For investors, generative AI is a gift that keeps on giving. But while popular chipmakers like Nvidia and Broadcom led the infrastructure opportunity over the last few years, computer memory specialists like Sandisk (SNDK -3.68%) have convincingly stolen the show.

The company's shares have soared by a blistering 4,000% in just 12 months -- enough to turn a $25,000 position into well over a million. This trend is driven by soaring demand for its hardware to help power data centers. Let's dig deeper to decide if the company is still capable of generating life-changing returns, or if it's a giant bubble ready to pop.

Memory has become AI's primary constraint

When OpenAI's ChatGPT hit the scene in late 2022, tech companies quickly realized that they would have to buy more and better graphics processing units (GPUs) to keep up. These chips are ideal for running and training large language models (LLMs) because of parallel computing -- the ability to process multiple calculations simultaneously.

However, over time, GPU clusters became so powerful that they began to strain the memory capacity needed to help data centers store information and access it quickly. Sandisk helps solve this problem.

Sandisk is known for its enterprise NAND flash solutions, which allow data centers to store data electronically with no moving parts. While these products may have higher upfront costs than less advanced hard disk drives (HDDs), they offer better performance and less energy consumption, which is ideal for the vast scale needed for AI data centers.

Image source: Getty Images.

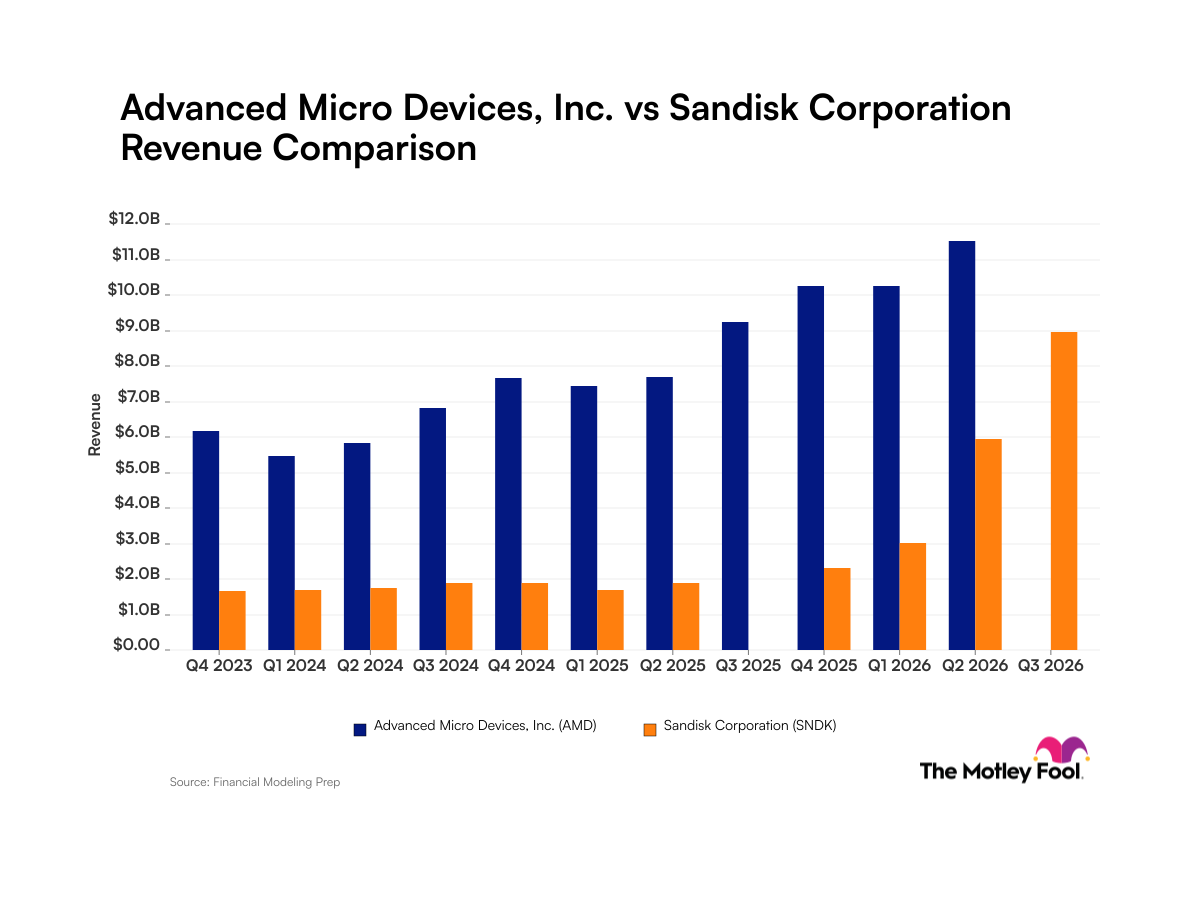

Business is booming

Analysts at McKinsey & Company estimate that spending on the global AI data center build-out could reach $7 trillion by 2030. Plenty of things could change by then. But a large percentage of that money will almost certainly go toward memory hardware solutions, putting Sandisk in an excellent position for substantial revenue and profit growth.

The company is already benefiting substantially from this megatrend. Fiscal third-quarter revenue soared 233% to $1.47 billion year over year, driven by strength in its data center segment and edge computing, which refers to memory hardware located on devices themselves instead of in data centers.

Perhaps most importantly, the company's gross margin has jumped from just 22.7% to 78.4%, a level so high that it is typically seen in software-as-a-service (SaaS) companies that don't sell physical products. This dynamic has occurred because demand for memory is far outstripping supply, allowing Sandisk to substantially increase its prices.

Operating income jumped from just $2 million to $4.2 billion -- an eye-popping gain that explains much of the stock's recent rally.

NASDAQ: SNDK

Key Data Points

Shares are still dirt cheap, but there is a catch

Despite gaining over 4,000% over the last 12 months, Sandisk's shares are still relatively affordable because profits are growing so fast. With a forward price-to-earnings (P/E) of just 23, the stock actually trades at a discount to the Nasdaq-100's estimate of 26, despite profits growing significantly faster than the typical technology company's.

This disparity can be explained by the history of the memory industry, which has a long track record of booming with new tech trends and then busting when supply catches up to demand. Sandisk's stock price suggests that, despite the AI optimism, investors are still worried that the company's elevated growth and margins won't last for the long haul.

There is also the growing possibility that generative AI itself is a bubble, and that the technology won't live up to the wild expectations driving the current levels of data center spending. If this scenario plays out, Sandisk's hyperscaler customers could eventually start cutting back on their memory spending at the same time memory supply increases, leading to a severe glut in the market and falling prices.

While Sandisk's fantastic earnings make it look like a strong buy, risk-averse investors may want to sit on the sidelines for now.