After a 58% surge in 2025, Constellation Energy (CEG +3.37%) was the darling of the nuclear power and artificial intelligence (AI) data center energy trade. Its momentum has turned since the start of the year, as regulatory uncertainty and a lofty valuation weigh on the stock. Here's what is troubling Constellation Energy, along with thoughts on whether investors should buy the weakness in the energy stock right now.

NASDAQ: CEG

Key Data Points

Constellation Energy's weak start to 2026

Constellation Energy's biggest strengths are its existing energy infrastructure and massive nuclear energy footprint. The company operates 21 reactors across the United States, accounting for nearly one-quarter of the country's active reactors today. It also has a strong presence in the PJM Interconnection, a fast-growing region for data centers that serves 13 states in the Northeast and Midwest.

As an independent power producer (IPP), Constellation owns and operates power plants and sells its electricity into the open market. In contrast, regulated utilities are overseen by the government and have rates approved by regulators. As an IPP, Constellation benefits when electricity demand is strong, and prices rise. However, it is vulnerable to falling prices and to the regulation of electricity capacity.

Image source: Getty Images.

In January 2026, the White House National Energy Dominance Council (NEDC) and all the governors from the PJM states issued a Statement of Principles calling for an emergency capacity auction to be held by September 2026. As part of the proposal, hyperscalers would bid for 15-year power purchase agreements (PPA), forcing them to fund the construction of new gas or nuclear plants so that rising electricity costs aren't passed on to households.

To shield consumers from skyrocketing prices, PJM and the Federal Energy Regulatory Commission (FERC) have implemented a price collar for upcoming auctions. For the 2026/2027 and 2027/2028 delivery years, a price cap of $325/MW-day and a floor of $175/MW-day have been established. As of March 2026, PJM has asked FERC to extend this price collar to the 2028/2029 and 2029/30 auctions to prevent further spikes in consumer prices.

Regulations and price collars limit the amount of windfall profit Constellation could make during supply shortages. On top of that, Constellation management forecasted earnings per share (EPS) for this year to be between $11 and $12, below analysts' estimates of $12.11, which is why the stock has gotten off to a slow start this year.

Buy the dip on Constellation Energy

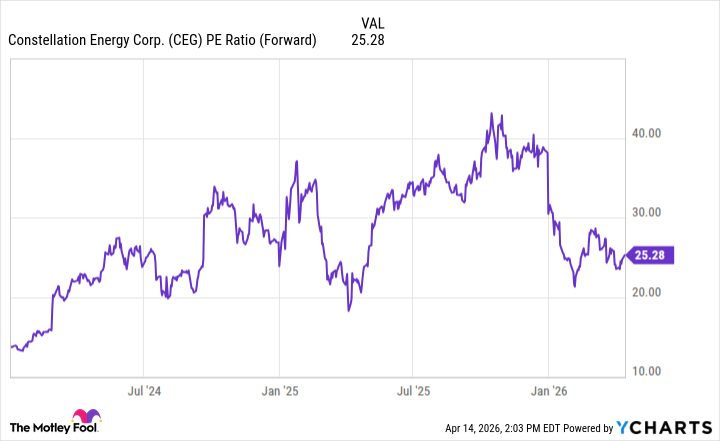

Recent share selling has hurt Constellation, and there could be some limit to its recovery upside if regulators continue to put price caps in place and limit deals with hyperscalers. That said, its valuation has come down from 40 times forward EPS to 25 times forward EPS in recent months.

Data by YCharts.

Constellation owns a slew of assets across the United States and is adding capacity and making deals directly with hyperscalers through colocation deals, which could provide further upside for the power producer. As AI demand for electricity continues to grow, Constellation should benefit from its massive fleet of energy assets, making the recent dip a good opportunity for investors who haven't already gotten in.