Artificial intelligence (AI) has played a central role in driving the stock market rally over the past few years. That's not surprising, as the massive investments in data center infrastructure and the deployment of AI software by enterprises have been driving up revenue and earnings growth for companies across several industries.

The Global X Artificial Intelligence & Technology ETF, an AI-focused exchange-traded fund that invests in companies benefiting from deploying AI in their products and services and selling related hardware, has soared by 145% over the past three years. That's well above the 85% appreciation in the S&P 500 index over the same period.

AI stocks can continue to outperform the broader market, as companies in this sector continue to report stunning growth quarter after quarter. In fact, there are a few AI stocks that have the potential to even double this year. Let's look at two such names.

Image source: The Motley Fool

Micron Technology

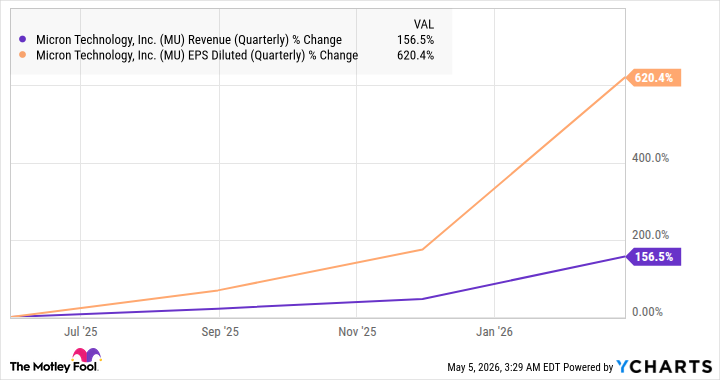

Memory chip specialist Micron Technology (MU +0.90%) has been enjoying stunning earnings growth, driven by strong demand for dynamic random-access memory (DRAM) and NAND flash storage in AI data centers. The following chart clearly shows the rapid acceleration in Micron's margins and earnings in recent quarters.

MU Revenue (Quarterly) data by YCharts

Importantly, the favorable demand-supply environment that's fueling Micron's terrific growth is here to stay for the rest of the year. Market research firm Gartner expects the memory market's revenue to almost triple in 2026 to $633 billion over last year. Higher memory prices and strong demand will drive this massive jump.

The firm notes that the price of DRAM, which accounted for 79% of Micron's revenue in the previous quarter, is on track to jump by 125% in 2026. What's more, Gartner adds that "any meaningful pricing relief is not expected until late 2027," paving the way for Micron to continue delivering strong growth in earnings.

NASDAQ: MU

Key Data Points

Micron's earnings are expected to jump sevenfold in the current fiscal year to $58.08 per share, according to Yahoo! Finance consensus estimates. A 75% increase is anticipated in the next fiscal year to $101.47 per share. Even if Micron trades at 20 times earnings at that time, a significant discount to the Nasdaq Composite index's earnings multiple of 40, its stock price will reach $2,029.

That's almost 3.5 times of where Micron stock is right now, indicating it will not only double this year but also carry its strong momentum into 2027.

Nvidia

Nvidia (NVDA +1.30%) has become too cheap to ignore right now, and that's because it has been underperforming the broader market over the past six months despite clocking healthy revenue and earnings growth. Nvidia stock has remained flat over the past six months, compared with the 51% surge in the PHLX Semiconductor Sector index over the same period.

NASDAQ: NVDA

Key Data Points

As a result, investors can now buy this semiconductor giant at just 25 times forward earnings. That's a steal, considering that Nvidia's growth is poised to accelerate significantly in fiscal 2027 (which coincides with the majority of 2026). The company's earnings grew by 60% in the previous fiscal year to $2.99 per share.

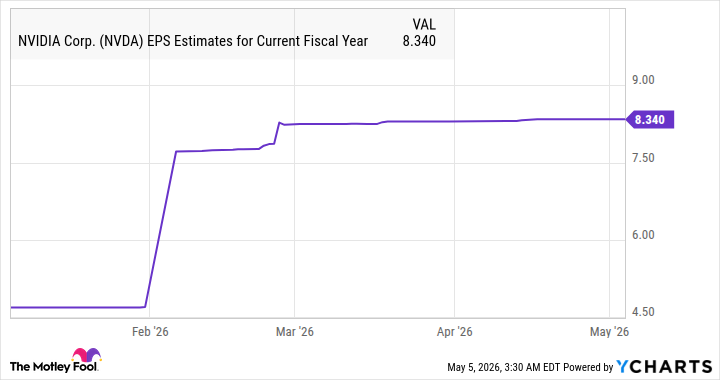

Analysts are expecting a 75% jump in Nvidia's earnings to $8.34 per share in the current fiscal year. However, the estimates have been increasing lately.

NVDA EPS Estimates for Current Fiscal Year data by YCharts

There is a solid chance Nvidia will roar past Wall Street's expectations in 2026 because of its massive revenue backlog. The company expects to sell $1 trillion worth of its Blackwell and Vera Rubin processors in 2026 and 2027.

That's a sizable upgrade over Nvidia's estimate of $500 billion in revenue from these two processor families for 2025 and 2026. The company's data center business generated a record $194 billion in revenue in the previous fiscal year, up 68% from the previous year. So the $1 trillion forecast for the next couple of years suggests Nvidia is likely to see healthy acceleration in its data center revenue in 2026.

The resulting acceleration in Nvidia's bottom line should ideally be rewarded with a premium valuation. Let's say it trades at 50 times earnings at the end of the year, a premium to the Nasdaq Composite's average earnings multiple due to the market-beating earnings growth it is poised to deliver. Its stock price could more than double to $417.

So, it isn't too late for investors to buy Nvidia stock yet, as it could come out of its slump by delivering stellar quarterly reports this year and soar to new highs.