Nvidia's (NVDA -0.10%) stock is up 76% in the last year alone. But did you know that Intel (INTC -1.24%) has trounced the market, up 241% over the last 12 months? That's right -- the struggling computer chip maker that has fallen from its leadership position is finally seeing its stock price rebound due to investments from the U.S. government, potential large foundry customers, and Nvidia itself.

Intel may have lost its pole position in advanced computer chips to Nvidia years ago, but that doesn't mean you should leave it for dead. Here's what the next five years may look like for both Nvidia and Intel, and what it could mean for their stock prices going forward.

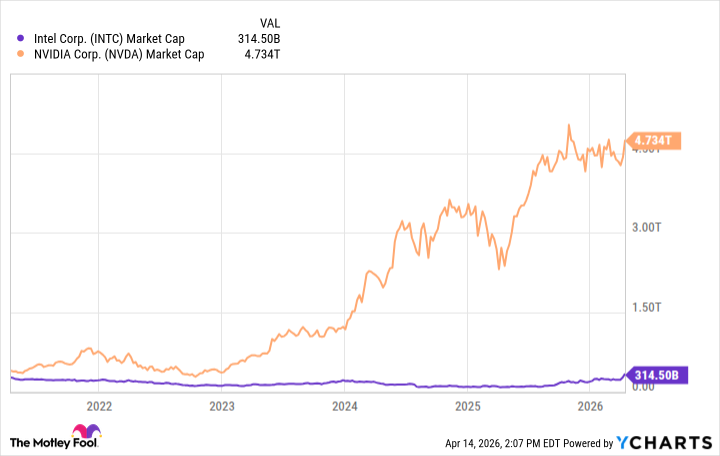

Image source: Nvidia.

Weaker historical financials

There's no denying that the past few years have looked bad for Intel. Revenue from its personal computing division fell after the pandemic consumer hardware boom, while demand for artificial intelligence (AI) drove its data center customers to spend more on Nvidia computer chips than on Intel. Partly due to divestitures, Intel's revenue is actually down over the last 10 years. Net income has fallen from a peak of around $20 billion to breakeven in 2025.

On the other hand, Nvidia has become one of the most profitable businesses in the world in the last few years. Revenue has grown by 1,000% in the last five years to $216 billion, while net income has soared to $120 billion. Nvidia's ultrapowerful AI systems, manufactured by Taiwan Semiconductor Manufacturing (TSMC), are taking over the data center market, leaving Intel in the dust.

NASDAQ: INTC

Key Data Points

Uncertain future prospects

Well, if Nvidia is crushing Intel, why is Intel's stock price up more over the past year?

Wall Street generally does not value a stock based on past performance, but on what it believes the company can generate in future earnings. Intel's prospects are looking brighter for a few reasons. One, the United States has determined that it wants Intel to succeed, and it took a 10% stake in the business last year. Two, Intel is slowly building a customer list for its foundry business, which will manufacture chips for third parties, similar to TSMC. Third, Intel began at a much cheaper valuation, with its market cap below $100 billion 12 months ago, versus $3 trillion for Nvidia.

Investors are betting that the future will look better for Intel, especially if it can garner customer orders from the likes of Amazon, Microsoft, and even SpaceX/Tesla for the proposed factory partnership between the two Elon Musk businesses. Even Nvidia has a proposed partnership with the foundry.

NASDAQ: NVDA

Key Data Points

Nvidia is doing just fine at the moment, but there are worries about rising competitive pressures for its data center market. Its own customers, like Amazon, are investing heavily in homegrown computer chips manufactured by Nvidia's supplier, TSMC (and, in the future, perhaps Intel), which could box Nvidia out of future growth. The company has done phenomenally well, but with a starting price-to-earnings ratio (P/E) of 39, any investor buying today is going up against tough expectations for future growth.

Data by YCharts.

Where will Intel stock be in five years?

Intel's future is a bit tricky to value, as it does not generate a profit today. This is entirely dragged down by its foundry business in building computer chips for third parties, which burned $2.5 billion last quarter alone. Its personal computing and data center business segments remain profitable.

If the foundry business scales up, Intel may reach $100 billion in revenue five years from now, up from $52 billion in 2025. It will likely not achieve the same profit margins as TSMC (54% operating margin last quarter), but it could reach about half that level at 25% with the beginnings of operating leverage and the pricing power inherent in selling AI computer chips.

That would lead to $25 billion in annual earnings for Intel, compared to zero today. With a current market cap of $312 billion compared to almost $5 trillion for Nvidia, Intel stock still has room to run if you believe it will begin to win back market share of computer chip sales.