One of the most anticipated events of the year has come and gone.

Friday, May 15, marked the final day of Jerome Powell's second term as Fed chair (though he'll remain on the Board of Governors) and the ascension of his successor, Kevin Warsh. It also represents a period of heightened uncertainty and instability for the Dow Jones Industrial Average (^DJI +0.59%), S&P 500 (^GSPC +1.18%), and Nasdaq Composite (^IXIC +2.07%).

Jerome Powell's final day as Fed chair was May 15. Image source: Official Federal Reserve Photo.

Warsh steps into the central bank's lead position with experience under his belt. He was previously a member of the Board of Governors of the Federal Reserve from Feb. 24, 2006, to March 31, 2011. This means he and the 11 other members of the Federal Open Market Committee (FOMC) played an important role in guiding the U.S. economy through the financial crisis.

However, Warsh intends to shake up America's foremost financial institution, which may not be the best news for Wall Street or its major indexes.

Kevin Warsh signals his desire for the Fed to become a passive entity

Before taking his post as Fed chair, Warsh first had to earn a majority vote from the Senate Banking Committee. In 2.5 hours of testimony, President Trump's nominee laid out his vision of what the central bank should be and how he'd reshape it.

As part of his written statement to the Senate Banking Committee, in response to concerns about Federal Reserve independence in light of Trump's repeated calls for the FOMC to cut interest rates, Warsh had this to say:

Fed independence is up to the Fed -- that has three implications. First, Congress is tasked with the mission to ensure price stability. Inflation is the Fed's choice. Second, Fed independence is at its peak in the conduct of monetary policy. And third, as the chairman said, the Fed must stay in its lane.

These final seven words, "the Fed must stay in its lane," point to a drastic departure from the Fed's role as an active market participant since the late 2000s.

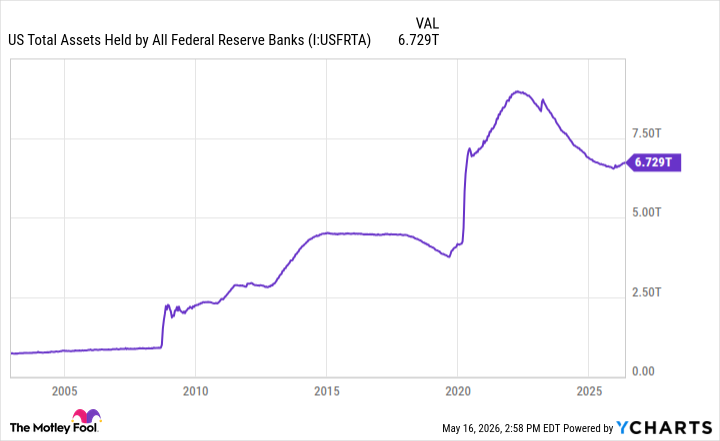

Even before his testimony, Warsh had been hypercritical of the Fed's bloated balance sheet, which grew approximately tenfold to nearly $9 trillion between August 2008 and March 2022. Although a quantitative tightening cycle reduced these total assets to $6.7 trillion as of May 2026, Warsh would still prefer these assets (primarily long-term U.S. Treasury bonds and mortgage-backed securities) to be sold.

US Total Assets Held by All Federal Reserve Banks data by YCharts.

But there's a catch to this shift in central bank ideology: selling U.S. Treasury bonds can adversely impact a historically pricey stock market.

Bond prices and yields are inversely related. If the Fed sells trillions of dollars of Treasury bonds, the expected reaction would be lower bond prices, higher yields, and therefore higher borrowing costs. Even if the FOMC doesn't alter the federal funds target rate, making the central bank a passive participant by selling its assets can have the same effect as rate hikes.

When the stock market began 2026 at its second-priciest valuation in history, investors were expecting several FOMC rate cuts. But with these cuts now shelved due to inflationary pressures from the Iran war, and the new Fed chair adamant that "the Fed must stay in its lane," the likelihood of higher interest rates is climbing.