Some may argue that Nvidia (NVDA +1.30%) is a fading stock, but I don't think that's the case. I think now could be the perfect time to buy it, especially after the market shrugged off its incredible fiscal 2027 Q1 earnings report last month. Few stocks offer the upside and value of Nvidia, and there are three reasons I think it's among the best buys in the market now.

Image source: Getty Images.

1. Data center capital expenditures are skyrocketing

At the start of 2026, everyone was marveling at how much money the AI hyperscalers planned to spend on their data center build-outs. The estimate at that time was $650 billion, but it has likely ticked up a bit since then. However, Nvidia revealed during its latest earnings call that 2027 will be another year of major increases on that front, as the company expect hyperscalers to spend over $1 trillion in capital expenditures. Given that Nvidia remains the primary supplier of computing units for those data centers, this bodes well for its future.

NASDAQ: NVDA

Key Data Points

However, the bigger trend is what is expected to occur by 2030. By then, Nvidia expects global data center capital expenditures to reach $3 trillion to $4 trillion annually. If that happens, Nvidia's stock is sure to skyrocket over the next few years.

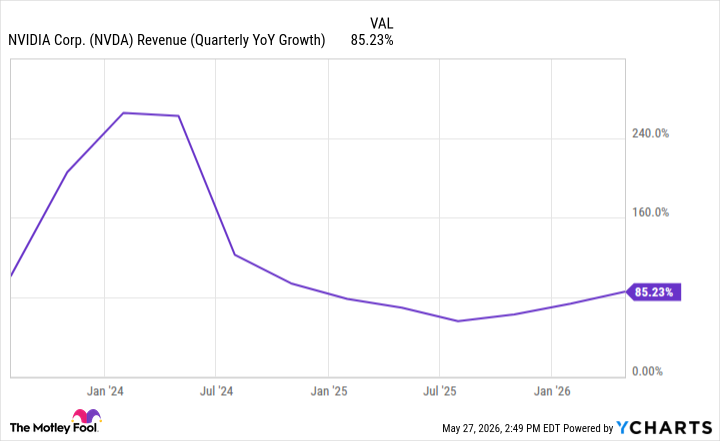

2. Nvidia's growth continues to accelerate

Back in mid-2025, everyone was convinced that Nvidia's growth rate would steadily decline after a few quarters of slowing growth. However, that trend has pivoted, and now Nvidia's revenue growth is re-accelerating. During its fiscal 2027 Q1, its revenue increased by 85%.

NVDA Revenue (Quarterly YoY Growth) data by YCharts.

Next quarter, Wall Street analysts expect 96% growth. Nvidia has a strong history of outperforming the analyst consensus, so don't be surprised if its revenue doubles next quarter. For a company of Nvidia's size to be posting this level of growth is unprecedented, and given the trend of capital expenditures, it's hard to imagine its growth slowing much over the next few years.

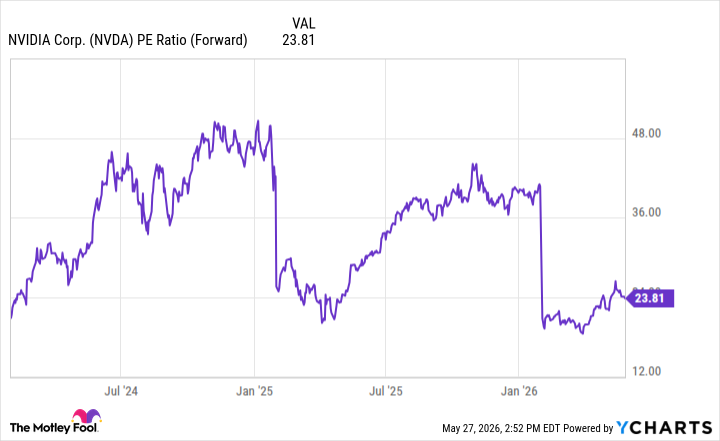

3. Nvidia's stock looks like a solid deal

Somewhere along the way, the notion that Nvidia's stock was expensive and overvalued became widespread, but that is in no way true. The best way to value the stock is in relation to its expected forward earnings, mainly because Nvidia is growing so quickly. As of this writing, Nvidia trades for 23.8 times forward earnings.

NVDA PE Ratio (Forward) data by YCharts.

That's only slightly more expensive than the S&P 500 (^GSPC +1.18%), which trades for 21.8 times forward earnings. While that ratio considers this year's projected strong growth rates, it doesn't reflect anything from the years beyond. With capital expenditures increasing and a shift toward more computing spending than construction spending, that should be another year of strong growth for Nvidia, giving the stock room to increase.

Next year, Wall Street analysts project 40% revenue growth for Nvidia. That figure has steadily been ticking up as more information becomes available regarding 2027 expenditures, and I wouldn't be surprised if it ends up somewhere in the 50% range. Because Nvidia is reasonably priced and expected to grow revenue rapidly, don't be surprised if the stock's returns echo that growth. If that's the case, investors can expect strong, double-digit returns over the next year or so, which will easily allow it to outperform the market and several of its big tech peers.