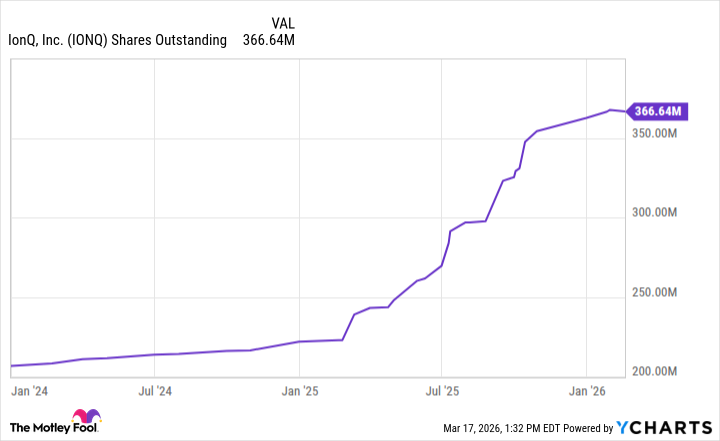

IONQ Shares Outstanding data by YCharts.

Since 2024, IonQ's outstanding share count has almost doubled. Notice that significant issuances occurred throughout the last year -- while the stock price was soaring.

The premise here is that IonQ has taken advantage of its rising valuation by issuing stock to raise money and pad its balance sheet. Management then used that capital to fund acquisitions that it marketed as game-changing growth catalysts -- further fueling the hype cycle.

Why IonQ could lose 80% of its value by year's end

Issuing stock to fund growth and diluting shareholders in the process is not a sustainable strategy. I think it's only a matter of time before investors catch on to IonQ's playbook and rotate their capital toward more durable opportunities in the tech landscape.

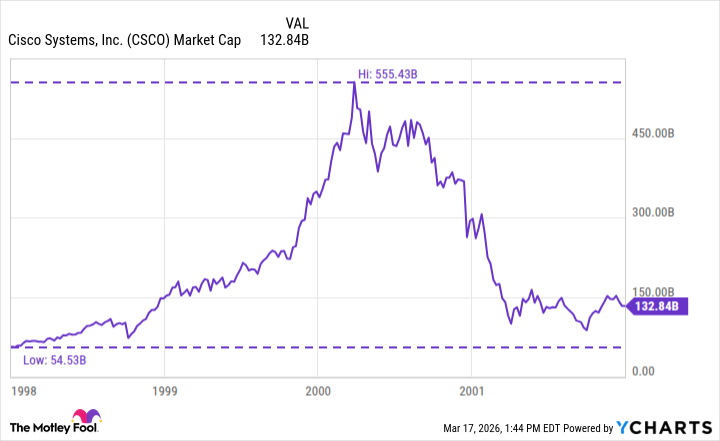

In my view, IonQ trades more like a meme stock than a sound investment. While the company continues to promote a narrative that echoes those that were once common among dot-com bubble darlings, I predict that IonQ stock will crater in a similar fashion to Cisco in the early 2000s.

CSCO Market Cap data by YCharts

By year's end, I think it's more likely that IonQ will be trading below $10 than it is to double and hit Wall Street's target.