Today's Highlights

📌 Top story -- scroll down for more updates

PayPal Sells Off On Guidance

1:15 pm — PYPL -8.97%

By Buck Hartzell

PayPal (PYPL -0.76%) had a pretty decent quarter. Total Payment Volume increased 11% to $464 billion or 8% f(x) neutral basis. But GAAP operating income decreased 3% to $1.5 billion. PayPal is looking for $1.5 billion of cost savings over the next 2-3 years, by removing people and AI automation. They are also upgrading their tech stack to become cloud native. Do these types of upgrades ever get done on time and on budget? Q2 guidance is for non-GAAP EPS decline of 9%. We all knew PYPL needed work. Meanwhile they bought another $1.5 billion in stock. I care more about repurchases than Q2 guidance.

Burry Dumps GME After eBay Bid Kills His Thesis

10:00 am — GME -2.56% in pre-market trading

Michael Burry has officially abandoned his GameStop (GME -0.73%) investment, selling his entire position following the retailer’s "audacious" $55.5 billion bid for eBay (EBAY +0.43%). The "Big Short" investor noted that while he initially envisioned GME transforming into an "Instant Berkshire" similar to Berkshire Hathaway (BRKB +0.36%), the massive debt required for the deal shattered his thesis. Burry warned that the acquisition could push leverage to a "borderline distressed" 7.7 times EBITDA, drawing unfavorable comparisons to struggling firms like Wayfair (W -5.44%) and Carvana (CVNA +1.50%). Despite CEO Ryan Cohen’s combative defense of the $125-per-share offer, GME shares tumbled 10% as markets balked at the $20 billion financing gap.

- Balance Sheet Red Flags: The proposed deal relies on a $20 billion letter from TD Bank (TD +0.13%), leaving nearly $35 billion in funding unaccounted for beyond dilutive equity issuance.

- The "Instant Berkshire" Burial: Burry’s exit signals a major loss of confidence from the value-investing community, shifting the narrative from creative transformation to reckless over-leverage.

Shopify's Guidance Steals the Thunder

9:45 am -- SHOP -5.84%

By Matt Frankel, CFP®

Team Hidden Gems

Shopify (SHOP -4.29%) delivered the kind of quarter that should have cleared the bar, but its outlook gave investors pause. Revenue jumped 34% from the year-ago period to $3.17 billion, topping Wall Street's estimate of $3.09 billion, while GAAP earnings of $0.45 per share blew past the $0.24 consensus by 90%. Operating income nearly doubled to $382 million as the platform's higher-margin product mix kicked in.

Most of that momentum came from Merchant Solutions, which covers payment processing and merchant lending. Its 39% revenue growth far outpaced the 21% rise in Subscription Solutions (the recurring software fees merchants pay to use the platform), and that mix shift is doing more work than the headline. Heavier reliance on payments and loans is pulling overall margins down, and the cost is showing up in transaction and loan losses, which climbed 55% to $116 million. Those losses now eat 3.7% of revenue, up from 3.2% a year ago, a trend management will need to monitor as the lending book grows. Looking ahead, the company guided to high-twenties percent revenue growth next quarter, signaling deceleration from this quarter's pace.

NASDAQ: SHOP

Key Data Points

Shopify's Q1 Dip Is Noise for Long-Term Bulls

8:15 am -- SHOP -6.72% in pre-market trading

By Yasser El-Shimy

Team Rule Breakers

Foolish investors would be well-advised not to miss the forest for the trees in Shopify's (SHOP -4.29%) Q1 report. The Canadian e-commerce juggernaut delivered a stellar Q1, with revenue jumping 34% to $3.17 billion and Gross Merchandise Volume topping $100 billion. Operating income nearly doubled to $382 million: showing tremendous operating leverage for Shopify.

Why did shares tumble pre-market? Guidance and valuation are the likely culprits. Shopify forecast Q2 revenue growth in the "high-twenties". While robust, this is a deceleration, and the Street may have been hoping for above estimates guidance. With the stock trading at a relatively high forward P/E near 85X, the market priced in perfection. Any hint of slowing growth triggers profit taking.

For long-term shareholders, this is noise. The underlying business is compounding beautifully, and their AI pivot is just beginning. If I have been waiting to start or add to a position, this post-earnings haircut offers an opportunity into a generational e-commerce winner.

This Morning's Breakfast News

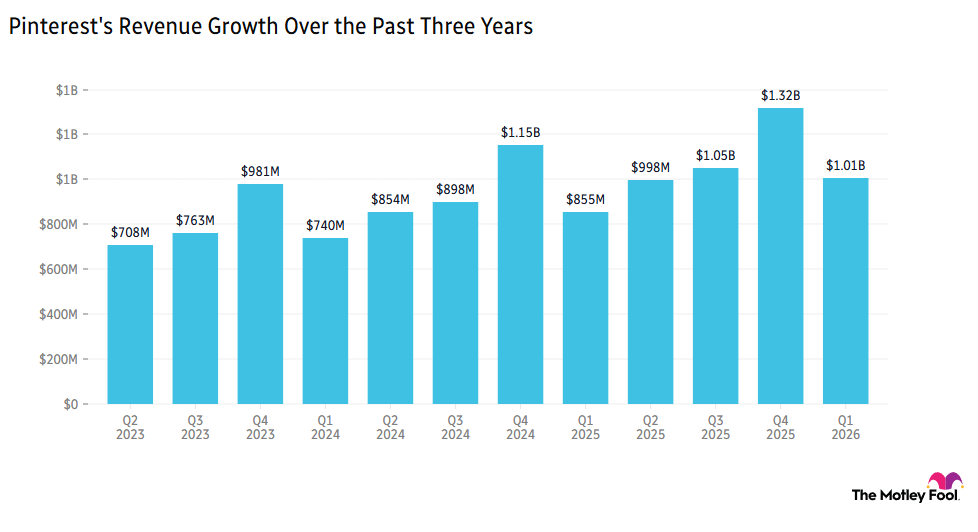

7:30 am -- PINS +15.97% in pre-market trading

Pinterest (PINS -1.72%) soared over 15% ahead of the market open after results showed the fastest sales growth since Q2 2024, driven by higher monthly active users (MAU), with revenue guidance for the coming quarter ahead of expectations.

- "We remain focused on ensuring monetization more fully reflects the strength of our engagement": The 11% jump in MAU versus last year represented a 10th straight quarter of double-digit user growth, yet CEO Bill Ready explained the push continues to turn this into tangible profits.

- "The bull case for Pinterest is compelling": In March, Fool analyst Rich Greifner explained the Rule Breakers recommendation "boasts a large, engaged user base with high commercial intent -- exactly the audience advertisers covet."

Apple Eyes Intel for AI Chips

7:00 am -- AAPL -0.15%, INTC +3.55% in pre-market trading

Bloomberg reports Apple (AAPL -7.35%) has held internal talks about using new processor manufacturers, including Intel (INTC -1.02%), as a way to limit supply chain disruptions and diversify away from using Taiwan Semiconductor (TSM +0.23%).

- Lack of chips for iPhone and Mac is constraining growth: The news comes swiftly after CEO Tim Cook explained the business has "less flexibility in the supply chain than we normally would" on the quarterly earnings call last week.

- Landing Apple would be a major win for Intel: Intel CEO Lip-Bu Tan is targeting new customers for chip production as part of the turnaround strategy, making the company a natural fit to take some market share away from incumbents such as TSM.

NASDAQ: AAPL

Key Data Points

Axos Posts Strong Q1 With Eye on M&A

6:00 am

By Buck Hartzell

Axos (AX +2.98%) reported an 18.7% YoY jump in diluted EPS to $2.15. Book value per share grew 17.7% YoY to $53.89 too. But the biggest jump was in non interest income which jumped from $33.3 million to $85.9 million this year. But $22 million of that was a one time legal settlement. Verdant leasing generated $23.7 million on non interest income too.

Axos purchased $2.3 billion in deposits from Jenius Bank and $3.2 billion of IRA savings and CDs from Capital One. The M&A environment is looking attractive to Axos. Their own stock is attractive relative to the overall market too.