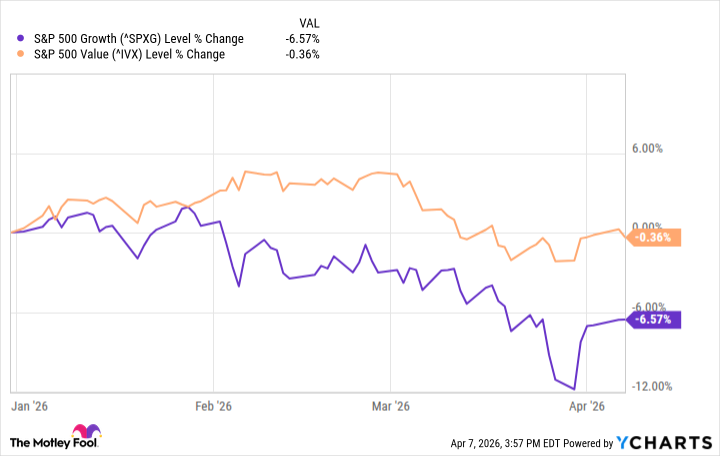

If you're a close follower of the stock market's inner workings, then you likely already know growth stocks have trounced value stocks for the better part of the past six years. Specifically, since the market's COVID-19 pandemic-prompted low in mid-March of 2020, the S&P 500 Growth index has rallied a little more than 200% versus the S&P 500 Value index's measurably more modest gain of just over 130%. Credit the incredible proliferation of artificial intelligence (AI), mostly, which disproportionally favored a small handful of big growth companies.

As the old adage goes, nothing lasts forever. Change is underway right now, in fact. Since the beginning of this year, the value index has held its ground while growth stocks have slipped nearly 7%.

Data by YCharts.

Not a surprising performance

It's not exactly an earth-shattering disparity. Three and a half months isn't a terribly long time, and a 7% performance disparity isn't enormous.

All big trends start out as small ones, though, and the argument that growth stocks have peaked and value stocks are poised to take the lead for a while holds more than a little water.

That's what analysts at Invesco expect, anyway. As Senior Director of U.S. Value Product Management Tracy Fielder penned late last year right before the aforementioned divergence started taking shape, "value stocks, based on the Russell 1000 Value Index, are at a 30% discount to the S&P 500 Index (^GSPC +1.18%), and a 50% discount to growth stocks, based on the Russell 1000 Growth Index." Their performance in the meantime suggests most investors agree.

Image source: Getty Images.

And it's not just Fielder. JPMorgan's market outlook for 2026 agrees, explaining "with overall valuations at multi-decade highs, select value sectors should play a bigger role in [portfolio performances] 2026." Economic uncertainty stemming from lingering inflation, conflict in the Middle East, and an artificial intelligence revolution that isn't quite as revolutionary as initially anticipated all make value stocks more compelling investment prospects if only because they offer at least a little more performance certainty than growth stocks do at this time.

Such a shift is certainly coming sooner or later

Past performance is no guarantee of future results, of course, and there are exceptions to ... well, everything. Not every value stock is poised to shine from here, just as not every growth stock will struggle. Indeed, JPMorgan's outlook acknowledges "growth should continue to fare well as the long-term secular force of AI continues to mature."

Do view the hint being given by recent performances through a lens of strategic realism, though. Change is normal -- and even predictable -- in the market, across both sector and style leadership. Veteran investors know such a change is coming sooner or later, but without any announcement or real fanfare. This performance diversion may be the only early warning that anybody's going to get.