Financial headlines feel personal when you're retired. Every time a high-flying stock drops by double digits in a single trading session or a company's management revises its earnings guidance downward, the instinct is to act -- sell, rebalance, something.

But for retirees trying to protect what they've saved over decades of hard work, the most dangerous responses to market volatility are the ones rooted in emotion. The ongoing sell-off in artificial intelligence (AI) stocks isn't necessarily a warning sign that you need to act imminently.

Rather, it may be a much-needed reminder that you may have been positioned incorrectly at the outset. Here's what to do.

Image source: Getty Images.

Chasing narratives is a big problem when building durable wealth

Retirees who indexed heavily on AI-adjacent names -- semiconductors, cloud infrastructure companies, or enterprise software platforms -- likely did so because the story appeared compelling. To be fair, the returns from the tech sector validated this thesis for most of the last few years.

However, smart investors understand that concentrated exposure to a single theme brings fragility to your portfolio. That's the last thing you want for retirement.

When a high-growth sector enters a correction, it rarely does so gradually. Over the last few months, growth stocks have shown harsh gap downs upon capex surprises and a shift in sentiment around the pace of AI monetization.

Retirees are at risk of locking in these valuation de-ratings more permanently compared to the paper losses a beginner investor has to endure. In turn, poorly timed losses in retirement can diminish a portfolio's durability and longevity. Luckily, the solution isn't to abandon equities entirely. It's simply to widen your aperture.

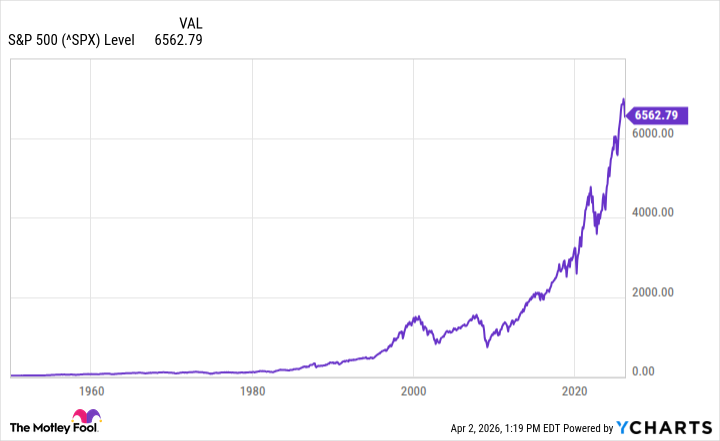

How the S&P 500 does the heavy lifting for retirees

The S&P 500 is one of the most resilient instruments available to long-term investors. The index gives you exposure to the largest U.S. companies and automatically rebalances as winners thrive and laggards get replaced.

If AI someday delivers on its promises, the S&P 500 is positioned to capture the upside, because the companies developing, monetizing, and purchasing AI are all included in its holdings. In contrast, if AI disappoints over the coming years, the index's diversification insulates your portfolio from feeling downside pressure in concentrated doses.

Notably, the S&P 500 has an unmatched long-term track record when benchmarked against any single sector thesis. The index has survived the dot-com bubble, the 2008 financial crisis, a global pandemic, and every macro-driven scare in between.

Retirees who stayed the course and invested in broad index funds through these cycles didn't just recover -- they managed to compound their wealth. Time in the market -- not timing the market -- is the key pillar supporting wealth preservation at a stage when capital protection matters most.

How should retirees invest right now?

If you are a retiree sitting on AI positions that are in the red, the question isn't whether to sell. It's whether you're comfortable lowering your cost basis and adding to those positions today.

If the answer is no, it may be time to trim this concentrated exposure and rotate toward broader index funds such as the SPDR S&P 500 ETF Trust (SPY +1.65%), the Vanguard S&P 500 ETF (VOO +1.60%), or the Invesco S&P 500 Equal Weight ETF (RSP +1.30%). As a sweetener, you may be able to use any losses from AI stocks to offset your tax liability.

In addition to these rebalancing efforts, it would behoove retirees to hold short-duration bonds or money market funds to help finance basic living expenses. This approach provides a liquidity buffer and allows you to avoid selling equities to raise cash during market downturns.

The AI revolution could still play out as its most enthusiastic advocates contest. But a retirement portfolio shouldn't bet the house on this, or any, narrative. Retirement funds need to be constructed to survive every economic cycle -- euphoric and brutal ones alike. This is exactly what broad market exposure through the S&P 500 is designed for.