Sandisk (SNDK +2.12%) has been on a tear on the stock market since its separation from Western Digital in February 2025, rising by a stunning 4,200% in just over a year.

Sandisk's phenomenal rise has been fueled by the terrific demand for its NAND flash storage products, which are used in data centers, smartphones, personal computers (PCs), and other devices. Artificial intelligence (AI) data centers have cornered a significant chunk of the available NAND flash supply, creating a massive supply gap that has led to a sharp spike in the price of Sandisk's products.

However, the rapid rise in Sandisk's revenue and earnings has brought its stock price to around $1,500. It was trading at just under $40 a share after its listing on the stock market in February 2025. The stunning jump in this AI stock could encourage management to go for a stock split.

Let's see why such a move could make sense.

Image source: The Motley Fool.

Sandisk could go for a stock split to make its shares more accessible

A stock split happens when management decides to multiply or divide a company's outstanding shares without impacting its market cap. A forward stock split has been quite common among technology companies in recent years, as the AI-fueled rally in tech stocks has led to soaring valuations and high stock prices.

NASDAQ: SNDK

Key Data Points

Though a forward stock split is purely a cosmetic move, as it simply increases a company's outstanding share count by lowering the price of each share, there is a belief that making such a move could help increase demand for a company's shares. For instance, Sandisk's high share price of around $1,500 could keep it out of the reach of retail investors who may not have such investible cash at their disposal.

As a result, a 10-for-1 forward stock split could bring its price down to $150 by increasing the outstanding share count, thereby helping it attract more investors and increasing demand for Sandisk stock. Of course, the company's fundamentals won't be altered by such a move, and the stock's future performance will be governed by its financial performance.

Moreover, many brokerages allow investors to buy fractional shares. So, they can still buy this tech stock despite its high price. This probably explains why Sandisk's rally isn't slowing down, as investors have been buying the stock hand over fist due to its attractive valuation and remarkable growth.

So, if your brokerage allows you to buy fractional shares of Sandisk, doing so could be a smart move for the long run, as its solid earnings growth potential suggests more upside.

The acute shortage of memory chips should continue to be a tailwind for the stock

Market research firm Gartner recently noted that NAND flash prices could surge by 234% in 2026. Sandisk is reaping the benefits of this favorable pricing environment, reporting $23.41 in adjusted earnings per share in the third quarter of fiscal 2026 (which ended on April 3), swinging from a loss of $0.30 per share in the year-ago period.

Importantly, the memory supply shortage isn't going to end any time soon. Counterpoint Research estimates that high memory prices could last beyond 2027, driven by data center-fueled demand. The shortage is so acute that major tech companies are reportedly offering to finance the purchase of equipment for memory manufacturers.

What's more, the memory shortage is helping Sandisk secure long-term contracts with customers. The company signed three multi-year supply agreements in the previous quarter, with combined minimum revenue commitments of $42 billion, followed by another two in the current quarter. Though it hasn't disclosed the value of the new contracts signed in fiscal Q4, the size of the three contracts from the previous quarter clearly suggests that it is sitting on a massive revenue backlog.

Even better, Sandisk management noted on the earnings call that its long-term agreements include variable pricing terms "to capture upside if prices rise." As such, it is easy to see why analysts have significantly upgraded their earnings per share forecast for Sandisk.

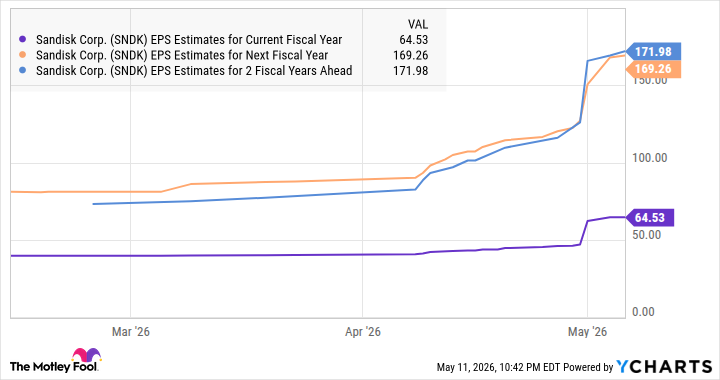

Data by YCharts

If this growth stock trades at even 30 times earnings (a discount to the tech-laden Nasdaq Composite index's average earnings multiple of 43) after a couple of fiscal years and it achieves almost $172 in earnings per share, as seen in the chart above, its price could jump to $5,160. That's 3.3x Sandisk's current stock price, indicating that it remains worth buying irrespective of a split.