Micron Technology and Sandisk are among the hottest stocks on the market, delivering stunning returns to investors over the past year due to phenomenal growth in their revenue and earnings.

Both semiconductor stocks have benefited from the incredible demand for memory chips used in artificial intelligence (AI) data centers. Moreover, memory demand has been so strong that Micron and Sandisk are unable to fulfill the same. As a result, memory prices have jumped significantly in recent months.

Given the healthy demand for memory chips, which isn't going away any time soon, manufacturers are focused on bringing additional capacity online. This is precisely why shares of Lam Research (LRCX +1.82%) have shot up by 293% over the past year. The good news for investors is that this AI stock has the potential to deliver more upside.

Image source: Getty Images.

The memory chip shortage is a catalyst for Lam Research's growth

Lam Research sells wafer and fabrication equipment to foundries, chipmakers, and integrated device manufacturers (IDMs). It gets 39% of its revenue from sales of memory manufacturing equipment.

NASDAQ: LRCX

Key Data Points

This explains why Lam has been enjoying outstanding growth. The company's fiscal 2026 Q3 revenue (for the three months ended March 29) increased by 24% year over year to $5.84 billion. Its earnings growth was even more impressive at 41% year over year, driven by higher-margin product sales and improved factory efficiency.

Lam's guidance makes it clear that its healthy growth rate is sustainable. The company's fiscal Q4 revenue guidance of $6.6 billion points toward a potential jump of 27% from the year-ago quarter. More importantly, Lam Research believes that the aggressive investments in memory and foundry manufacturing equipment will expand its addressable market and ensure that its robust growth continues.

The company pointed out in early 2025 that it was expecting NAND flash manufacturers to spend $40 billion on converting their factories to produce advanced storage devices over "several years." However, Lam now estimates that the majority of that spending will occur before the end of 2027. At the same time, Lam expects new capacity additions to boost its addressable market.

Lam has raised its WFE spending estimate for 2026 to $140 billion from an earlier estimate of $135 billion. But at the same time, Lam believes there is scope for further growth in its WFE spending forecast this year, followed by another year of solid growth in 2027.

The stock is still capable of delivering more gains

Lam has been a multibagger investment over the past year. But favorable conditions in memory and the broader semiconductor space suggest it can still move higher, especially given the healthy earnings growth it is expected to deliver.

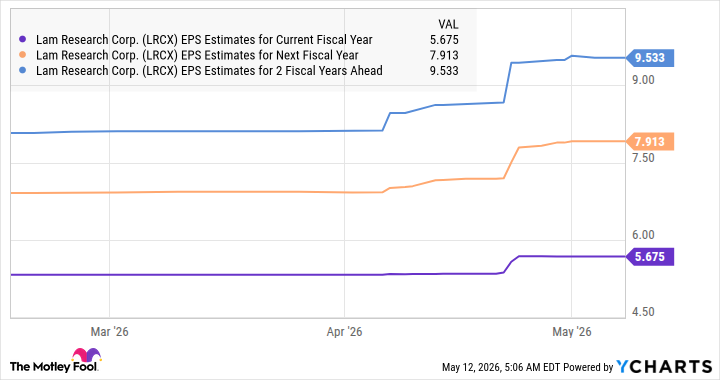

Data by YCharts

If Lam's earnings indeed reach $9.53 per share in fiscal 2028 and it trades at 43 times earnings at that time (in line with the Nasdaq Composite index's average), its stock could jump to $410. That's a potential jump of 38% in the next two years. But this AI stock could deliver bigger gains than that, as massive investments in AI data center infrastructure could create a need for more chips, thereby boosting demand for Lam's equipment.