The market has rallied from its end-of-March lows to new heights, but there are still several stocks that I think represent excellent buying opportunities. These three stocks in particular may have rallied over the past few days, but on a valuation basis, when you look at where they are trading at now compared to where they have traded historically, and where they could be by 2027, it's clear they're still positioned for some strong upside.

Image source: Getty Images.

Nvidia

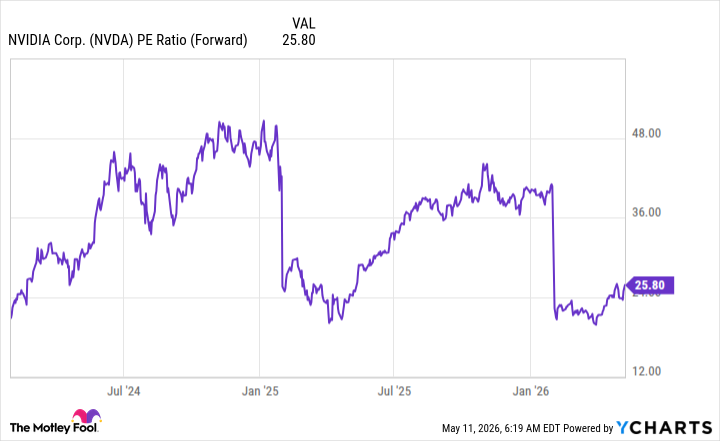

Nvidia (NVDA +1.30%) has had a strong few months and is back above a $5 trillion market cap, trading near its all-time high. So how is it still a good buy? Well, not all of its success has been priced in yet. Nvidia's shareholders are well aware of this pattern. Usually, the stock flounders during the first half of the year, then rallies in the middle. The stock appears to be doing just that, and I wouldn't be surprised if it can rise to forward earnings levels in the mid-30s by the end of summer.

NVDA PE Ratio (Forward) data by YCharts.

If it does, that would amount to a gain of around 50% from today's level. Nvidia's future share price performance will be influenced by how much the hyperscalers and data center specialists expect to devote to capital expenditures next year, and it has already received some positive hints on that front. Alphabet noted on its Q1 conference call last month that it expects a "significant increase" from 2026's capital expenditures in 2027. The chipmaker's investors should be thrilled about that, as it likely means 2027 will be another year of great growth, making Nvidia a solid stock to buy now.

Micron

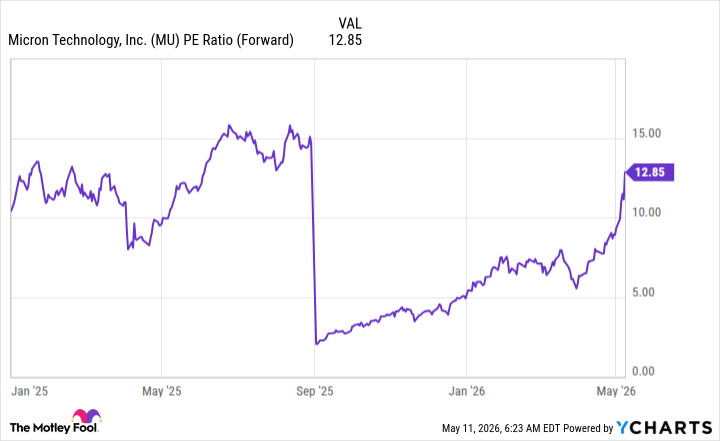

One of the biggest issues facing the AI build-out right now is a shortage of memory chips. Micron Technology (MU +0.90%) is one of the big three memory chip producers, and it's benefiting enormously from this shortage. Memory chips are essentially a commodity, so when supply is low and demand is high, prices soar. That's exactly what we're seeing with Micron, and its sales growth has been downright incredible. Two quarters ago, its revenue was $13.6 billion. In the last quarter, it was $23.9 billion. Next quarter, management expects $33.5 billion in revenue. That's a major ramp-up and showcases how Micron is going to thrive over the next few years as all of the key memory makers build new fabrication facilities that should eventually result in supply catching up to demand.

MU PE Ratio (Forward) data by YCharts.

At 13 times forward earnings, the stock looks incredibly cheap, but it will always trade at a discount to its peers due to the cyclical nature of the memory chip market. However, there is still a lot of upside from here as the memory chip shortage may take years to resolve.

Meta Platforms

Last is Meta Platforms (META +2.27%), the parent company of social media sites Facebook and Instagram. While those may be mature businesses, they are still thriving. Meta has been heavily investing in AI capabilities, and one result of those investments has been better ad performance on its platforms. These improvements helped power Meta's revenue growth to 33% year over year.

NASDAQ: META

Key Data Points

While many investors have some concerns about the size of Meta's AI-related capital expenditures, the reality is that the growth in its ad business alone is nearly justifying its spending. If Meta can deliver on some of its other AI products and promises, such as providing superintelligence to the masses, then Meta could be a stock waiting to explode higher.

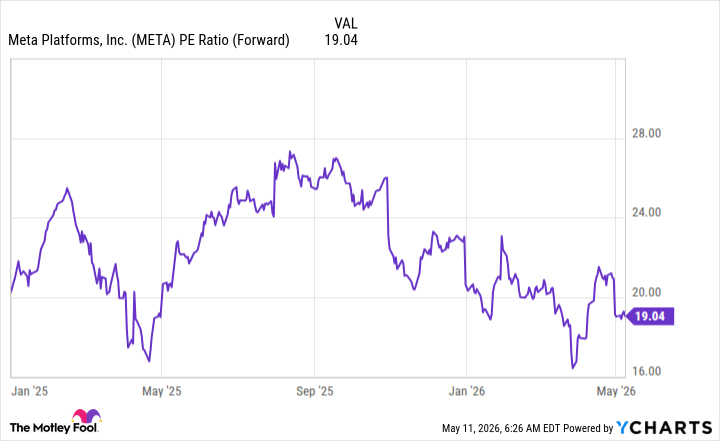

The reality is, Meta is actually pretty cheap right now, even with its impressive advertising business.

META PE Ratio (Forward) data by YCharts.

Trading at about 19 times expected forward earnings, Meta's stock is cheaper than the S&P 500. I think it's a compelling buy at these levels, and investors should scoop it up whenever they have the chance.