Carnival Corp. (CCL +0.46%) stock has experienced a brutal sell-off amid the dramatic spike in fuel prices. In a sense, this reaction is understandable due to the cruise line's heavy dependence on fuel.

However, fuel costs are only one of the factors that can make or break a travel stock like Carnival. Such factors leave investors questioning whether Carnival stock is a bargain or a trap.

Image source: Carnival Corp.

Carnival and its fuel situation

Carnival is the world's No. 1 cruise line, carrying nearly 42% of all cruise passengers, according to Cruise Market Watch. This means that Carnival is probably the cruise line most affected by higher fuel prices.

The company spent $397 million in the first quarter of fiscal 2026 (ended Feb. 28), helped by efforts to reduce fuel consumption. It also spent $1.8 billion on fuel in fiscal 2025, a 10% yearly reduction. Still, the recent spike in fuel prices has likely more than reversed these savings from falling consumption.

So profound are the effects that Carnival forecasts an impact of more than $500 million for the year, reducing its anticipated profit for fiscal 2026 to $2.21 per share, down from the predicted $2.48 per share in the previous quarter.

NYSE: CCL

Key Data Points

Fortunately, Carnival has benefited from a record performance. It reported 103% occupancy in Q1 (100% occupancy means two people in every cabin). It also announced record bookings, and demand has extended well into 2028, meaning it has to discount less to fill its cabins.

Such conditions make it likely that it can pass fuel costs on to its passengers. While it maintains the right to add a surcharge of up to $9 per person per day when oil is consistently above $70 per barrel, it has so far chosen not to do so.

Moreover, even if fiscal 2026 earnings come to $2.21 per share, it will still be higher than the $2.10 per share earned in fiscal 2025. This means that while growth may have slowed, it likely has not stopped.

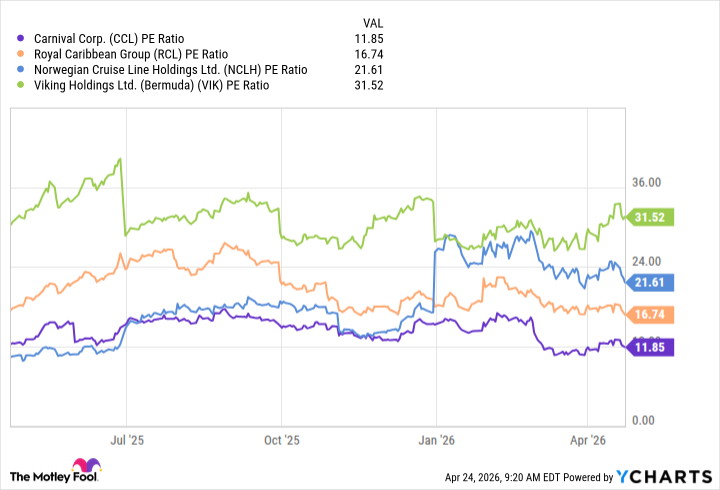

Plus, Carnival stock is cheap. Currently, it trades at about 12 times earnings, well below the P/E ratios of rivals Royal Caribbean, Norwegian Cruise Line Holdings, and Viking Holdings. That situation may limit the potential downside for investors who buy Carnival now.

CCL PE Ratio data by YCharts

Is Carnival a bargain or a trap?

As conditions stand now, Carnival is more than likely a bargain.

Indeed, the risks of higher fuel costs could add to passenger costs and possibly sap the demand for cruises if those costs stay high.

However, economic uncertainty has not dampened demand for cruises. Also, the 12 P/E ratio positions Carnival stock to surge higher should the higher fuel prices fall. That in itself should indicate that investors who are willing to take the risk should buy and hold.