SentinelOne (S +5.15%) developed a cybersecurity platform called Singularity, which protects enterprise cloud networks, endpoints (computers and devices), and everything in between. It's powered by artificial intelligence (AI), enabling automation across key threat detection and incident response processes.

While SentinelOne stock is trading in the green this year, it's still down 78% from its record high set during the tech market frenzy in 2021. Its valuation was simply unsustainable back then, but it's now cheaper than each of its rivals in the AI-powered cybersecurity space, which could be an opportunity for investors.

In fact, the majority of the analysts tracked by The Wall Street Journal have rated SentinelOne a buy, and their average price target points to more upside ahead. Read on.

Image source: The Motley Fool.

Cybersecurity for the AI era

AI can be a dangerous technology in the wrong hands, with bad actors using it to stage sophisticated cyber-attacks at machine speed. As a result, holistic wall-to-wall cybersecurity platforms have never been more important. Singularity not only protects against breaches, but it also has powerful remediation features to help enterprises restore their networks if they succumb to a successful attack, which minimizes disruptions.

However, many businesses are also deploying AI at a rapid pace, which is creating new attack surfaces for hackers to exploit. SentinelOne launched a new tool called Prompt Security to address this challenge; it performs constant risk assessments and enforces pre-set policies in real time when AI agents are active in corporate networks, and it also secures the use of coding assistants like Anthropic's Claude Code to prevent sensitive data from leaking to third parties.

Preventative tools like Prompt Security will be increasingly important as AI is deployed more broadly across the corporate sector, because they ensure businesses adopt a secure posture from the start.

NYSE: S

Key Data Points

Accelerating revenue growth and an improving bottom line

SentinelOne had a record $1.16 billion in annual recurring revenue (ARR) at the end of its fiscal 2027 first quarter (which concluded on April 30). It was a 23% increase from the year-ago period, which actually marked an acceleration from the 22% growth the company produced three months earlier in the fourth quarter of fiscal 2026. This is a sign of significant positive momentum in the business.

The result was even more impressive considering management actually reduced marketing spending on a year-over-year basis during the quarter. In fact, SentinelOne's total operating expenses grew by just 7%, which was almost entirely from an increase in research and development spending. This allowed more money to flow to the bottom line.

SentinelOne still lost $76.1 million during the quarter on a generally accepted accounting principles (GAAP) basis, but that was a 63% reduction from its year-ago loss of over $208 million. But it gets even better, because after excluding one-off and non-cash expenses, the company was actually profitable to the tune of $12.2 million.

If SentinelOne can achieve GAAP profitability on a consistent basis, management will have more flexibility to invest aggressively in growth, which could drive further momentum at the top line.

Wall Street is bullish on SentinelOne stock

The Wall Street Journal tracks 39 analysts who cover SentinelOne stock, and 21 of them have given it a buy rating. Two others are in the overweight (bullish) camp, while the remaining 16 recommend holding. None of the analysts recommend selling.

Their average price target of $19.26 implies a modest potential upside of 16% over the next 12 months, but the Street-high target of $26 suggests a juicier potential upside of 57% might be in the cards instead. I think the latter outcome is realistic because of SentinelOne's attractive valuation.

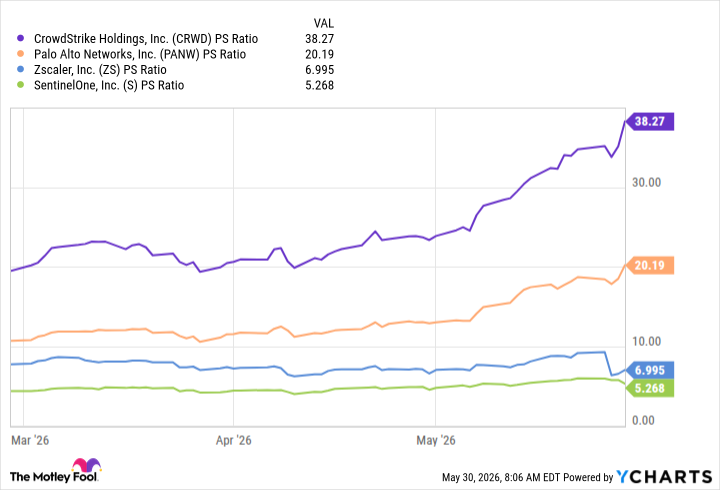

Based on the company's trailing 12-month revenue, its stock is trading at a price-to-sales (P/S) ratio of just 5.3, making it far cheaper than its rivals in the AI cybersecurity space. They include CrowdStrike, Palo Alto Networks, and Zscaler:

CRWD PS Ratio data by YCharts

CrowdStrike is a much bigger company than SentinelOne, with over $5.2 billion in ARR. Plus, it grew its ARR by 24% during its last reported quarter compared to 23% growth for SentinelOne. For those reasons, CrowdStrike deserves its premium valuation, but I would argue a sevenfold premium to SentinelOne is far too much. I'm not suggesting SentinelOne will close the gap completely, but there's certainly room for upside.

For example, a 57% gain in SentinelOne stock would take its P/S ratio to 8.3, so it would still be cheaper than CrowdStrike by several orders of magnitude. As a result, I think even Wall Street's most bullish 12-month price target is achievable.