Apple's (AAPL -0.56%) iPhone sales increased at a solid clip in the first quarter of 2026, driven by a huge installed base of users that are in an upgrade window and the strong demand for the tech giant's smartphones in China.

Market research firm Counterpoint Research notes that Apple's iPhone shipments increased by 5% year over year in the first quarter of 2026. This increase in sales came at a time when the overall smartphone market declined by 6% in Q1 due to a memory shortage and rising component costs. The Magnificent Seven company's resilient growth in Q1 made it the world's top smartphone vendor with a 21% market share.

Cirrus Logic (CRUS +0.05%) has turned out to be a big beneficiary of Apple's improving sales. The semiconductor stock is already up 40% in 2026 as of this writing, and its close ties with Apple suggest it could deliver more upside in the future.

Let's look at the reasons why this Apple supplier's impressive stock market rally is sustainable.

Image source: Getty Images.

Cirrus Logic is delivering healthy growth due to solid iPhone sales

Cirrus Logic designs audio chips, camera controllers, haptics and sensing solutions, and power management chips for smartphones, computers, tablets, and wearable devices. Apple is its largest customer, accounting for 92% of its revenue in the fourth quarter of fiscal 2026 (which ended on March 28).

NASDAQ: CRUS

Key Data Points

The healthy growth in iPhone sales rubbed off positively on Cirrus. The chip designer's revenue increased by 6% year over year to $449 million. What's more, its earnings increased by a much more impressive rate of 17% from the year-ago period to $1.95 per share. The full-year earnings growth was also quite solid at 23% to $9.26 per share.

Cirrus noted that its margin profile is improving due to a better product mix, which isn't surprising given that the company has been winning more business from Apple. Cirrus was originally a supplier of audio codecs for Apple's devices, but it has diversified into providing haptics solutions and camera controllers over the past couple of years.

The good news for Cirrus investors is that it is poised to win more content in Apple's devices. Apple announced in March this year that Cirrus Logic is a part of its American Manufacturing Program (AMP), developing "mixed-signal solutions for a number of Apple applications, including advanced ICs to power Face ID systems." The Face ID chip is a new opportunity for Cirrus, as management noted on the latest earnings call.

Cirrus, therefore, seems well-positioned to capitalize on the strong iPhone upgrade cycle. The integration of artificial intelligence (AI) features in iPhones is encouraging users to upgrade quickly to new devices, as noted by Consumer Intelligence Research Partners last year. Moreover, Dan Ives of Wedbush Securities pointed out after the iPhone 17 launch in September 2025 that there are 315 million iPhones that haven't been upgraded in four years.

All this explains why Apple has been able to overcome the broader weakness in the smartphone market. Moreover, Cirrus Logic's guidance for the current quarter indicates its growth is poised to accelerate.

The company expects $460 million in revenue in the current quarter at the midpoint of its guidance range. That would be an improvement of 13% from the year-ago period. Looking ahead, Cirrus Logic's revenue growth could accelerate nicely due to robust iPhone demand and the new chips it will deploy for Apple.

This could pave the way for healthy growth at Cirrus, potentially unlocking more upside.

Analysts may be underestimating its growth potential

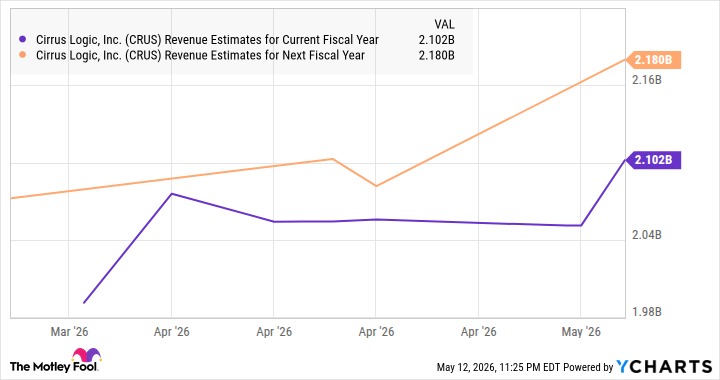

Cirrus Logic finished fiscal 2026 with $2 billion in revenue, an increase of 5% over the prior year. Analysts are projecting single-digit revenue growth from the company over the next couple of years.

Data by YCharts

However, we have already seen that the company is expecting robust double-digit growth in the current quarter. With the new business that's coming its way, don't be surprised to see Cirrus' growth significantly outpacing analysts' estimates in the future. Assuming it can clock even 10% revenue growth in the current and next fiscal years, its top line could reach $2.42 billion.

Cirrus is trading at just 4.5 times sales right now, a discount to the tech-focused Nasdaq Composite index's price-to-sales ratio of 5.5. Assuming it trades in line with the index's average after a couple of years and achieves $2.42 billion in revenue, its market cap could increase to $13.5 billion. That represents potential upside of 59% from current levels, suggesting it isn't too late for investors to buy this growth stock, even after the healthy jump it has seen this year.