The knock on Microsoft (MSFT -1.77%) stock in 2026 is self-explanatory: Capital expenditures (capex) are ballooning, Azure growth is moving a half-step slower than Wall Street demands, and an uncomfortable portion of the cloud backlog is tied to a single unprofitable partner, OpenAI.

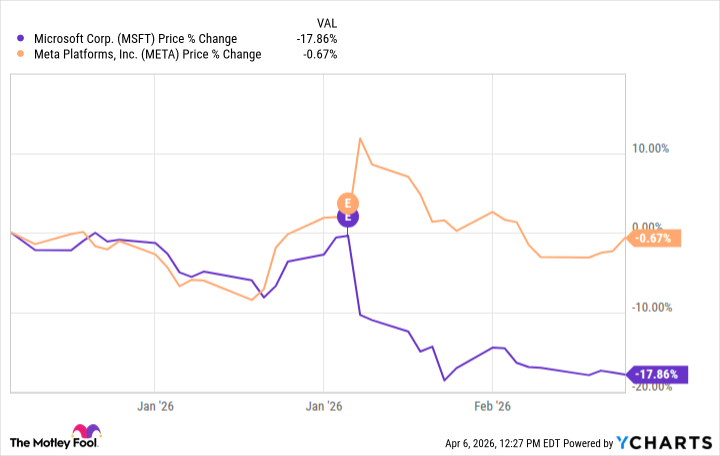

The stock has shed roughly a third of its value from all-time highs -- its worst drawdown since 2008. On the surface, the panic seems fair. But smart investors are looking at things beyond rising infrastructure costs and quarterly cloud growth.

Let's explore some themes that deserve closer inspection at Microsoft to help determine whether this sell-off is warranted or a once-in-a-decade opportunity to buy the dip.

Image source: Getty Images.

Microsoft's problem is rooted in perception

One of the lesser-discussed drivers behind Microsoft's decline concerns who reported earnings the same week. Like Microsoft, Meta Platforms guided for significantly higher infrastructure expenses for this year. But unlike the Windows maker, Wall Street cheered Meta's budget choices.

The asymmetry illustrated above reveals something important: The market isn't penalizing capital spending at all. Instead, investors are selectively penalizing the narrative behind spending choices.

Meta illustrated how its AI investments are enhancing monetization across the company's advertising empire. By contrast, Microsoft told a story of infrastructure -- ongoing buildouts for new data centers and custom chip designs.

The short attention spans that sometimes dictate Wall Street's next move decided one company was winning and one was lagging. This is nothing short of a perception problem.

The Copilot critics are discounting important data

The prevailing bear case on Microsoft leans heavily on Copilot's underwhelming performance. CoPilot's adoption rates have admittedly been slower than the initial hype suggested. It's true that consumers and enterprises have optionality as competing large language models (LLMs) release new products and services at breakneck speed.

However, this critique has far more merit at the consumer margin level than in the realities of how enterprise software budgets are constructed. Copilot is not an app that people download on their mobile device for generic queries. Rather, CoPilot is purpose-built to win multiyear contracts with Fortune 500 companies as its capabilities become embedded across critical applications.

Unlike consumer apps, enterprise software platforms don't go viral. They slowly metastasize, quietly expanding horizontally through organizations over the course of years.

The number of enterprise customers with more than 35,000 Copilot seats tripled in a single year. What skeptics are missing is that CoPilot is simply a new-category product type that comes with a long sales cycle for the time being.

NASDAQ: MSFT

Key Data Points

Is Microsoft stock a buy?

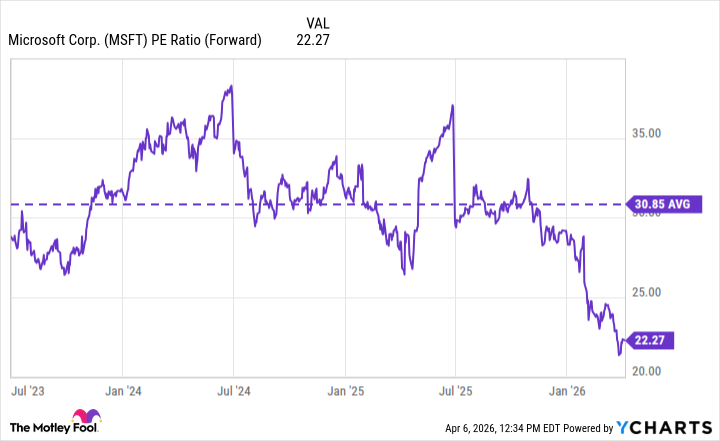

Microsoft now trades at roughly 22 times forward earnings, well below its own 10-year average. This is less a distressed valuation than it is a hard reset for Microsoft stock.

MSFT PE Ratio (Forward) data by YCharts

While the risks are real, Microsoft's moat, featuring enterprise lock-in at a scale, a balance sheet that can absorb multiyear infrastructure buildouts without blinking, and a diversified software portfolio that generates cash during any economic cycle, is not fractured.

Microsoft stock isn't broken. It's simply experiencing a harsh rerating as the company is held to a standard it hasn't yet met. Over time, I'm optimistic this gap will close.

The smart question isn't whether to buy Microsoft stock right now. It's whether you have the patience and conviction to hold it while the rest of the market slowly realizes that it asked the wrong questions to begin with.