Veeva Systems (VEEV +3.59%) has hit significant challenges over the past six months, as many investors increasingly fear that competition will erode its market share. The company's stock is down by 37% over this period, as of this writing. However, after its massive correction, Veeva Systems' shares look attractive. Here is why long-term investors should seriously consider investing in the company at current levels.

Image source: Getty Images.

The price is right

Veeva Systems specializes in designing cloud solutions for life sciences companies, a niche where it is a leader. It may be a fairly small player in the broader cloud computing market, but thanks to its cloud software that addresses the unique challenges and requirements of biotech and pharmaceutical companies, it is deeply embedded in the day-to-day activities of some of the top players in this niche. This grants Veeva Systems an economic moat thanks to switching costs, as it isn't easy for its clients to jump ship, at least not without risking business disruptions.

Can Veeva Systems bounce back and perform well over the next five years (and beyond) despite increased competition? My view is that it can, and here are four reasons the stock is a buy right now. First, the company continues to add new customers to its ecosystem, as it did during its latest period. Veeva Systems boasts 15 of the top 20 biopharmas as its clients.

NYSE: VEEV

Key Data Points

Second, Veeva Systems is investing in ways that could pay off down the road, notably in artificial intelligence (AI). The company won't be content with generic AI solutions; just as its cloud services are tailored to the demands of the life sciences industry, so will its AI tools. Veeva Systems launched Veeva AI, an agentic AI tool designed to boost productivity by fast-tracking and automating tasks such as reviewing clinical data, ensuring regulatory compliance, and more.

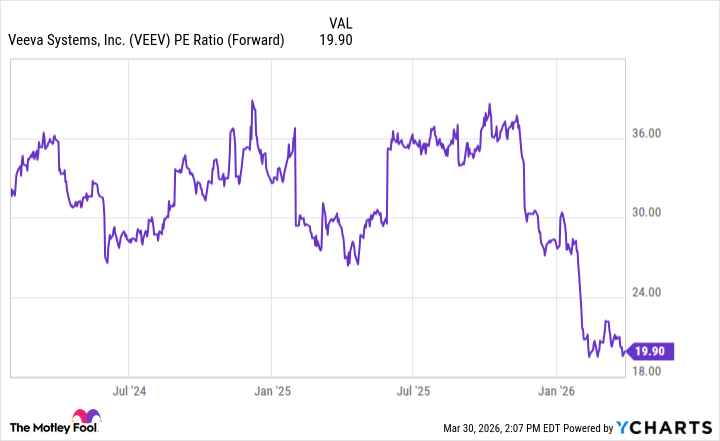

This is just the beginning, though, as Veeva Systems plans to launch more AI-powered tools, an initiative that could help it grow its market share. Third, Veeva Systems still has significant white space to exploit. The company estimates a total addressable market of more than $20 billion, which dwarfs its trailing-12-month revenue of $3.2 billion. Lastly, Veeva Systems' shares look cheaper than they have in a while.

VEEV PE Ratio (Forward) data by YCharts

The company's forward price-to-earnings ratio of about 20 is near multi-year lows. In my view, Veeva Systems could rebound and deliver outstanding returns over the next half-decade as it continues to dominate its corner of the cloud market. That's why its shares look like a screaming buy after dropping by 37%.